Central Provident Fund (CPF) is a compulsory comprehensive savings and pension plan for working Singaporeans and permanent residents primarily to fund their retirement, healthcare, and housing needs in Singapore. It started in 1 July 1955 and just like our Integrated Shield Plans, there have been many changes over the years.

Like with most changes, some will appreciate it, others will not appreciate it as the “rules changed”.

Love it. Hate it. It is an asset class that we will have with us for the rest of our lives.

To help you understand CPF, the opportunities and optimization better, I have put together a free webinar to share my knowledge on it. Limited seats only. Join us with the link here.

Fun Fact #1: You cannot use your CPF to pay for your house in the past

Before 1968, CPF cannot be used to pay for a house. In 1968, the government finally allowed the use of CPF for the downpayment and to service the monthly mortgage loan instalment. Fast forward to 2021, majority of the people around me are using their CPF to pay for their downpayment and their monthly mortgage loan servicing.

This liberation allowed Singapore to have one of the highest house ownership levels in the world. However, as more money is used for housing, the original intend of CPF to help us retire may have taken a back seat. There is also the cause of concern for accrued interest.

Most of you might be servicing your mortgage with your CPF and worry that you do not have enough money in your CPF for retirement. For that purpose, I use a CPF Projection Calculator for my clients. This allow me to accurately measure the amount my clients will have in their CPF at age of 55. So far, they have found this insightful.

Fun Fact #2: Special Account (SA) was started in 1977

To help you with retirement, the special account was created in 1977. Tons of literature has been written on the special account. Among my favorites are the following. If done correctly, the following opportunities will help you in your retirement.

- Transferring Ordinary Account (OA) monies to Special Account (SA) to have a higher interest (up to 5%)

- Retirement Sum Top Up Scheme (RSTU): Top up up to $7000 into your CPF for tax deductible benefits.

- CPFIA: Using CPF-SA to invest (with limitations)

However, it is worth noting that the higher interest that the SA earns is not guaranteed. The floor rate of 4% has been extended by the government until 31 December 2021. The SA and Medisave (MA) rates are reviewed quarterly. The 1M65 movement takes the assumption of these rates being at 4%.

Fun Fact #3: Medisave was started in 1984

Medical inflation isn’t new. Medisave was created to help you to pay for our healthcare cost. It is not hard to understand that one of the The Hidden Cost Of Retirement is Healthcare. With healthcare cost escalating at more than 10% per year, tons of measures have been implemented to help you pay for our healthcare cost.

Among which, you can use your medisave to pay for (part of) our integrated shield plans. There are some outpatient treatments that can be paid using medisave. You also have to set aside a Basic Healthcare Sum (BHS) in your CPF. The BHS is adjust annually to keep up with inflation. This is one initiative to help with medical cost.

With the new co-payment medical plans now, you will have to plan for your retirement a little differently.

Fun Fact #4: Minimum Sum Scheme Was The First Version of CPF-Life

CPF is still about retirement. Before CPF-Life, there was the minimum sum scheme (MSS). However, as your life expectancy increase, you run a risk of outliving your MSS. Hence, the retirement scheme was updated/upgraded to become the CPF-Life. The retirement account (RA) is created at age 55. Your OA and SA monies will be transferred into the RA during then.

