During the end of the year, the topic of Supplementary Retirement Scheme (SRS) and Central Provident Fund (CPF) contributions will become frequently searched topics for wealth management. This is because for every additional dollar contributed, we might pay lesser in taxes. If you are 40 and older, this article is for you. We are going to talk about taxes, retirement and worse case situations.

#1 Quick Summary of SRS

SRS is a voluntary program started in 2001 to help individual (local and foreigners) to save more money for retirement. You are eligible for tax reliefs by contribution to SRS subjected to the cap of the personal income tax relief (currently $80,000). There is also a maximum that you can contribute to SRS (currently $15,300 for Singapore Citizens and Permanent Residents; and $35,700 for foreigners).

For example, I earn $100,000. I contribute $15,000 into my SRS. My taxable income will now be $85,000 (assuming I have not hit the cap of the personal income tax relief).

Your returns in the SRS account will be tax-free and 50% of the withdrawals from SRS are taxable at retirement.

Your contributions must be made before the 31 Dec of the year to quality (hence, the interest at the end of the year).

You can make withdrawals on or after the statutory retirement age (currently at 62) for you to enjoy penalty free withdrawals. Withdrawals are made in a 10 years window.

For investments in life annuities, the 10-year withdrawal period does not apply. So long as you continue to receive your annuity streams in perpetuity, 50% of the annual stream will be subject to tax.

A 5% penalty will be imposed for early withdrawals.

For more information about withdrawals, head over to IRAS withdrawals to understand more.

#2 The Best Case Scenario

The best case scenario is to have $400,000 in your SRS account at the age of 62 and you are not working by then. We assume that we will be drawing out $40,000 evenly over the next 10 years. Since 50% of the amount withdrawn will be taxable, the taxable income is $20,000 (assuming no other income). At $20,000, there is no income tax payable.

This rigid best case scenario creates a conundrum because it creates a happy problem that you have ALOT MORE than $400,000 due to excellent investment returns AND you still have a well paying job by then.

#3 The “Worse Case” Scenario

Suppose you are 30 year old today and contribute the maximum of $15,300 into the SRS account every year until age of 62. If your ROI is 20%, you would have $31 million in your SRS account. You would have to withdraw around $3 million yearly and be subjected to the highest income bracket.

If we manage our expectations and have a reasonable ROI of 5%, you would have $1.2 million in your SRS account. In this case, you would have to withdraw roughly $120,000 yearly. If you are still working and at the peak of your career getting a good income, you will be possibly subjected to a highest income bracket.

The “worse case” is to have really good investment skills and still be working by then. However, I feel this as a “happy” problem to have.

#4 What if I’m just a normal human being?

$1.2 million sounds big and you might not even be sure you will still have a job then at 62. Most of my client ask me what if they are a normal human being, how does SRS still make sense to a layman?

Firstly, we have to start with the question of contribution. How much should you make a year before SRS contributions make sense?

SRS is a tax planning tool. Hence, it is important to know at which chargeable income bracket (after CPF contribution, tax relief) will it make sense for us to contribute to SRS.

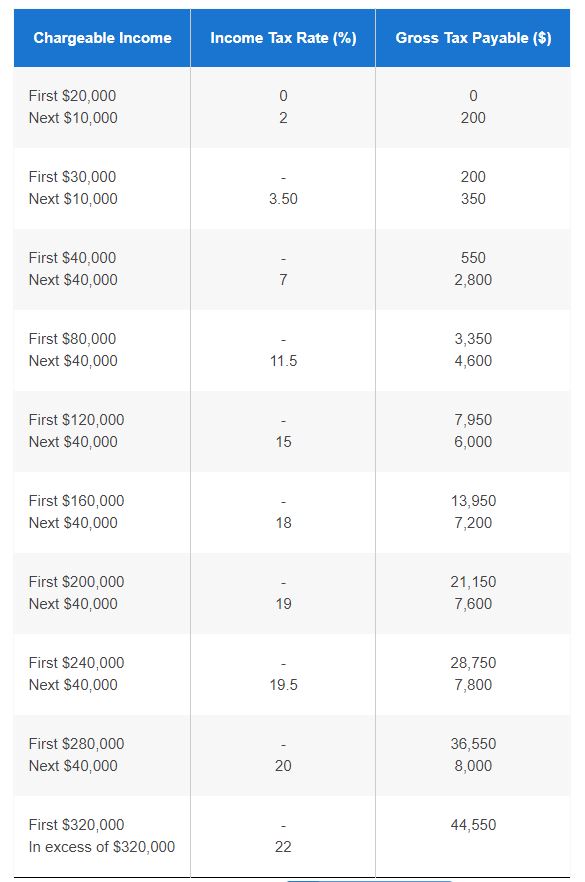

Personally, SRS contribution will start to make sense after the $80,000 chargeable income bracket. Any other income after the $80,000 is subjected to a tax rate of 11.5%. Hence, I find it reasonable to contribute to SRS unless I can find an investment instrument that can give me 11.5% easily. Of course, there are other reasons as well.

