Making the correct decisions when managing your wealth is essential. To do so, you may seek advice from trusted individuals like family and friends. Unfortunately, they may be making crucial mistakes with their personal finance decisions too, leading you astray.

Here are six personal finance myths that you would want to stay away from.

#1: Financial Planning is for the wealthy

“I don’t have money to plan for the future.”

The mindset that financial planning is only for wealthy individuals is a myth many people believe. Whether you are rich or poor, it is important to take control of your finances and budget planning. If you have income and expenses, creating a plan to handle them should leave you with more to spend. In the past, barriers such as high brokerage fees made it challenging to pursue a financial plan. However, transparency and technology have made it much easier to get started in the current age.

As a general rule, purchasing every product and service you desire will quickly get you into financial trouble. Following a budget is vital when you earn or have a specific amount of money. While some individuals think that having a budget doesn’t allow you to have fun, the opposite is true. You just need to make compromises. For example, if you want to buy a new car, you may have to cut out on extra wardrobe items and restaurant outings over a defined period of time.

#2: Using Credit Cards Is Best During an Emergency

“I have 6x monthly income limit on my credit card. I should be fine”

While covering an unexpected expense using a credit card may be handy, this action can be highly detrimental. Credit card interest rates are often high. Even if you have a small debt, the interest included with each payment can slowly eat away at your funds. Creating an emergency fund for troubling times is a much better option, allowing you to pay for costs you weren’t expecting.

#3: Investing Requires a Lot of Money

“Buying Apple Shares ($148 on 13Mar23) is expensive!!”. (Owned the latest iPhone 14 SGD $1311anyway)

Investing and making money in the stock market are often associated with wealthy individuals. This is a common myth seen from the portrayal of Jordan Belfort in The Wolf of Wall Street playing on fuboTV. This movie shows Belfort’s extravagance and lifestyle fueled by his success in the stock market. While having a lot of money certainly opens up multiple avenues for investment, a lot of instruments allow the average investor to enroll – in some cases, starting with as low as $10.

You can choose your preferred instrument – be it fixed deposits, bonds, mutual funds or stocks – based on the money that you have and the risk that you are willing to take.

#4: Getting Into Debt Is Bad

“Should I take a loan for my Balenciaga T-Shirt?”

While it’s important to approach debt with caution, it can be a good decision. Borrowing money can be a handy tool to reach financial goals, such as funding a startup business or purchasing a home. While you’ll be paying interest on the amount you borrow, using debt for a positive financial pursuit can be highly cost-effective. However, using debt to finance a lavish lifestyle could lead you down the wrong path, forcing you to pay high interest. Choosing the appropriate debt tools is critical when borrowing, and the timing is also essential.

Different sectors of the economy have cycles where the values of assets go up and down. In the housing sector, if you purchase a home when values are high, thinking you can save money by deducting mortgage interest on your taxes, it may not be best. Renting allows you to wait for lower home prices. Owning a home can be a dream for many individuals. However, purchasing at the top of a cycle can become a nightmare if you have to pay high installments for an extended period. Choosing the appropriate time to get into mortgage debt can be vital if you want to benefit.

#5: Paying Off High-Interest Debt First Is Best

“Which credit card debts should I pay off first?”

If you’re following mathematics, paying off debt with high-interest rates first will lower the amount of fees you pay quicker once you close out these types of debts. While this action is a good approach, it may take a significant amount of time, making you feel frustrated.

I have found that it is helpful and motivating to pay off accounts containing a small debt (anything less than $1000) first. Once you knock a few out, you’ll have fewer accounts to deal with and can focus on paying debts with the highest interest rates.

#6: Retirement Planning Can Be Done Later

“I will plan for retirement when I’m 65”.

Another common myth relating to personal finance is that retirement planning is usually completed later in life. While starting a retirement account may be the last thing on your mind if you’ve recently graduated from college and started a new job, it can be the best time to begin this pursuit. Saving for retirement early allows you to accumulate wealth over a larger number of years. Doing so can have a significant impact on the money you have to spend when you retire.

Final Thoughts

Don’t let these myths get into your way of financial success. Discern between the noise and what make sense to you.

March Forward!

