On Feb 18, 2022, Finance Minister Lawrence Wong delivered the Singapore Budget 2022 in Parliament. The topics were broad ranging as it addresses the economy, helping businesses and green initiatives. The focus which I saw was mainly into healthcare, retirement and funding them.

In this article, I will talk about 4 main things from the Singapore Budget 2022 that will affect ordinary people like you and me. In addition, I will talk about the possible impact in a limited context.

#1: GST for You and Me

Singapore will raise Good and Service Tax (GST) from 7% to 9% in 2 stages in 2023 and 2024.

*Groan*

This might be dreadful news for everyone. GST is basically a tax on all goods and service in Singapore. Think of your coffee at Breadtalk, the iPhone you buy from Singtel or the massage at the parlor. We might not “see” GST very often as most shops would have already incorporated GST into their final prices. When GST increase, this will inevitably be passed to consumers like us. It is more important than ever to plan more for our retirement.

Positively thinking, the GST in 2022 is still 7%. If you have any bigger expenditure (Read more: How To Save On Big Ticket Purchases) that you require, you can consider doing so in 2022. These could be things like renovation, buying a laptop etc.

On a side note, this might boost the Singapore economy in 2022.

#2: Vouchers for You and Me

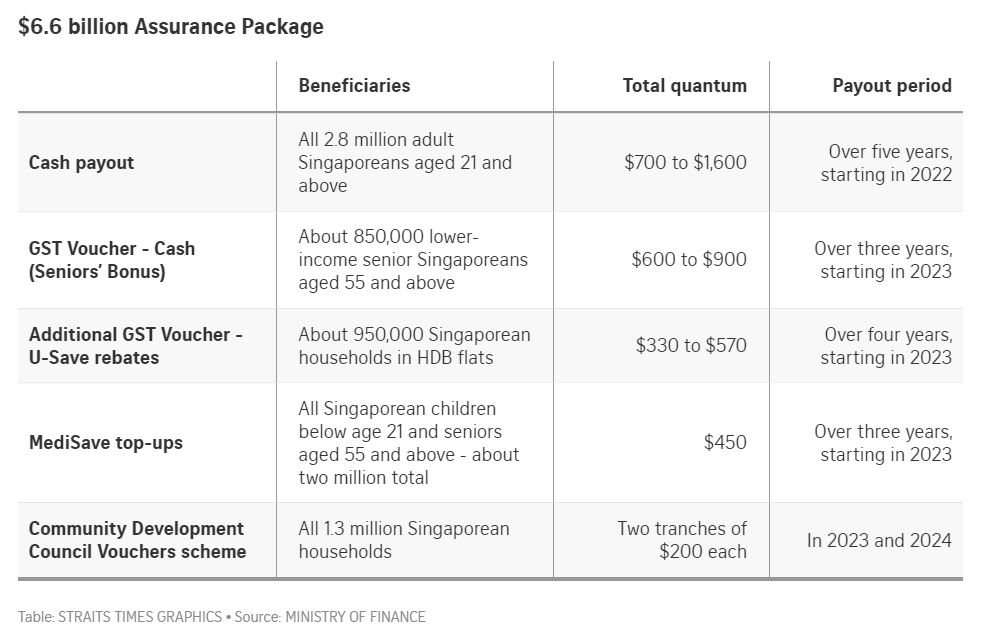

The Assurance Package first announced in 2020 by then Finance Minister Heng Swee Kiat has been topped up to be $6.6B by current Finance Minister Lawrence Wong. The main intention is to help support lower and middle income household in the increase in GST (maintain standard of living) even after the package ends.

The Straits Times actually did a beautiful summary on the vouchers that could be received. For a more detailed look at how much specially you will be getting, the Ministry of Finance page is the place to go.

I can safely say that the minimum that a Singaporean age 21 and above will get at least $700 from 2023 to 2027.

#3: CPF Retirement for You and Me

CPF Retirement Sums Raised

The first impact on CPF retirement is that our retirement sums will be raised by 3.5% per year for the next 5 cohorts that will be turning 2023 to 2027. There have been no mention if this will be reduced after that. It would be good to note that it was previously increasing at 3% per year.

This means that more have to be put inside of CPF so that you will be able to have a higher monthly payout at 65. However, this will also mean that you will likely draw out less at age 55. (Read More: 3 Key Changes To CPF Policies From 2022).

It is also worth noting that 8 out of 10 active CPF members aged 55 in 2027 will be expected to hit their BRS securing a basic level of retirement in any case.

