In August 2021, MOH first talk about financing cancer treatments in Singapore. The cancer drug list was then announced to be take into effect in April 2023. I believe this is going to affect healthcare cost in Singapore. However, I don’t see many people being aware of this. In this article, I will talk about what cancer drug list is and the potential impacts on your healthcare costs in the years to come.

Why aren’t we talking about the cancer drug list CDL

Why cancer?

We are lucky that not all critical illness have a drug list now. In my knowledge, cancer drug list was created to finance future cancer treatments in Singapore. By statistics, cancer is the number 1 causes of death in Singapore. As you can see in the table below, cancer is number 1 followed very closely by ischaemic heart diseases.

Singapore’s healthcare cost will definitely be impacted if more and more people suffers from cancer. At the same time, if treatment cost were to increase, the cost may spiral out of control.

As you can see that there will now be a limit on how much medishield life can claim per month for each drug. If this is insufficient, the patient will have to pay cash for it.

I have a shield plan. Will I be affected?

Insurance companies selling the integrated shield plan will have to follow MOH guidelines to change their plans accordingly for claims on cancer treatments. I believe that each insurance will give a different limit to their coverage. Let’s take NTUC enhanced incomeshield to illustrate an example.

Cancer Drug List Example NTUC

You can see that under point 6, depending on the plan type that you are on, the multiple of your limits will be different. For example, if I’m holding on to the Enhanced Advantage, I will be having a 4X MSHL (Medishield Life Limited).

You then have to go to the cancer drug list to find the drug that you need to have find the limit. If the MSHL is $2000, your claim limit under NTUC Enhanced Advantage will be $8000 (4X of $2000) per month. This is before any co-insurance and deductible or co-payment.

Please do get a professional financial advisor to clarify the type of coverage that you have as I have no intension to go deeper into the calculations of the claims.

We have to ask whether we have enough savings to “afford” the second critical illness or cancer especially during relapse.

This is something that you will have to discuss with your professional financial advisor.

Final Thoughts By Wealthdojo

I believe that there will be more of such healthcare treatment cost changes in Singapores in the years to come. While having coverage it important, it is also important to build an asset that will be able to sustain and maintain such coverages in the years to come.

Wishing you good health!

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

Insurance is an expense, until it is not. Here, I wish to address the power of adding critical illness coverage into your portfolios.

What Is Critical Illness Coverage?

Critical illness coverage is a type of insurance that provides financial protection in the event of a covered critical illness, such as cancer, heart attack, or stroke. Many people think that traditional health insurance is enough to cover all medical expenses, but this is not the case.

5 Reason Why You Need Critical Illness Coverage

High Cost of Critical Illnesses: The cost of treating critical illnesses can be astronomical, even with health insurance. Between co-payments, deductibles, and uncovered expenses, it is common for patients to incur significant out-of-pocket costs when diagnosed with a critical illness. In addition, many people are unable to work during treatment, leading to loss of income and additional financial strain. Critical illness coverage can provide a lump sum payment to help cover these costs, giving your clients peace of mind and financial security.

Limitations of Traditional Health Insurance: Traditional health insurance policies typically have limits on the amount of coverage they provide. If your client requires an extended stay in the hospital or an expensive medical procedure, they may quickly reach their coverage limits, leaving them responsible for the remaining expenses. Critical illness coverage, on the other hand, provides a lump sum payment that can be used to pay for any expenses, including those not covered by traditional health insurance.

Maintaining Quality of Life: A critical illness can have a profound impact on a person’s quality of life. Not only do they have to cope with the physical and emotional toll of the illness, but they also face the financial burden of medical expenses. Critical illness coverage can provide the financial resources necessary to maintain your client’s quality of life, allowing them to focus on recovery instead of worrying about finances.

Protecting Savings and Investments: When a critical illness strikes, the financial impact can be devastating. In addition to medical expenses, there may also be loss of income, which can quickly deplete savings and investments. Critical illness coverage can help protect your client’s financial future by providing a lump sum payment that can be used to cover expenses and maintain their standard of living.

Peace of Mind: Perhaps the most important benefit of critical illness coverage is the peace of mind it provides. Knowing that they are protected against the financial impact of a critical illness can allow your clients to focus on their recovery and not worry about how they will pay for their medical expenses. This peace of mind is invaluable and can greatly improve their overall well-being during a difficult time.