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

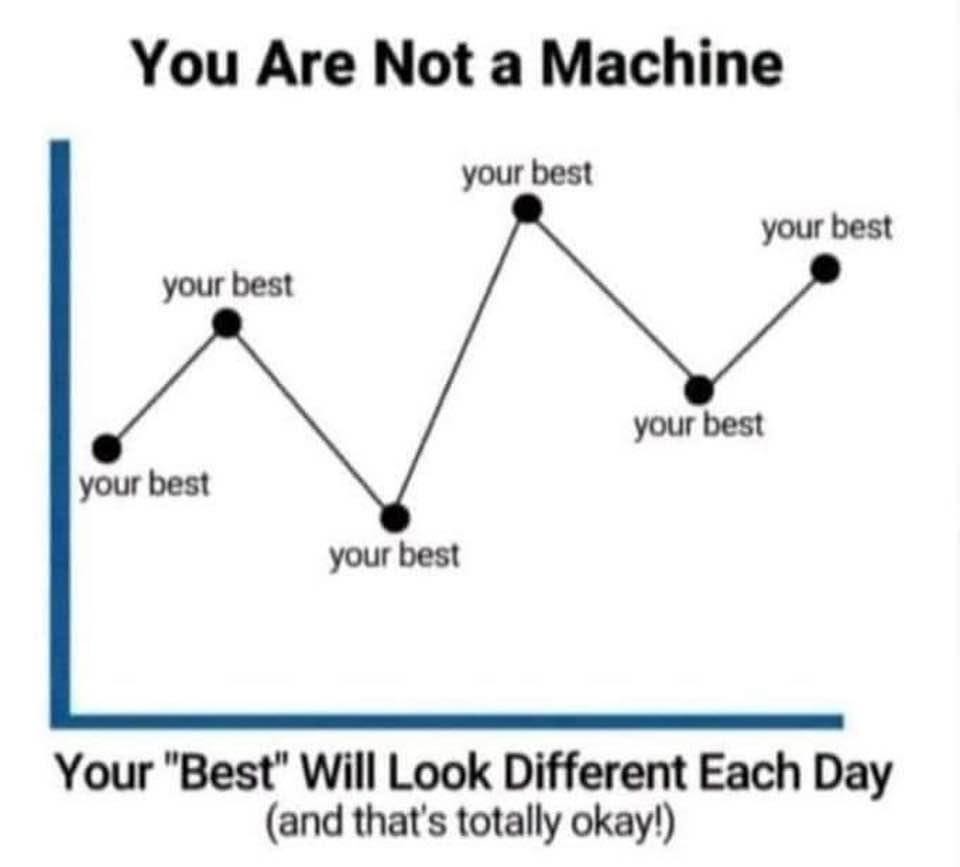

Give yourself a pat in the back as 2022 haven’t been an easy year for everybody. I know some who pass away because of COVID. I know some who are retrenched. I definitely know more than one person who had a mental breakdown. I would like to say that you have already done well. Your best will look different everyday.

Your Best Will Look Different Every Day

While 2022 is ending, there are some financial news that are still impacting our lives. I will be updating the 4 most impactful financial recaps that happened in 2022 and will continue to impact us in 2023.

2022 Financial Recaps That Will Affect You In 2023

#1: Increase in CPF Top Up Tax Reliefs

In 3 Key Changes To CPF Policies From 2022 (if you haven’t read, this is my top article of 2022), I wrote about the change in rules for tax reliefs for Retirement Sum Top Ups (RSTU).

In a nutshell, the amount of tax reliefs structure have been streamlined to be up to $8,000 (instead of $7,000). and this cap will now be shared between Special Account (SA), Retirement Account (RA) and the MediSave Account (MA).

If you are planning to RSTU in 2023, the new limit will be $8,000.

#2: Interest Rates Increasing

I believe the era of low interest rates will be ending and we are moving to a more “reasonable” interest rate ranges. This increase in interest rates have sent some shockwaves to the property market. On the flipside, this means that the interest in your bank account will finally increase.

Frequent readers of my blog will know that I share about the power of the R.E.V. strategy to increase cashflow from your bank accounts. However, as the rules of the banks keep changing, I have refocus my attention on getting more consistent returns elsewhere.

I check if there are changes among the bank multiplier accounts and will only change if the changes are drastic. Best High Interest Saving Account Singapore 2022 will give you a glimpse of what’s available now. I’m willing to bet that there might have already been some new changes already.