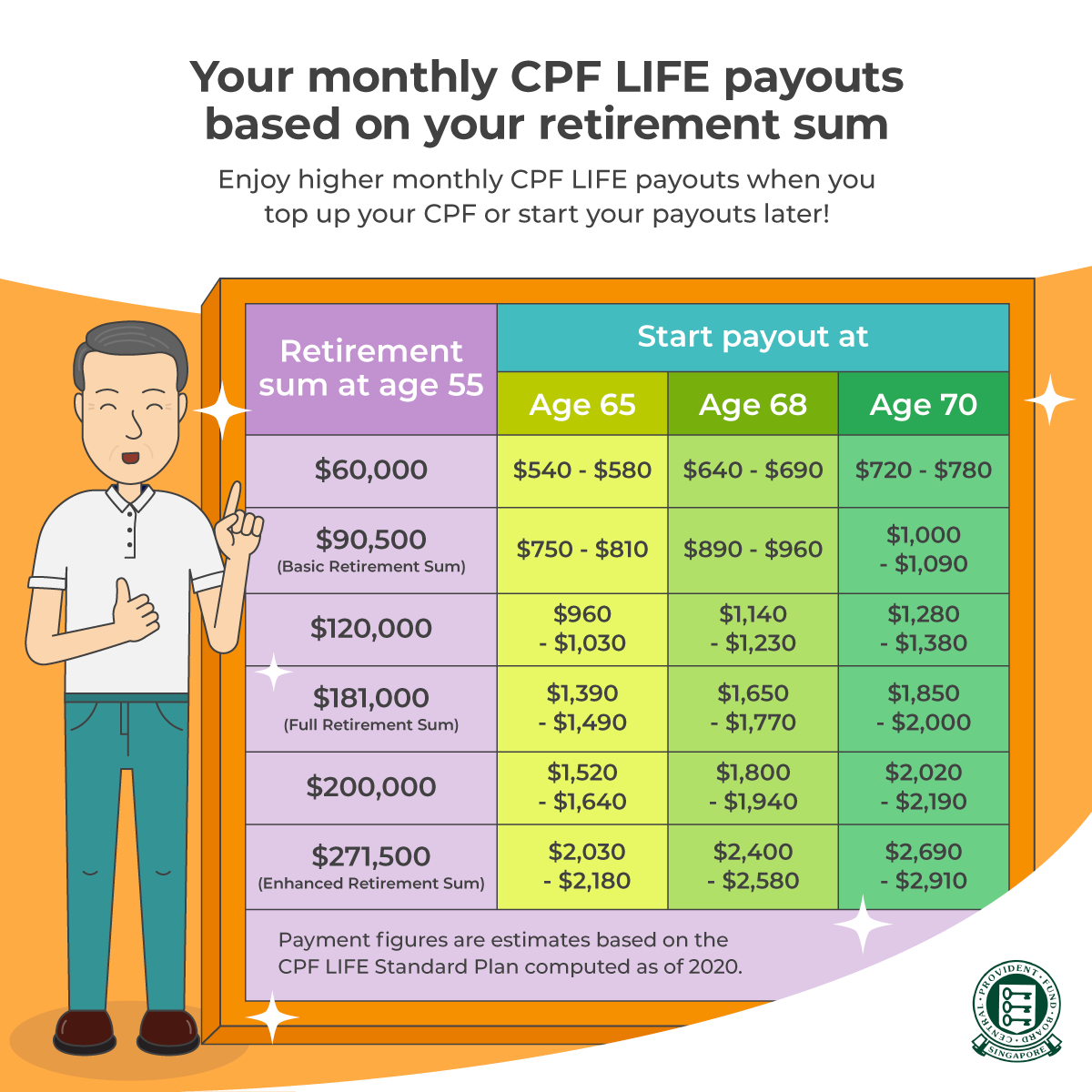

Assuming that you have $181,000 (FRS) in your Retirement Account (RA), you will get between $1390 to $1490 per month for the rest of your life starting from age 65. This will form part of your retirement cashflow. There are 9 options for you to choose from at age 55.

Fun Fact #5: There is a maximum amount of money you can put into CPF a year

You can’t just simply top up everything into your CPF. There is a maximum of $37,740 of mandatory and voluntary contributions that a person (employee or self-employed person) can make in a calendar year is subject to the CPF Annual Limit.

Final Thoughts By Wealthdojo

I personally like the CPF scheme because it really helps a lot of people including myself plan for our retirement seriously. I contribute to my SA every single year so that I can make use of the tax incentive and also hit my FRS in the years to come. Having enough in my medisave gives me the confidence to pay my integrated shield plans yearly and usually the interest on my medisave pays for my shield plan.

To each his own. Love it. Hate it. It is an asset class that we will have with us for the rest of our lives.

If you would like to benefit from CPF more, I have put together a free webinar to share my knowledge on it. Limited seats only. Join us with the link here.

Join my Telegram Channel for a tip a day! In Wealthdojo, we dedicate a small amount of time daily for learning new things. Continuous learning is one of the greatest secrets of success.

For those of you who want to turbocharge your journey, contact me at chengkokoh@gmail.com. I would like to hear from you what your experiences are currently and from there, we develop a plan specially catered just for your journey.

We wish you all the best! Stay Safe and Take Care!

Chengkok, Sensei of Wealthdojo.

[…] I have spoken about 5 Things You Need To Know About Your CPF. This stems from 5 mistakes people make using their CPF that I have written in the last year. One […]

[…] I have spoken about 5 Things You Need To Know About Your CPF. This stems from 5 mistakes people make using their CPF that I have written in the last year. One […]