If you are in cash this year, you would have beaten the market. Congratulations! However, this does not mean you should keep your money as cash as inflation will erode the value of your money.

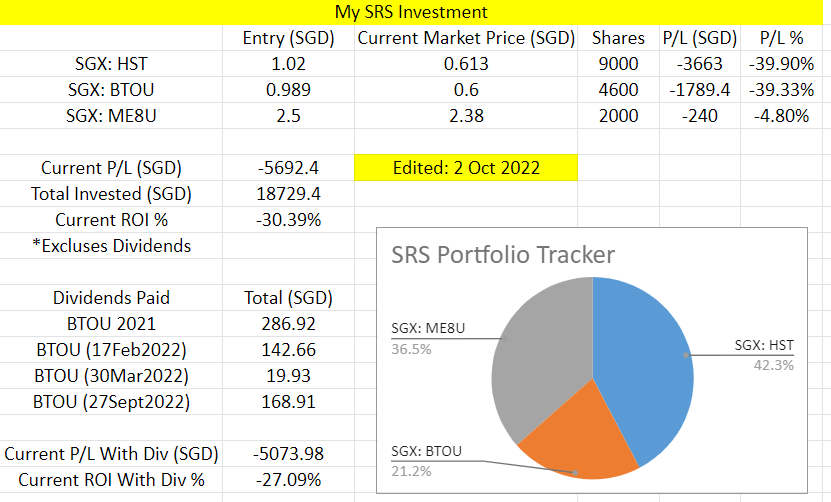

2022 is a rough year for the investment market. If you have invested in the STI for the past 1 year, you would have achieve no movement at all.

STI ETF Since March 2022

If you have invested in other markets, then you are most likely seeing a red in your portfolio.

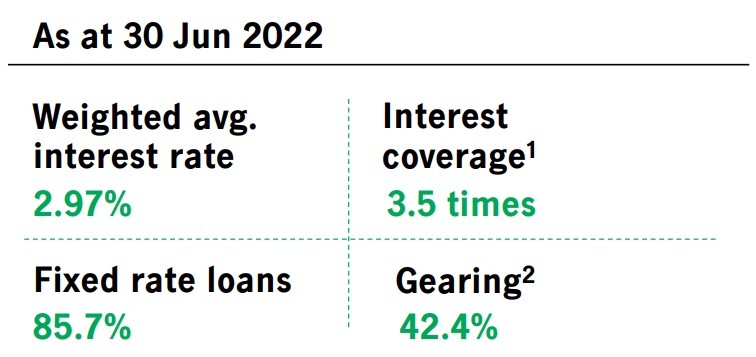

SGX: BTOU slides even further in the last quarter. I believe the main reason is because the FED has raise interest rates to combat inflation. This has made borrowing more expensive and may be a cause of concern for investors. However, it is worth noting the Fixed Rates Loans makes up 85.7% of their debt profile as of 30 June 2022 and isn’t a great cause of concern. BTOU is in a midst of transformation as explained in June 2022. I will be reading closely to this in the quarters ahead.

Manulife US REIT BTOU Debt Profile June 2022

SGX: ME8U is a new entry into the SRS portfolio. I was eyeing Mapletree Industrial Trust for a long time. It was a stock that I was interested in even before COVID-19. MIT’s property portfolio comprises of 143 properties ranging from light industrial buildings, stack-up buildings, flatted factories, business park buildings, Hi-Tech building and recently data centers.

Mapletree Industrial Trust portfolio growth in IPO has been amazing with a new position into Data Centre. Looking forward to its’ performance in the years to come.

Mapletree Industrial Trust Portfolio May 2022

I have also invested a small amount into a 3 year endowment with a guaranteed of 3%. As this is a very straightforward proposition, I will not be updating this particular segment.

Final Thoughts

Quarter 4 is the best time of the year to think about SRS contribution. The main reason for SRS contribution is to reduce your tax payable for your FY2022. You then need to consider the investment portion thereafter. I will be running a webinar on SRS tax reduction in the months ahead.