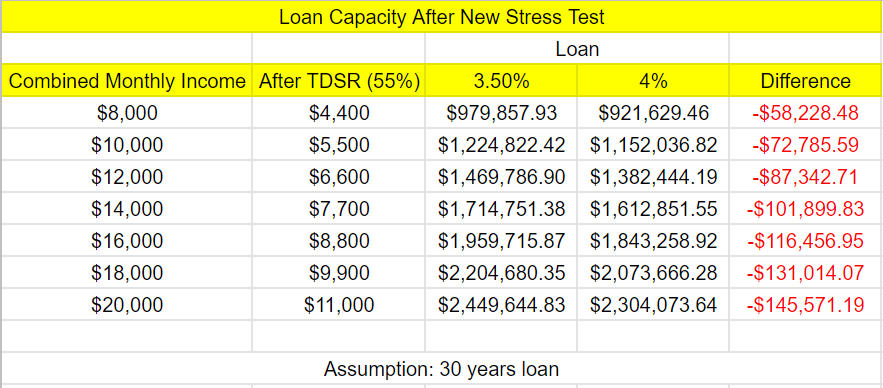

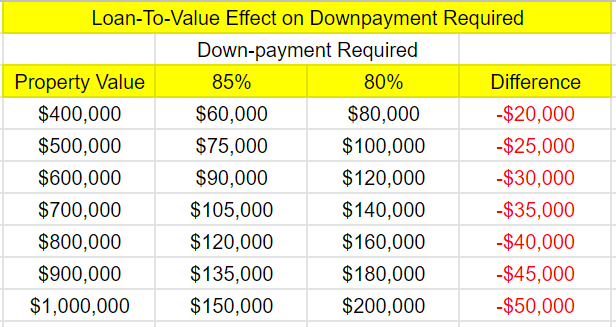

Loans will have a higher stress test. This will mean that you will get a lower loan amount if you plan to buy a house. If you are purchasing HDB, the loan to value have dropped from 85% to 80%, this mean that you have to increase cash payment by 5%

The one that got the most concern is of the 15 months waiting period for switching from private to HDB. While this has spooked the market. I believe there will be an increase in smaller condo units as a result.

#4: We Are Still in a Bear Market

I will share some statistic to give equity investors a glimpse of hope.

While we have obviously passed that date, this mean that we may be due for a recovery soon. (Disclaimer: this isn’t financial advice and just statistics).

The financial planning industry will evolve every year. While the rules of the game might change, it is vital to keep moving towards your end goal.

You are not alone in this. I suggest that you can consider to work with a trusted financial advisor that evolves with the economy. Otherwise, take time to read and understand the changes so that you can move towards your intended goal.

I wish you all the best. Take care!

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

While I believe that cooling measures are introduce to allow Singapore’s property market to achieve slow consistent growth, there will definitely be effects on homeowners, buyers and the renters crowd. I want to share 3 main implications of the new cooling measures done on 30 September 2022.

3 Effects of Property Cooling Measure Singapore

Higher Interest Rate To Calculate Loans

For property loans granted by private financial institutions, MAS will raise by 0.5%-point the medium-term interest rate floor used to compute the Total Debt Servicing Ratio (TDSR) and Mortgage Servicing Ratio (MSR).

For residential property purchase loans and mortgage equity withdrawal loans, they will using the 4% per annum (p.a.) floor (up from 3.5% p.a.).

3 Effects of Property Cooling Measure Singapore Maximum Loan Amount

Putting this into numbers, the maximum loan that banks will be able to provide will reduce by the following amount. Personally, I think there will be no major impact from this as the quantum for the properties are in the millions. This will affect buyers who will not be able to stretch (even more) when it comes to bidding for the property.

If asked if the interest rate floor will increase again, I personally don’t think so and likely to hover around the current rates. The MAS-MND-HDB have commented that “They (interest rates) are expected to rise further in 2023 along with US interest rates, before settling at a higher level compared to the lows during the period 2013 to 2021.”

Loan-To-Value from 85% to 80%

This is applicable for HDB housing loans only (Private LTV limit remains at 75%). This means the HDB buyers will have to increase cash downpayment by an extra 5%.