Final Thoughts

In conclusion, critical illness coverage is an essential part of any financial portfolio. The high cost of treating critical illnesses, the limitations of traditional health insurance, and the potential loss of savings and investments can all be mitigated with critical illness coverage.

By providing a lump sum payment to cover expenses and protect your client’s financial future, critical illness coverage can give them the peace of mind they need to focus on their recovery. As a world-class financial planner, it is important to educate your clients on the benefits of critical illness coverage and help them determine the right coverage for their specific needs.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

Travelling is not the same after COVID19. There are new terms such as VTL, PCR and 2G ruling. However, that’s not the most frustrating and most worrying thing.

It is that these rules can change overnight.

For those of you who are concerned about the cost of travelling and if it will be worth it, I will be writing on a sole account on my trip to Germany and the cost of it. I will also share my frustrations and what you should take note for your trip if you wish to do so.

Disclaimer: COVID19 rules change often. Please get the most updated information from official sources and let this blog be a guide for your safe travels to Germany.

Is it worth it to travel to Germany during COVID season

Booking of Flights

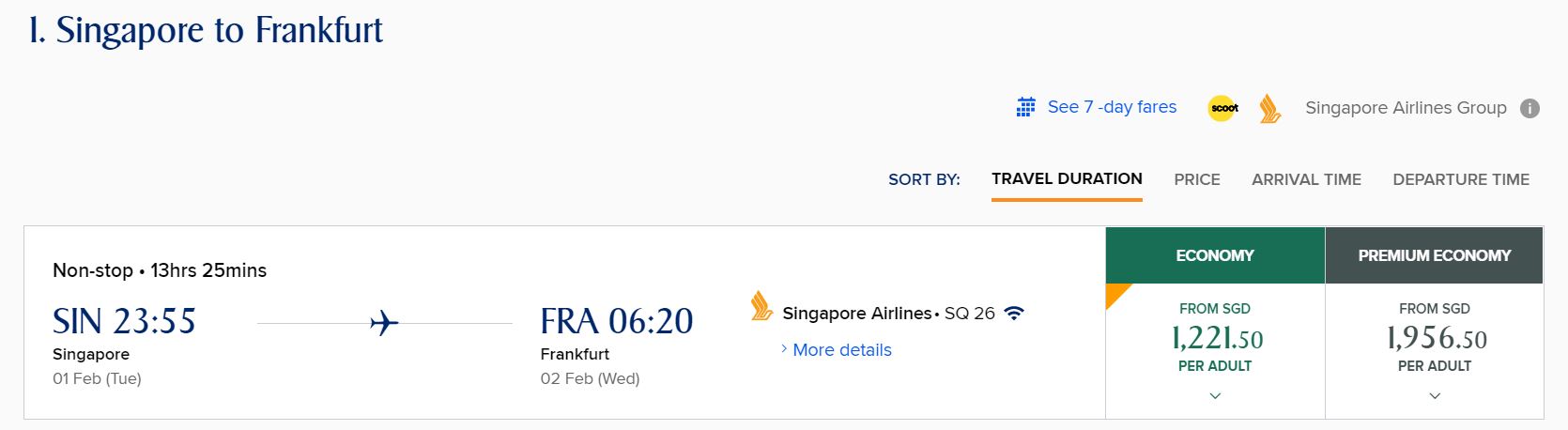

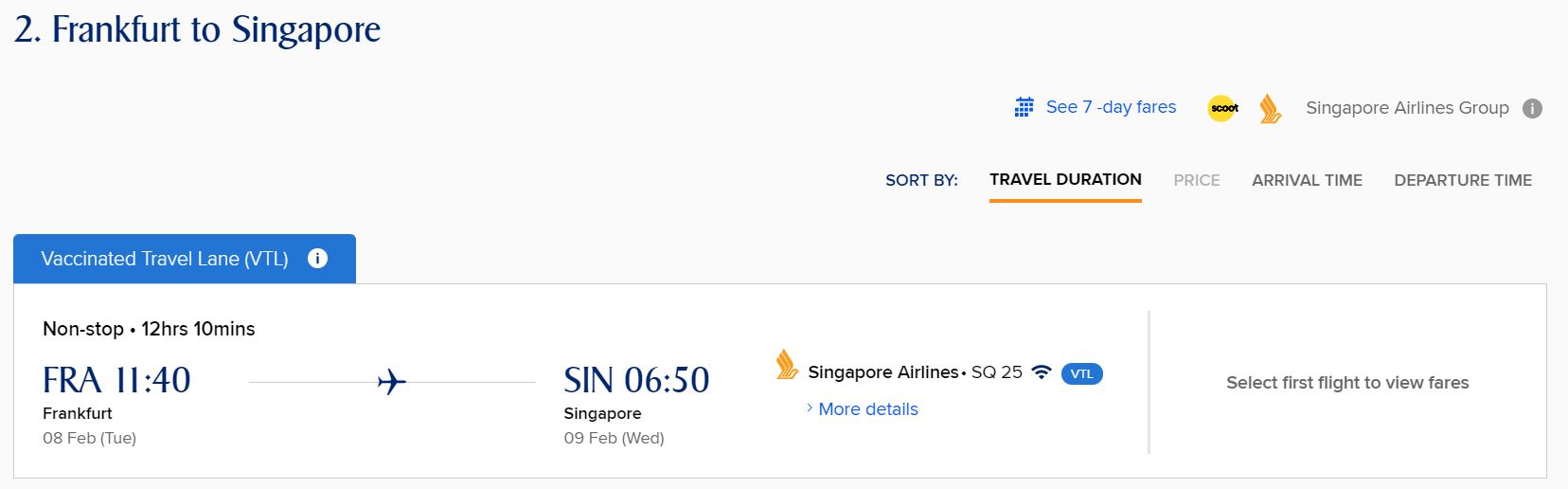

The booking of flight was the easiest part. When we were booking our flights, we were quite worried when we couldn’t find a VTL (Vaccinated Travel Lane) from Singapore to Germany. Fear not, this is because VTL is only applicable from Germany to Singapore. The flight from Singapore to Germany will not have a VTL status as shown below.

SIA Tickets Singapore to Germany Cost COVIDSIA Tickets Germany to Singapore Cost VTL

Noticed that there is a box in blue (from Frankfurt to Singapore) that shows Vaccinated Travel Lane (VTL). If you do not wish to be quarantined when you are back, pick the VTL (Vaccinated Travel Lanes). There will be VTL and non-VTL flights so choose properly. Hope this put to rest some of the doubts that some of you might have.

There are only two airlines namely Lufthansa and Singapore Airlines are serving this route for now.

In our case, We flew by SIA to Frankfurt during December 2021 and it costs $1007 both ways.