Do comment below and I will individually send you an invite for the event.

Meanwhile, take care and hope you are well.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

I never thought there will be a day the banks will adjust their interest rates upwards again(DBS, UOB, OCBC). In 2018 period, the local banks came out with a great marketing program to give higher interest. It was heavily discussed. However, it was short lived as the banks slowly reduced the amount of interest.

Learning from the past lessons, I view that this interest increase as temporary in nature and you shouldn’t base your long term planning (insurance or investment) to increase your interest in your bank account.

In this article, I will take on several assumptions to decide which bank account is the best for you in 2022.

Best High Interest Saving Account Singapore 2022

Assumptions Taken

Only DBS, UOB and OCBC will be taken into consideration

Based on the marketing message, OCBC sounds the best. It is also good to know that OCBC changed their program 1 month after DBS and UOB have made changes.

First Elimination

With our assumptions, we feel that DBS multiplier is the worst out of the 3.

Based on our assumptions, we will only hit 1 category in DBS multiplier. I feel that we shouldn’t increase our transaction categories just for the sake of the higher interest.

Effectively, there will be a higher interest on the first $25,000. Your interest of 1% will give you $250 annually.

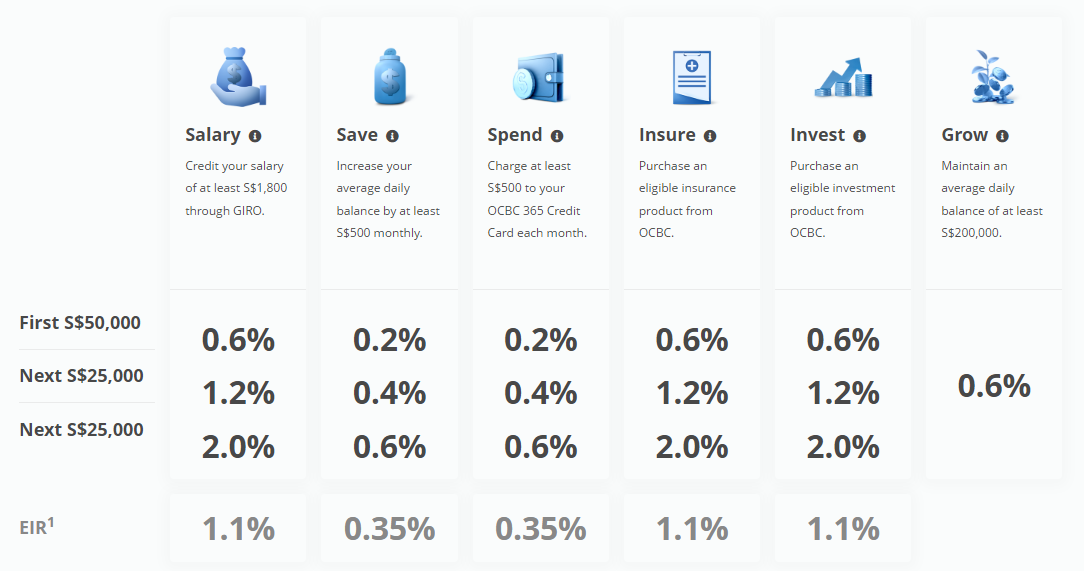

Best Fuss Free Bank Account: OCBC 360 Account

OCBC is rank the best fuss free bank account in my opinion as they follow a very simple interest tier model.

OCBC 360 Account Interest Tiers

Following our assumptions for using only salary crediting and spending on credit card, the effective interest rates (EIR) 1.5% resulting in an annual interest of $1500.