I believe this is aimed at HDB that are bigger in nature namely 5RM, Jumbo, Executive Apartments etc. In particular, this aims to reduce the raise of the million dollar HDB (231 Million Dollar HDB from Jan to Aug 2022). I believe the government intends for HDB to remain affordable and want to reduce the use of HDB to do speculation.

3 Effects of Property Cooling Measure Singapore LTV Effects

Personally, I think there may not be major impacts even for the higher quantum levels. You will also be glad to know that first timers or the lower income group will not be affected much by this because of the housing grants (up to $80,000) available for them.

15 Months Wait Out Period For Switching From Private to HDB

This is perhaps the most talked about measure as it will affect people is planning to sell their private property into a resale HDB. Currently, people who have private properties have to sell it within six months of the HDB flat purchase.

Now, there is a wait-out period of 15 months after the disposal of their private properties before they are eligible to buy a non-subsidised resale flat. This means that it will not be easy to move towards HDB. You will be glad to know that this is a temporary measure.

You will also be glad to know that this will not affect those age 55 and above who is choosing to downgrade at that time**.

I believe there will be 4 main effects of this.

#1: There will be an increase in demand for smaller condo units. If people who do not want to wait for 15 months, they may consider to downsize to the smaller condo units. I believe transactions (perhaps price) for 2BR to increase in the months ahead.

#2: There will be an increase in demand for 4BR HDB resale units. For people age 55 and above, the 15 months wait out period will not apply to them** if they shift to a 4BR HDB or smaller.

#3: In general, lower transaction as the buying pool has shrunk. I believe that over the next quarters, the overall transaction might be lower as HDB upgraders will think twice. This reduces the effective buying pool.

#4: In general, rental rates will increase.

Final Thoughts

I believe that the government is planning for a sustainable and gradual growth of property prices. The emergence of million dollar HDB, the increase in property prices and the increase in interest rate calls for prudence for financial planning.

Property play a big role in our financial planning. It will be prudent to understand your own financial situation before making a decision into the market. It is also important to remember that other asset class (eg: insurance, estate planning, equity investment) should be taken into consideration when planning for your financial future.

I wish you all the best. Take care!

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

The Future Is Here – A Book Review on “Futureproof – How To Get Your Business Ready For The Next Disruption” by Minter Dial & Caleb Storkey

Futureproof How to Get Your Business Ready for the Next Disruption

Foreword: Special thanks to Chengkok for giving me the opportunity to read and write a review for this book. The contents expressed are of the author’s own opinions and are in no way meant to serve as financial advice. Written By Minhui.

Introduction:

The book is split into 2 parts, the first part focuses on the mindsets that will help to embrace disruptions to become “futureproof”. The three mindsets are namely: meaningfulness, responsibility and collaboration.

The second part focuses on 12 of the prominent driving technological disruptive forces across the various industries. Minter and Caleb use humour, personal experiences and passion to bring across important lessons of disruptions for businesses today.

Part 1: The 3 Mindsets

Meaningfulness: The desire to find purpose is not something new, in fact, I argue that it is deeply rooted in human nature for one to search for meaning to have something to live for. Meaningful work helps us to lead more rewarding lives. As such, Minter and Caleb have outlined a framework of 5Ps of meaningfulness for businesses. The 5Ps are Purpose, People, Prize, Profit and Planet. It is with these 5Ps that businesses are able to position themselves in a different light from the others and contribute back to society purposefully. Meaningfulness helps a business to attract the right people who share the same values to scale to greater heights, making profits whilst balancing a higher goal of sustainability for the environment and impacting people’s lives positively.

Responsibility: The need for accountability is greater than before as disruptions take place, with disruptions, we are being exposed to consequences that we may not have answers to yet. Take the example of the debate over genome-editing, the benefits are clear, we could potentially create humans free from diseases but what happens when the gene-editing process goes wrong? Moreover, there are concerns over the justice and equity of access to such technologies. Hence, the moral permissibility of such technologies should be part of the public discourse. Responsibility is essential to a business in that it influences the ultimate purpose of the business and the ethics behind the means to achieve the goals.