#4.1 Tax Savings

To give an example, Amy earns $120,000 annually (after all personal tax relief).

Without SRS, she pays $7950 on taxes.

With SRS, her chargeable income becomes $104,700. She now pays $6190 on taxes.

She saves $1760. (which is a probably an extra month of family expenses)

However, in a situation where by you need liquidity for big purchases such as down-payment for a property, you might want to skip this year’s contribution. The balance of liquidity and tax saving should be taken into consideration.

#4.2 Emergency Funds

If you already have money in your SRS and have a URGENT need for cash, you can still withdrawal from SRS with a 5% penalty instead of having it locked up like the CPF. Of course, we ideally do not want to withdraw from our SRS. However, in an event of a unforeseen circumstances, the funds are still available.

#5 Then why after age 40?

I’m assuming that after age 40, it is likely that our income is more than $80,000. Plus, we might need liquidity for housing/renovation/marriage/children purposes before that. There is also an (irrational) fear is that if we contribute too early, we might compound it too much by then.

Hence, 40 years is ideal because there will be possible substantial tax saving, not having a liquidity issue and also closer to retirement age (lesser compounding period).

A potential solution to the “worse case” scenario is to get an annuity (but you will still be effectively taxed on half the annuity’s payouts every year).

#6onus How should you open a SRS account?

To open a SRS account, simply go to the 3 SRS operators (DBS/POSB, UOB & OCBC) website and you can do it online. You can register an account with any of them. There is little difference which bank you choose because you can invest in SRS approved assets from any institutions.

I suggest that you wait until the end of the year before applying. Typically, there are promotions to open a SRS account at the end of the year. On a side note, I’m don’t think there will be a promotion this year (2020) due to the COVID-19 situation. The banks have also been reducing their benefits this year.

Final Thoughts

I believe that SRS is a great tax saving tool for you if you are 40 and above. Your contribution might save your family one month worth of household expenses. When we are younger, it is important to balance tax-saving and liquidity. Upon retirement, SRS can provide a source of income for us in addition to possibly rental, dividends etc.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

Feel Free To Reach Out To Share Your Thoughts.

Contact: 94316449 (Whatsapp) chengkokoh@gmail.com (Email)

Telegram: Wealthdojo [Continuous Learning Channel]

Reviews: About Me

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

Hi

For the below statement, how do they classify what is returns and what is not? If I contribute 1k every year for 5 years and invest in sti etf, I’ll only be taxed 5k right? The dividends and capital gains will not be taxed?

“Your returns in the SRS account will be tax-free and 50% of the withdrawals from SRS are taxable at retirement.”

Hey Robert, that’s a good question.

I asked that exact same question when I was exploring the SRS. The answer is really something more simple. Consider the followings:

Contribute $1k per year for 5 years: $5000 in the SRS

Because of investment the total amount of money in SRS is: $10,000. This implies that the capital gains is $5000.

After the age of 62, when you withdraw the amount from SRS, 50% of it will be taxable at retirement. As you have $10,000 in your SRS, only 50% of which is taxable. This means that you will be taxed on $5,000 for the withdrawal.

Hope that answers your question.

[…] is the Supplementary Retirement Scheme (SRS) contribution season. If you are 40 and above, do check out my previous post on the 5 things you need to know about SRS. Interestingly, someone emailed me on my 6 Level Wealth Karate System Page to ask about what will […]

[…] is the Supplementary Retirement Scheme (SRS) contribution season. If you are 40 and above, do check out my previous post on the 5 things you need to know about SRS. Interestingly, someone emailed me on my 6 Level Wealth Karate System Page to ask about what will […]

[…] Let’s look at the most ideal case where you reach your FRS (full retirement sum) and also the Best Case Situation for SRS. Assuming you draw down SRS at age of 65, this would mean that you will have the following […]

[…] I have already talked about SRS. In this semi viral article, I described the 5 things you need to know about SRS when you are 40 and older. Personally, I believe that SRS may be suitable for someone who is 40 years old and […]

[…] I have already talked about SRS. In this semi viral article, I described the 5 things you need to know about SRS when you are 40 and older. Personally, I believe that SRS may be suitable for someone who is 40 years old and […]

[…] Basic Knowledge: 5 things you need to know about SRS when you are 40 and older […]

[…] Top Article: 5 things you need to know about SRS when you are 40 and older […]

[…] Basic Knowledge: 5 things you need to know about SRS when you are 40 and older […]

[…] If you are new to Supplementary Retirement Sum (SRS), please start here. […]

[…] If you are new to Supplementary Retirement Sum (SRS), please start here. […]