However, I like this more as this is fuss free. If you don’t want to hit the credit card spending of $500 monthly, the salary option will have an EIR of 1.1% resulting in an annual interest of $1100. This is great for people who do not want to keep track of their spending for the sake of the extra interset

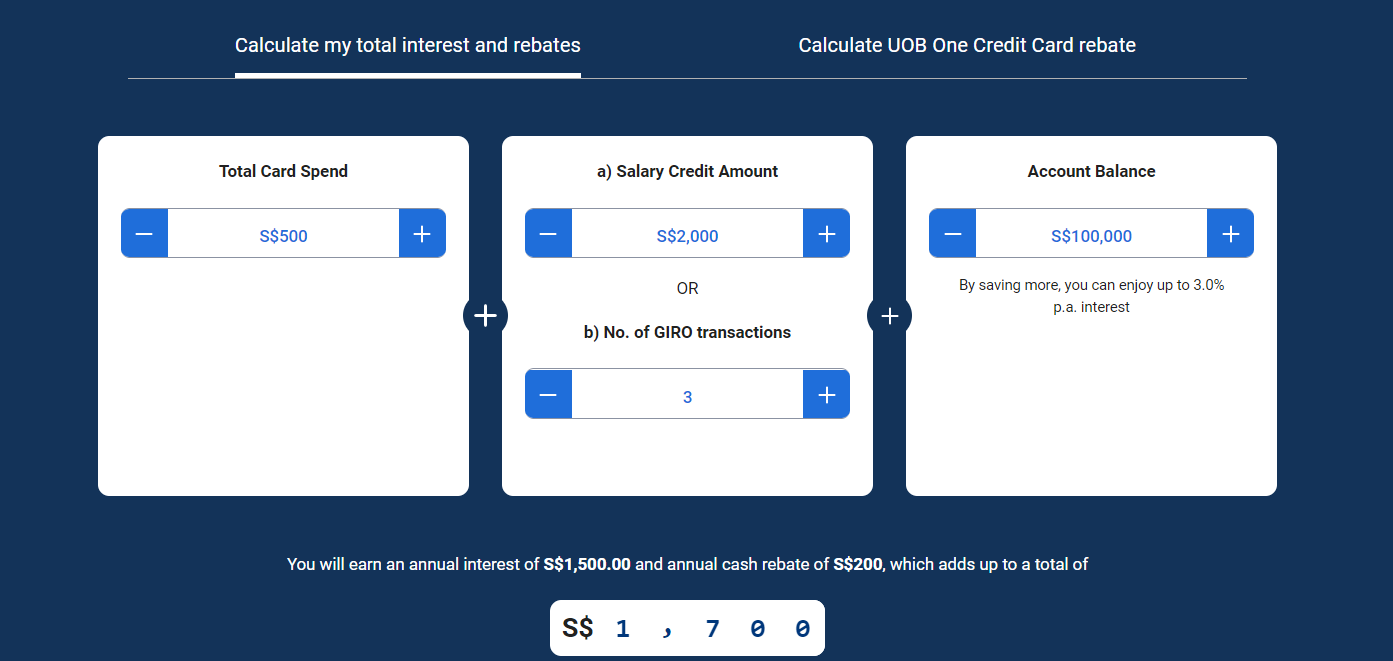

Best Higher Interest Bank Account: UOB One

UOB and OCBC comes up very close but UOB wins because of the ease of understanding of their UOB one card.

UOB One Account Interest Tiers

The emphasis of UOB is the credit card spend. If you do not hit the minimum of $500/month, then the interest be affected. Hence, this will only work if you are certain to be able to hit the monthly eligible credit card spend of $500.

The total annual interest (inclusive of cash rebates) from UOB One account and UOB One Card is $1,700 making this the best higher interest bank account for now.

Final Thoughts

There you have it. Personally, I’m went with the OCB 360 account because of the ease of use.

I believe that choosing your bank account is one of the first steps to plan for your finances. At the same time, I will avoid buying products just to get that extra bit of interest as the interest might change in future again.

That being said, you should always have a long term perspective when it comes to planning. I will recommend you to use the retirement calculator to have an idea how much you need for retirement.