Collaboration: No man is an island as the famous adage goes, the need for collaboration has been emphasised through the interconnectedness of today’s world. No one can be an expert in every field and accomplish everything by himself. By being receptive to others’ ideas, collaboration allows the cross-fertilisation of ideas and helps businesses to be more nimble to gain a competitive advantage. Sharing economies utilises collaboration very well, disruptive companies such as Airbnb in fact is asset-light as opposed to traditional hoteliers. Airbnb serves as a platform for connecting accommodation seekers to renters, making under-utilised spaces productive. In this example, collaboration requires much trust from both parties. Trust is a currency that is earned through the fostering of a collaborative culture and not commanded immediately. Businesses have to leverage on each other’s specialisation for greater efficiency.

With that, these three mindsets are crucial in helping you to harness the opportunities from disruptions and “futureproofs” you as you will be better prepared when you question the meaning of your actions and factor in the responsibility behind the actions taken. Lastly, a collaborative spirit should always be encouraged as it helps us to be open-minded for opportunities.

Part 2: The 12 Disruptive Technological Factors

The Web

The Smartphone

The Cloud

Security

Internet of Things (IOT)

Artificial Intelligence (A.I)

Big Data Analytics

Blockchain & Cryptocurrencies

3D Printing

Energy Storage

Self-Assisted Driving

Genomics

I will not be delving deep into each of the 12 disruptive forces but will instead leave it up to you to do your own research or read the book for a deeper understanding. Minter and Caleb have pointed out these 12 technologies that will (if they are not already) disrupt businesses. Some of these forces are in fact intertwined.

The worldwide web became publicly available on 6 August, 1991. Much has changed since then, with its ever-increasing speed and ubiquity, it has allowed us to be reliant and engaged in it like never before. The plethora of tools made available by the web such as social media, e-commerce, peer-to-peer funding or marketplace and e-learning have been nothing short but amazing. It has simply changed the way we live, communicate and handle our daily tasks.

Next, the smartphone, has vastly improved over the years to allow it to function like a mini-computer in which we are able to conduct transactions, communicate with people and get a daily dose of news from Wealthdojo. The third disruptive force would be “the cloud”, which has enabled us to store our data on the internet instead of having it stored locally on a desktop or phone. This has allowed us to work from anywhere and share access to edit documents together with our colleagues who might not be in the same location as us, thus, boosting productivity for companies and institutions.

Cyber security is the protection of computerised systems from theft, corruption, or disruption. From individuals to corporations and governments, the importance of cyber security cannot be understated. The global cyber security market is estimated to be projected at USD 500.7 billion by 2030 according to research by Grand View Research Inc. The internet of things (IoT) are objects that have sensors to communicate both with one another and with us. IoT helps businesses to provide and deliver more customised, contextually relevant content and enhanced customer experience through data analytics. This will be explored further.

The sixth disruptive force is Artificial Intelligence (AI), it is the development and use of machines to function in ways normally associated with the cognitive functions of the human brain. These technologies include: 1) Logic programming- using facts and rules to create logical formulas, 2) Bayesian systems- using statistics and probabilities for prediction. 3) Expert systems-using knowledge-based systems for decision making 4) Semantic knowledge bases – understanding language sets, identifying content by its types, meaning, metadata or tagging. 5) Deep Learning – using algorithms to create models of high-level of abstractions. Being a laggard in adopting AI could jeopardise your businesses. Big data analytics is a function of the combined forces of the web, smartphones, IoT, the cloud, AI. What makes big data powerful is not the data itself but rather what one plans to do with it. It is crucial for companies to know how to navigate through these data to assist their decision-making process.

The eighth disruptive force is one that has been making headlines in recent days. Cryptocurrencies are digital currencies, operating independently of any central bank and through digital encryption, the transfers of these currencies are self-regulated. The most disruptive element of the cryptocurrency force is the underlying blockchain technology. Blockchain, operates as proof of existence. Laura Shin from Forbes wrote “Blockchain technology is likely to disrupt financial services first by making existing processes more efficient, secure, transparent and inexpensive”. Now, with the arrival of the metaverse, blockchain technology will become more significant, as cryptocurrencies and non-fungible tokens (NFTs) will enable purchases and value storage in virtual reality. Gartner forecasts that the business value generated by blockchain will grow rapidly, reaching $176 billion by 2025 and $3.1 trillion by 2030.