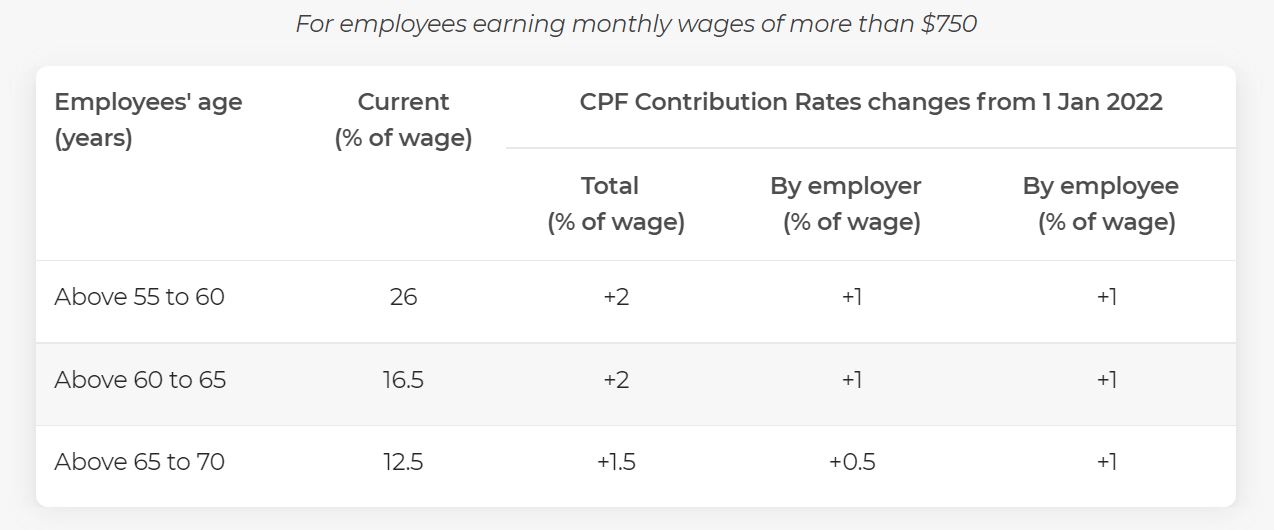

CPF Contribution Rates Raised

The second impact on CPF will be of contribution rates for employers and employees will continue to be increased. The first increase has started from 1 Jan 2022. The next increase will be in 2023. This will also mean that more will go into CPF.

It is worth noting that if a CPF member have already hit the FRS, you will be able to withdraw the excess out as cash. Therefore, increase in contribution rate (by the employer) is generally seen as a good sign.

#4: Taxes for You and Me

If you are affected by some of these tax, congratulations! You might be the top 1% income earners in Singapore. In the budget 2022, there will be 3 main taxes namely, income tax, property tax and luxury car taxes.

Income Tax

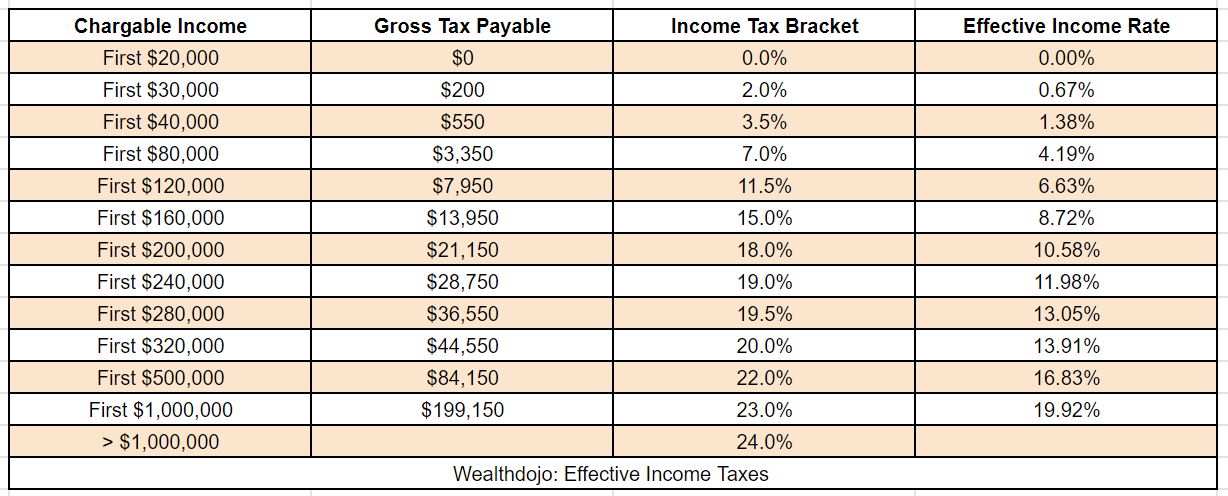

This change will come in for year of assessment 2024. This means that it will be for income earned between 1 Jan 2023 to 31 Dec 2023. There will be 2 additional upper bands.

For chargeable income from $500K to $1M, it will be taxed at 23%.

For chargeable income from $1M and above, it will be taxed at 24%.