I wish you all the best! Take care.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

In 2022, I having more conversations with my clients whether they should increase their retirement sums due to inflation. I begin to realize that it is not easy for them to project their future needs when they don’t know the perimeters needed.

Hence, I have build up a quick calculator for them to calculate in less than 1 minute how much they need and how much they have to invest NOW to achieve their retirement goals.

Retirement Calculator Singapore

The Assumptions

Behind every model requires a few assumption. I will go through the ones that require more thought process.

Replacement Ratio

This is the percentage of income to maintain lifestyle. Most studies suggest aiming for a target of between 70 and 85 percent of pre-retirement income. Typically, most of us spends a certain portion of our income to maintain our lifestyle. Some of us will spend more, some of us will spend less. To most of us, our spending habits will stay with us for a long period of time.

For Example: Peter earns $6K monthly and spends $4K every month on household needs etc. This means his replacement ratio is roughly 67%.

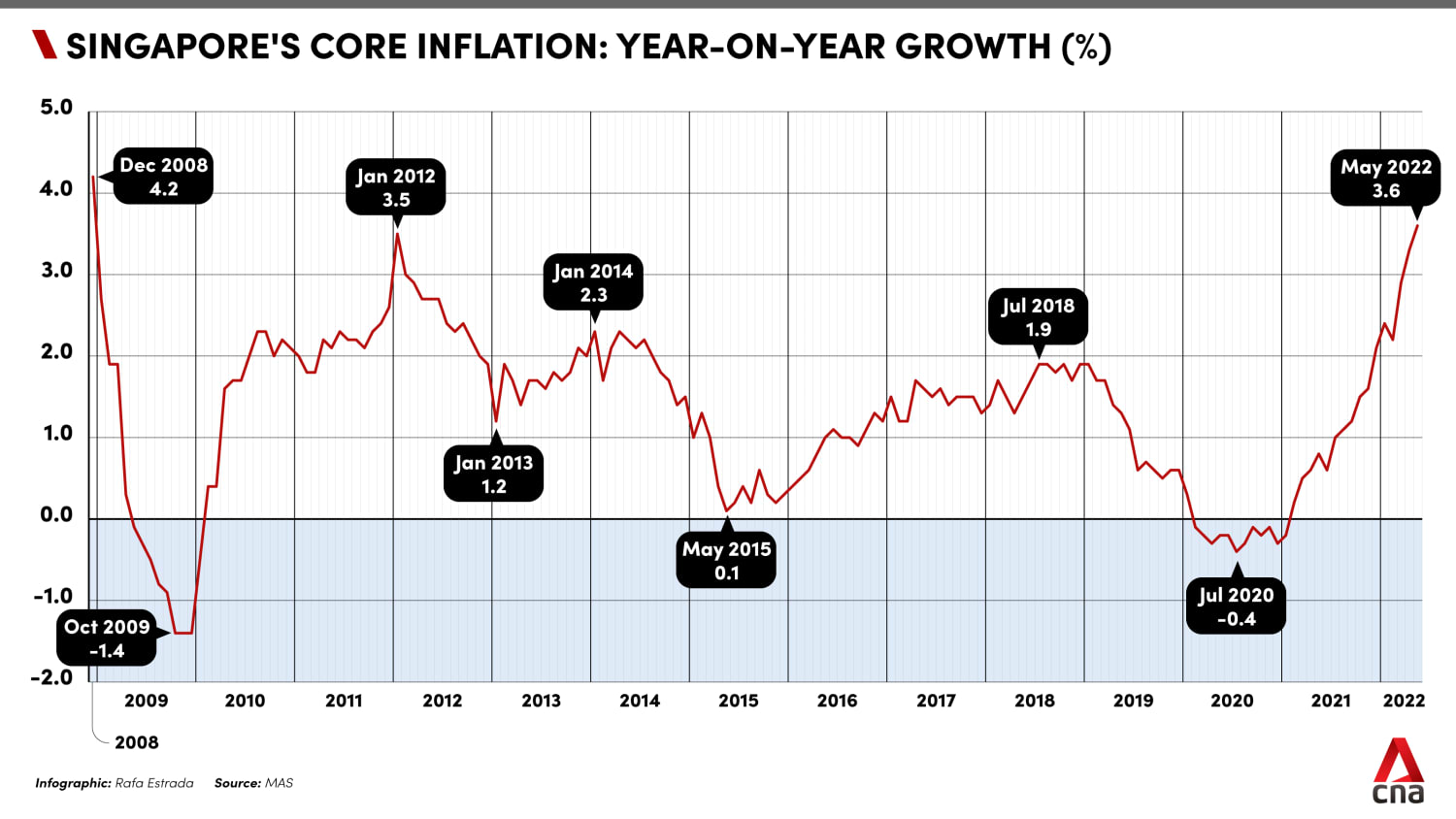

Inflation Rate

Though this is well defined, it is not easy to determine a meaningful figure especially when inflation has been going up in the last few months. From the graph below, you can see that we have spikes in inflation previously. However, it has been maintained at a certain level for prolong periods of time.

This is the rate that you want your investment to grow yearly to reach your goals. For this to be effective, it would be easier to attribute it to your risk profile which will then lead you to the appropriate investment instrument you will find suitable.

If you are someone who is risk adverse, you might consider fixed deposits which typically gives around 1% per annum. For Singapore bonds investment, the yield typically is around 2% to 3% depending on the tenure of the bond.

Taking a pause here, all forms of investments carry risks, including the risk of losing all of the invested amount. Such activities may not be suitable for everyone. With an additional disclaimer, the above doesn’t represent a buy/sell/hold recommendation.

The Retirement Calculator

Final Thoughts

I think planning beyond 2022 will be an interesting discussion as we are in midst of existing developments (Russian-Ukraine, China-Taiwan, Monkeypox, COVID19). However, we should let it stop us to plan consistently for the future.