Next, 3D printing is the construction of a three-dimensional product from a CAD model. There are many exciting applications for 3D printing. Examples, where 3D printing could be use, includes:

Rapid prototyping

Quick design iteration

Low volume production

Mass customisation

Virtual inventory

Prosthetics

Production of less common spare parts

Renewable energy is hugely beneficial for the environment, however, one of the big challenges to such alternative energy sources is the storage for it. This is due to the intermittent nature of the generation and the inadequacy between when it is created and when it may be needed. Today the mechanisms to store this energy effectively and cheaply remain to be developed. Energy storage is a good example of how all the changes identified by the authors, will not all have direct relevance for all businesses. However, it is of concern to businesses that are involved in producing and storing energy, or those that are heavily energy-dependent.

The eleventh disruptive force is self-driving which enables vehicles to use a combination of sensors, cameras, radars and artificial intelligence to travel between destinations without a human operator. Tesla, has arguably been leading the way with its large fleet of electric vehicles, and more companies such as Volkswagen and Rivian, have jumped on the bandwagon in a bid to achieve a slice of the pie

Lastly, Genomics which is the twelfth disruptive force is the study of the full genome, including all genetic material. Roughly, 2 per cent of our genome is allocated to genes that ‘code’, with the function of programming or encoding a particular product. The study of genetics remains embryonic for businesses outside the medical sphere, nonetheless, the analysis and interpretation of epigenetics (the study of changes in organisms caused by modifications of gene expression rather than alteration of the genetic code) brings the hope for greater robust business applications. Although businesses’ relationship with genomics is in its infancy stage, we can expect to see significant changes in this area in the upcoming years.

Conclusion

These 12 forces of disruption are just examples that Caleb and Minter have pointed out to keep a look out for in the coming decade, they might not be relevant for every business out there, but one takeaway from the book is that we should embrace disruptions as opportunities and prime ourselves for changes.

Humans are more adaptable to changes than perceived, Covid-19 has been a good example, working from home may have been unimaginable for most companies pre-covid but the nationwide implemented circuit breaker has forced most of us to adapt to a whole new working environment at home within such a short period of time, and very likely this new normal is here to stay. More companies have called for a permanent work from home (Twitter, Spotify and etc.).

This book cannot make you “futureproof” but it will open your mind to think about how to do so. Companies and individuals should carry out an honest assessment of ourselves for the mindsets that are required to embrace disruptions as discussed in part 1 because we simply cannot afford to be slow to react to the disruptions that will continue to change the way we live and work in the future.

Final Thoughts

Thank you Minhui for writing this lovely book review.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

In the most recent webinar that I conducted, I asked the participants what are they concerned about when it comes to investing in the long run?

I thought that most people’s answer would the lack of time or the inexperience in the market. It turns out that for most people, they are not too sure if they are doing it right.

Why is it not easy to invest in the long run

If you think about it using a proxy, it is like a person driving on the roads but unsure if they driving properly. If this is not risky, I don’t know what is.

The Why

Fear Of Missing Out FOMO

As we get more plugged into the internet, social news gets spread very quickly. With more people getting stuck at home during the COVID-19 period, we log in more to these social platforms to keep updated on the world around us.

One popular topic is how people are getting rich during the pandemic. Topics like Bitcoin, NFTs, Value Investing or Growth Investing gets thrown around. Because it seems that every Tom, Dick and Harry is doing it, people fear missing out and started participating into these.

Redefine Basics

Investing is the act of allocating resources (usually money) to buy an asset, in hopes of reselling it later at a higher price (Definition from Investopedia).

For most people, they get the concept that they will make money when the price goes up. I believe there is a certain form of Social Investing (a term that I just made up) going around in the recent market. Reddit has made certain stocks like Gamestop pop. Elon Musk has certainly contributed to the popularity of Bitcoin and Tesla. One thing for sure is that prices seems to be influenced by social pressures.

While it has created some millionaires, some people are unsure what they are doing anymore.

The art of investing starts from buying an asset. This concept seems to have lost its’ way in this season.

Our Mind Plays Tricks

Let’s play a game. Find a place to record your answer for Quiz A and B.

Quiz A

Choice #1: You get a 100% chance of getting $50.

Choice #2: You get a 50% chance of getting $100, 50% chance of getting $0.

Write down which one will you choose?

Quiz B

Choice #1: You get a 100% chance of losing $50.

Choice #2: You get a 50% chance of losing $100, 50% chance of losing $0.