In the grand scheme of things, our effective income taxes are still reasonable as compared to many other countries. I believe this will affect the top 1% of us. (Read More: Income Tax Deductible 2021)

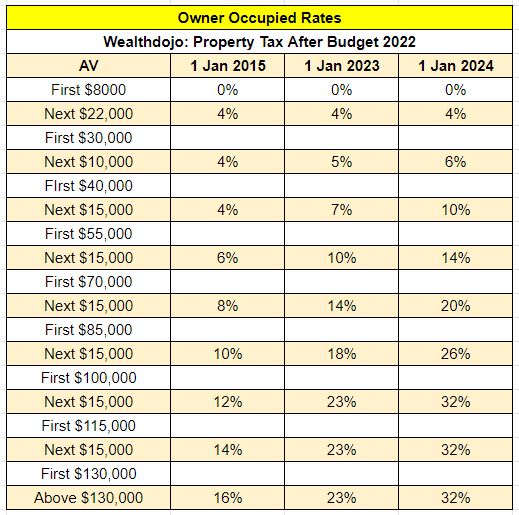

Property Taxes

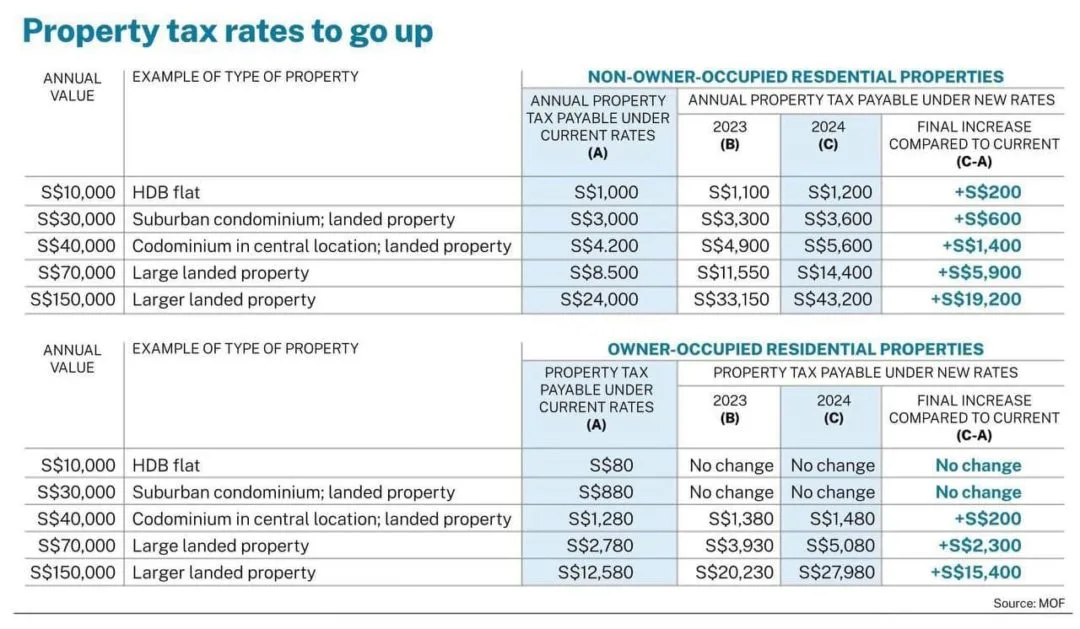

To understand property taxes, there are 2 concepts that you need to know. One is Annual Value (AV) and the other is whether the owner is staying in the property. As the latter is quite clear, I will explain AV.

AV: Estimated gross annual rent of the property if it were to be rented out.

This number is decided by IRAS and there is nothing much you can really do about it. You can find the AV of your property on the IRAS portal. Looking at the photo below, you can have a rough sense by looking at the AV compared with the type of property.

Property taxes will be raised in 2 phrases namely in 2023 and 2024.

I believe impact will be felt for Non Owner occupied of AV > $45,000 with tax rates increasing from the current 14% to 28% in 2024. These would most likely be an investment property that are collecting rent.

For Owner occupied of AV > $55,000, the tax rates will increase from the current 4% to 10% in 2024. According to Lawrence Wong, this will affect 7% of owner-occupied residential properties. I believe this will be a combination of landed property owners (5% according to Department of Statistics in 2021) and some condominiums owners in central areas (2% of residential properties owners by subtraction). It will not affect most of us.

This is be seen as a form of wealth tax.

Luxury Car Taxes

An additional registration fee (ARF) tier has been created for cars, taxis and goods-cum-passenger vehicles with open market values (OMV) exceeding $80,000.

This will only affect Porsche Cayenne, Lamborghini Urus and Bentley Continental GT, and it will also affect several other makes such as Ferrari, McLaren, Aston Martin, Rolls-Royce and Mercedes-Maybach as well as top-end models in a number of other brands.

I believe this will not impact most people on the ground.

The top 6 luxury car brands in Singapore sold 216 cars in 2019. If demand remains the same, only a extremely small proportion of people will be affected by this. This is definitely a wealth tax.

Conclusion

The budget comprises more than just the above 4. The 4 points above just show how the Singapore Budget 2022 will directly impact you and me.

I wish you the best in your financial journey. Hope to hear from some of you.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

Feel Free To Reach Out To Share Your Thoughts.

Contact: 94316449 (Whatsapp) chengkokoh@gmail.com (Email)

Telegram: Wealthdojo [Continuous Learning Channel]

Reviews: About Me

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.