If realised you have a retirement shortfall, congratulations! It is time to do something about it. There are various instruments available and I will be glad to have an open conversation with you on how to do that with you.

If you feel like something needs to be done, the next place you need to go to is here (to read more) or simply contact me using the information below.

I wish you all the best! Take care.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

2021 has been a year of transition. Singapore had quite a successful period and was enjoying limited COVID-19 cases until Delta and Omicron arrived. There were restriction imposed on the number of gatherings (2pax and 5pax rule) and it was phrased out in 29 March 2022. If you have already forgotten, there were two lockdowns from 16 May 2021 to 13 June 2021 and 23 July to 9 August 2021.

Essentially, we were in a cha-cha mode where the economy trying to get off its’ feet.

The mission of Wealthdojo is still the same. We serve to educate and debunk the “free financial advice” that was given without context.

Key Metrics (Unaudited) in 2021:

51 claims (Top claim $47336.59 for critical illness)

> $100,000 paid out in claims through their insurance program

51 Articles written (Year 2021)

3 High Quality Webinars

Achievements in 2021:

Achieved MDRT (Top 5% Financial Consultants World Wide)

As I look back at 2021, there were many shortfalls. Moving forward, there will be more done to impact the financial literacy space in Singapore. 2022 will be the year of creation.

Wealthdojo Junior (Pilot): Financial Literacy for Juniors

Inspire 30 new families to work on their financial journey

Continue being MDRT in 2022

One Last Story:

2 old man were discussing about their retirement life. Both had the same skillsets and started working at the age of 20. They both saved $30K by the time they were 30 years old. Old Man 1 used the money to invest in the stock market while Old Man 2 used the money to buy a car.

Everyone congratulated Old Man 2. For years, Old Man 2 was seen to be successful and Old Man 2 felt very happy.

Today, Old Man 1 is living in his fully paid condominium, he fulfilled his CPF-FRS and have an investment portfolio generating dividends for him. Old Man 2 is living in his fully paid HDB, he fulfilled his CPF-BRS and have some savings in his bank account. His car is now worth zero (scrapped since years ago).