However, if you understand it mathematically, you should be indifferent between all the 2 choices in Quiz A or Quiz B. The expected value of both Choices in Quiz A are the same (i.e. +$50), while the expected value of both Choices in Quiz B are the same (i.e. -$50), so there should be no difference (at least mathematically) between the Choices in either Quiz. (Thank you Kok Ming for your help)

This tells us that as humans, we feel losses more keenly than gains (loss aversion). That’s probably the reason why you might have taken gains off the table early out of fear and hold onto large losing positions in the hope that they will rebound.

Our minds are not wired to maximise performance but to minimize regret.

Anyway, that’s just one problem. These are other cognitive bias we need to overcome as investors.

Cognitive Bias Investing

So What Can You Do?

Now that you understand that the society and your own mind is against you, what can you do? I would humbly like to suggest 3 steps.

#1: Get financially educated and informed of the investment process.

#2: Focus on the controllable.

#3: Consider a multi asset class portfolio to minimise drawdown.

Why is it not easy to invest in the long run education

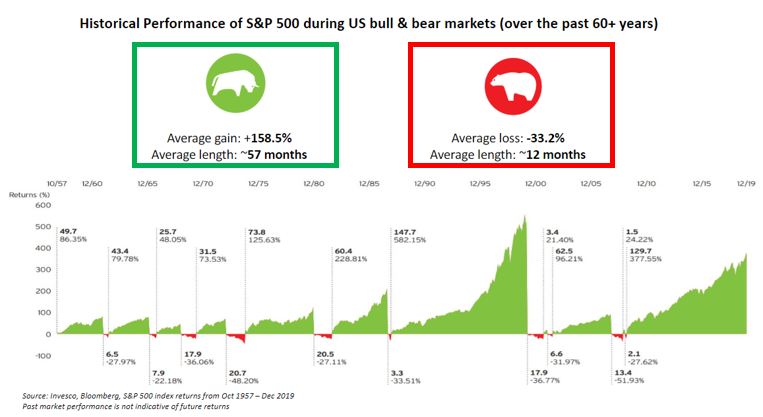

This graph records the S&P500 gains and losses over the past 60 years. The stock market can be considered like the following season (Spring and Winter). The average period for Spring (we love Spring don’t we) is 57 months and the average period for Winter (we don’t like the cold) is 12 months.

IF we are in a crisis now, it typically takes around 12 months before it is spring again. In the more recent COVID-19 crisis, the winter lasted around 6 months (Feb21 to Aug21) before roaring back into Spring again.

It is what you do during winter that determines your financial results. Getting financially educated allows you to prepare for such opportunities.

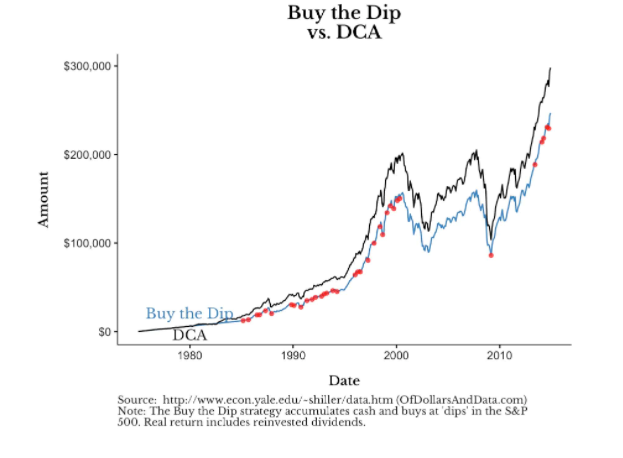

Dollar Cost Averaging VS Buying the Dips

Let’s assume that you can predict each and every dip (technically impossible) and buy them (further assuming you have the mental resilience to buy at the lowest). Do you know that Dollar Cost Averaging (DCA) beats buying the dip in this time period? Instead of focusing on the unknowns or black swan events, why not focus on what’s controllable which is doing simple Dollar Cost Averaging?