Old Man 2 was livid and complains the rising cost and about how the government is not doing enough to help them. Old Man 1 sipped his coffee calmly and said “You always had a choice. You chose your life when you were 30 years old”.

Choose wisely. Hope you contribute to your choices in the years ahead!

Wealthdojo Annual Report 2021

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

I don’t think I have to repeat how bizarre is the world is right now. After contracting COVID19, I sat down (actually slept down most of the time) and thought long and hard about how financial events are shaping our economy now.

There are events in the world and many are definitely out of our control. However, some of the effects will be trickled down to be felt by us. I will be talking about my thought of the 3 most important financial events that will affect us, inflation, interest rates and wages.

Disclaimers: All thoughts are mine alone. Though I would love to hear yours in the comments section below.

What will happen after 2022

Inflation

This is Singapore’s annual inflation rate over the past 25 years. As Singapore is only independent for 57 years, this data is what Singapore has been facing half the time. You can see for majority of the time, inflation was “well behaved” at 2%. The exception would be spike in 2008 (Financial Crisis) and for a period between 2011 to 2013.

I predict (mainly because of the lack of data and research) that we will be having a inflation > 2% for at least another 2 years before it gets back the usual range. I don’t think prices will fall when inflation becomes lower. Hence, make it a point to preserve the value of your money. This is especially important if you are nearly retirement or at retirement.

Interest Rates

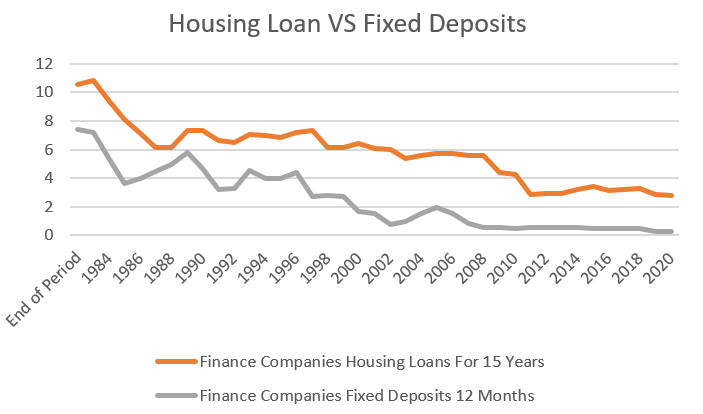

Graph 1: Singapore Housing Loan VS Fixed Deposit Trend

Interest rates affects various financial instruments and in the graph above. I’m hearing a lot of chatter on 4 things on the ground.

Housing Loan

When interest rates raise, housing loan rates also raises. As you can see above, the last 10 years we were living in a low interest rate environment. In the last few months, home loans are starting to move upwards to 3% (fixed rate). The implication of this is a cashflow drain.

Imagine you are servicing a 30 years housing loan of $800,000 at an interest of 1.1% previously. Your monthly mortgage works out to be $2610.

At 2%, your monthly mortgage is $2957. This is an increase of $347 monthly or $4164 annually.

At 3%, your monthly mortgage is $3373. This is an increase of $763 monthly or $9,156 annually.

Can you see why people are worried when rates increases to 3% now?

If you are looking into floating rates, Singapore is using SORA now. SORA is 0.8089% p.a. (as at 4 July 2022). A typical spread of banks would be between 0.8% to 1.2% depending on your relationship with them. I would expect the floating rates (including spread) will be between 2% to 4% in the next 2 years.

Fixed Deposits

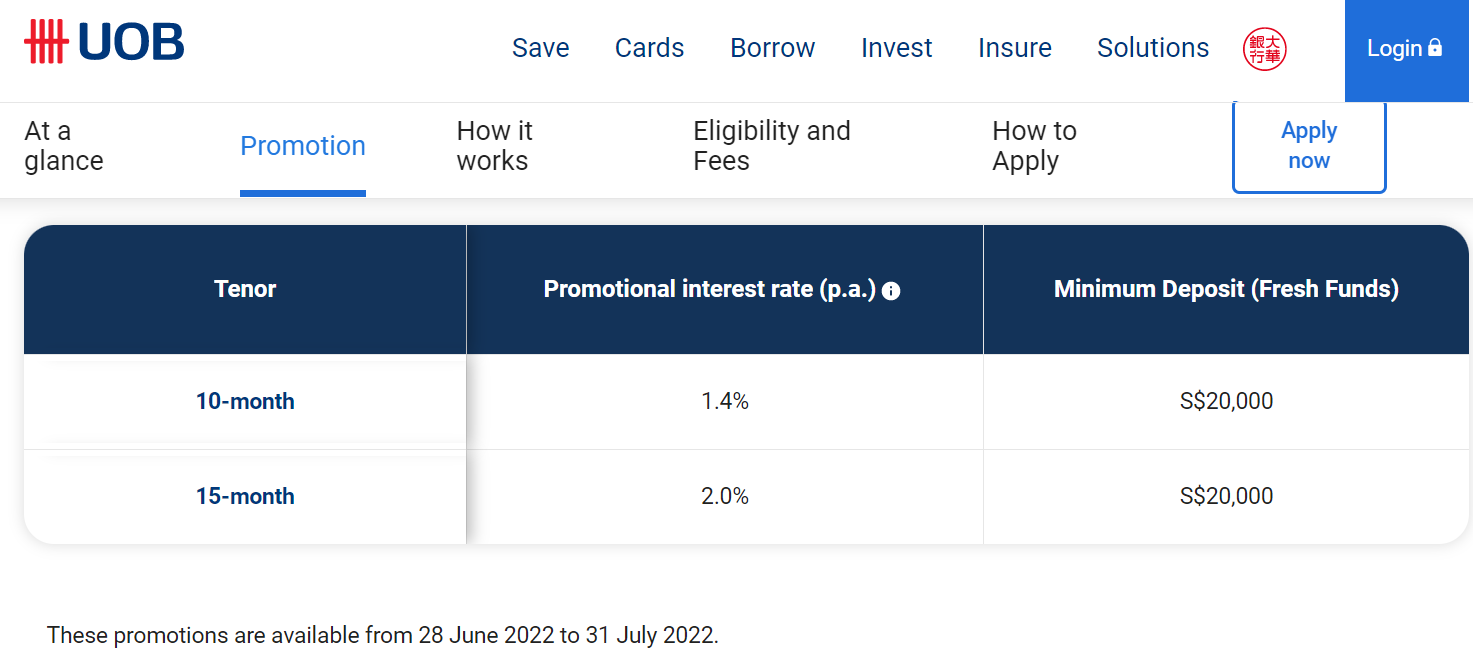

Hurray to those of you who are cash rich. Guaranteed rates never look better. We are seeing fixed deposit rates increasing with UOB giving 2% for a 2 year lock in. Other banks are also stepping up their interest rates too.