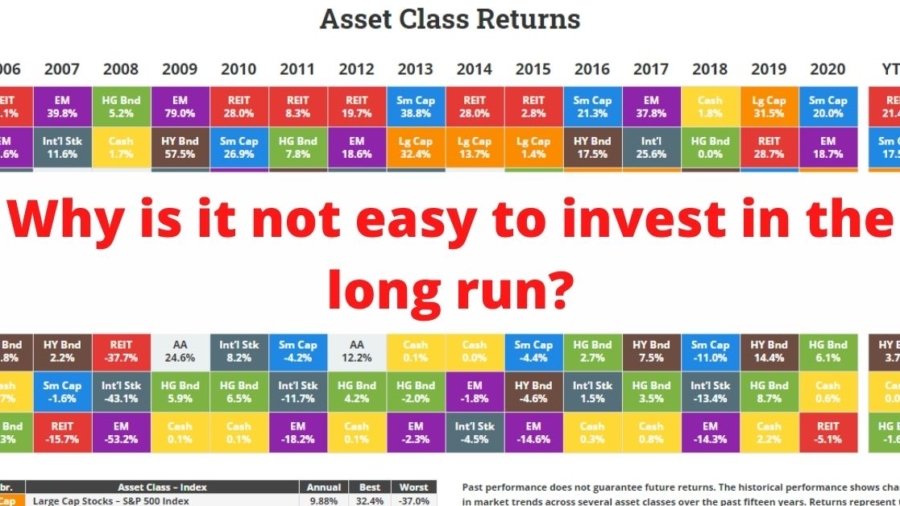

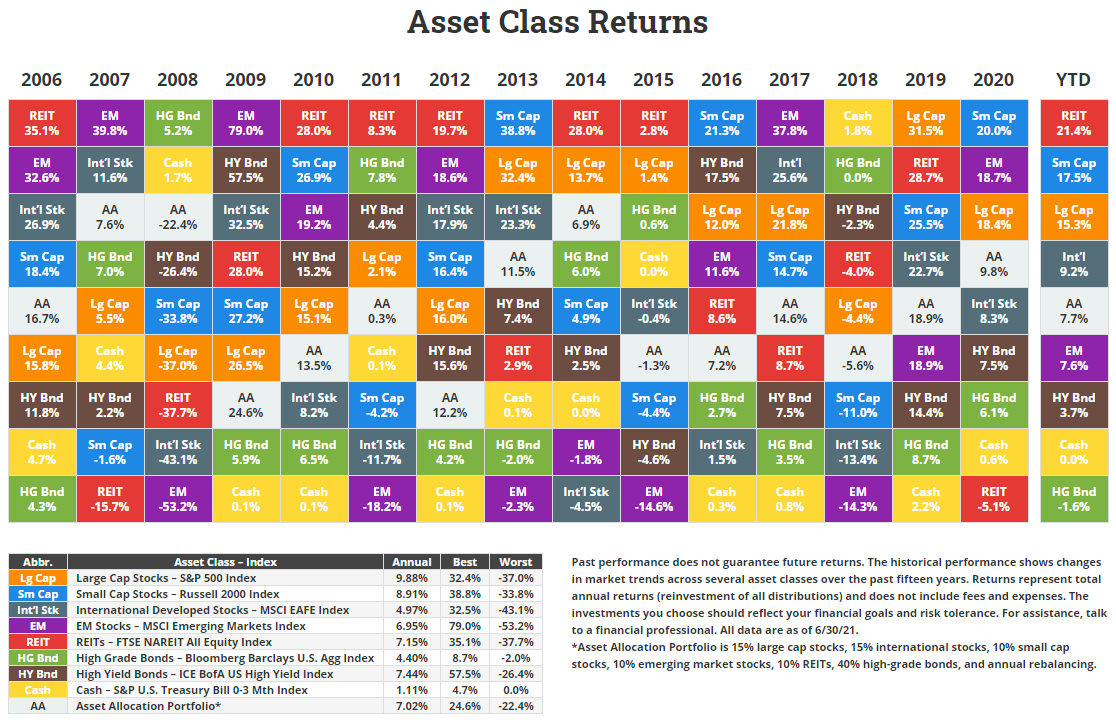

As you can see, different asset class performs differently every year. Because our minds are loss averse in nature, we might not be able to weather through each storms if we are only into one asset class. Consider a multi asset portfolio might make it easier for our minds to weather through each storms when it comes.

Final Thoughts

Personally, I’m invested in the long run. In investment, there will be volatility and it is something we have be comfortable with either through education, experience or both.

Do you related to the above? Let me know in the comments below.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.