Disclaimer: This is by no means a buy/sell recommendation

UOB Fixed Deposit July 2022

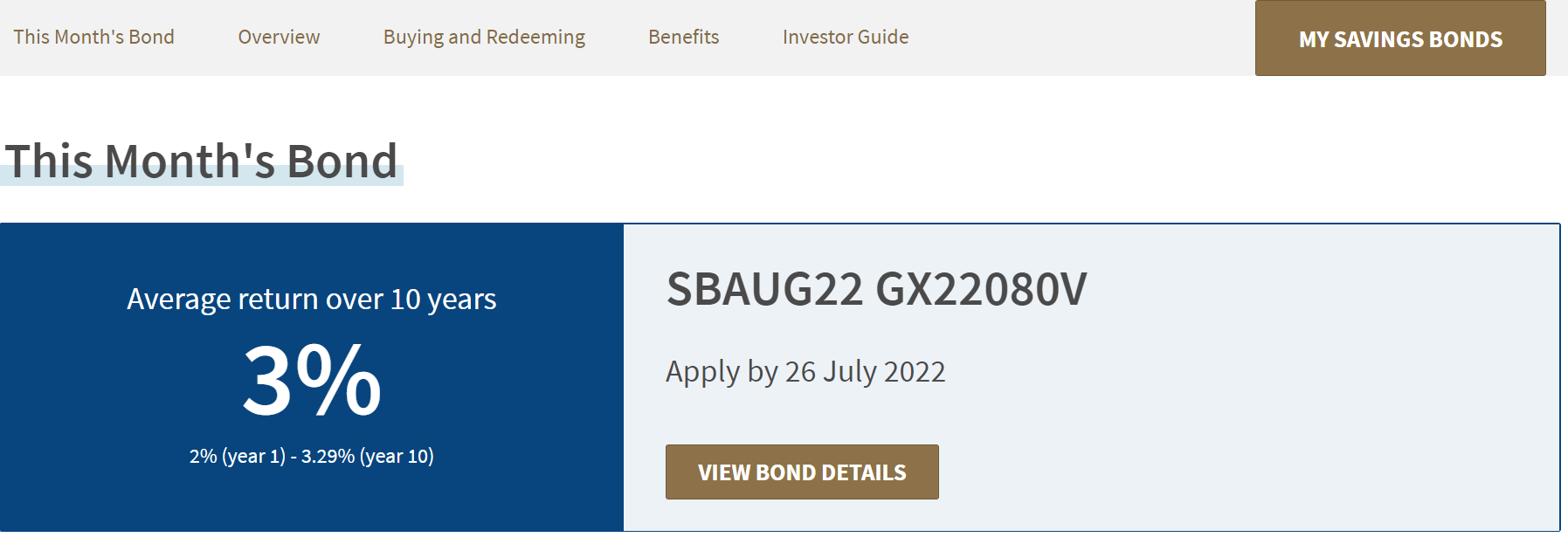

Even the Singapore Saving Bonds are giving average 3% returns in July 2022.

Singapore Saving Bonds July 2022

Looking at data, I’m concerned as the Housing Loans (15 Years) and Fixed Deposit (1 Year) are highly correlated (see graph 1). The average difference between housing loan and fixed deposit over the years is 3.3%. This means that if Fixed Deposit is 1%, there is a chance that the housing loan could go to 4.1%.

The industry has realigned expectations in July 2021. The upper illustration rate will be capped at 4.25 per cent a year, down from 4.75 per cent, and the lower illustration rate will be capped at 3 per cent a year, down from 3.25 per cent.

The previous rate change was in was in 2013, when the upper illustration rate cap was reduced from 5.25 per cent to 4.75 per cent a year. The lower illustration rate was reduced from 3.75 per cent to 3.25 per cent.

The main reason was because of the low interest decade that we were living in.

Now that interest rates are moving up, will insurance companies increase the rates in the participating policy again?

CPF Interest Rates

In a low interest environment, our CPF interest rates looks like an attractive place to reap guaranteed interest (we are leaving context aside for this statement).

Imagine if fixed deposit rates are nearing 3.5% or even 4%, I think it is very important to pause and think if people who continue contributing to their CPF (putting context aside for now) if the rates are near parity.

CPF may lose attractiveness (for a while). That being said, the CPF may change interest rates from time to time. Personally, I doubt that will happen. I am already very appreciative that CPF has kept rates the same despite the prolonged low interest environment.

Wages Inflation

Isn’t this something to be celebrated? Local wages grow by 7.8% in Q1, outpacing inflation. I believe that this is because there is a shortage of labor with travel restrictions. If you are looking for an opportunity, this is one of the best timing to seek a higher paying job.

Final Thoughts

Like I said from the start, these are some thoughts that I have jotted down and my own personal predictions for the future. I would love to hear your thoughts in the comments below.

Last but not least, do consider your own context before making your decision. Do reach out if you wish to discuss with me.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.