Travel Insurance

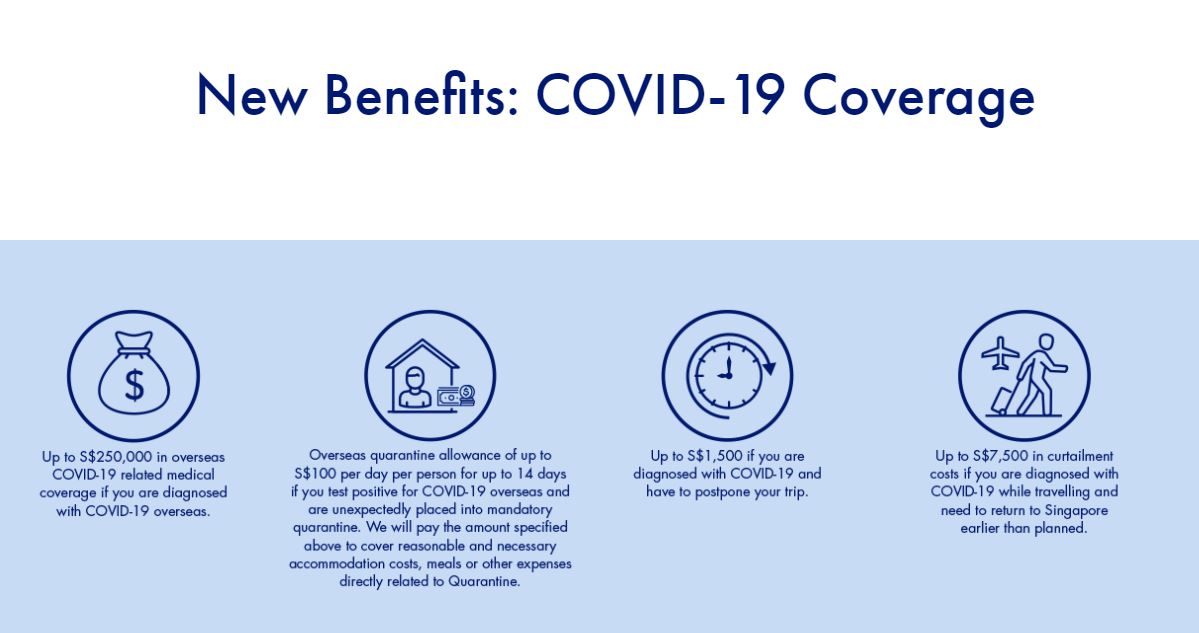

Travel insurance isn’t compulsory during the period of time when we were travelling to Germany but we purchased it anyway. There were 3 decent insurance companies that covers for COVID-19 situations that you can consider. These companies are namely AIG, AXA and NTUC. I won’t go into the details. Please note that some countries require proof of insurance before entering.

AIG COVID19 Coverage Travel Guard

Personally, I selected AIG Travel Guard for my trip there. It cost $137 for a ten days trip to Germany.

Vaccination Proof

This is probably the most important item you will need for a trip. Go to Notarise to download and print a copy of your vaccination proof. (I have also save a copy of the vaccination proof in my phone just in case).

Notarise Vaccination Certification

Germany treats COVID19 very serious. Every single retailer and restaurant will definitely check your vaccination status. You have to be fully vaccinated (with Germany approved vaccines) with 6 months of validity. You can consider this like a “passport / Trace Together” to be checked before entering any facilities.

FFP2 Mask

FFP masks are “filtering face piece”. It is a European standard for mask efficiency, ranging from one, the lowest grade, to three, the highest. Some hotels or tourist attractions will need you to wear a FFP2 graded mask before you can be allowed in.

It is very similar to America’s N95 or China KN95.

Is it worth it to travel to Germany FFP2 mask

I wasn’t sure how strict Germany will be so I bought the FFP2 mask from Shoppe that bore the wording FFP2 on the mask. I bought 10 FF2 masks for 10 days. However, 2 of them was faulty. Luckily, it is generally quite easy to buy a mask in Germany. The box I bought cost $16 for 20 pieces.

German Rail Pass

This is the least complicated of them all. You just have to check if buying single train tickets are worth it or buying a rail pass.

Is it worth it to travel to Germany Rail Pass

If you are travelling inter cities, you might be thinking if it is worth it to get a German Rail Pass. A German Rail Pass is like an “unlimited” travel pass that you can use to get yourself around. The German Rail Pass allows you to travel on Deutsche Bahn trains (U Bahns are not part of the DB series). It will get you to most places. It is generally worth it if you plan to travel to more than 3 cities (with a combination of Frankfurt, Cologne, Munich, Heidelberg, Stuttgart, Hamburg, Berlin). It is quite flexible and you can choose if you want it for 3,4,5,7,10,15 days consecutive or selected travel dates version.

I paid $325 (for myself) for a 10 days consecutive German Rail Pass Twin Pass. Simply print a copy of Rail Pass before going to Germany.

Travelling In Germany

That’s all the heavy lifting you need to do before going to Germany.

At the time of travel (Dec2021), we did not need to do any COVID-19 test to go to Germany (Check the latest here). It would be good to familarise yourself with the 3G, 2G and 2G plus rules in Germany. In most cases, you will see 2G more often, this means that you have to be fully vaccinated or recovered from COVID-19. In most cases of Singaporeans, you will be fully vaccinated already. Simply show your vaccination proof and your passport to be allowed in.

You will also need to wear a mask when you are indoors (trains, shopping center).

The restaurants do not practice safe distancing (which was strange to us). It tends to be a squeezy at times. On the bright side, the food portion is huge and affordable. Order as you deem fit.

Is it worth it to travel to Germany Food Cost

VTL Preparation into Singapore

This worried us the most as we needed to do a Pre-Departure test before coming back to Singapore. When we first booked the air ticket, the requirement was to do a PCR test which cost around 70Euros.

Germany To Singapore Pre Departure COVID Test VTL

However, when we re-checked the website, we realised that PCR OR ART was allowed for Germany (Category II). Although apprehensive, we decide to wing it and take the ART which cost 8.5Euros instead. Talk above massive savings!

We did our test at Zentrum. You should be able to find a COVID test center quite easily in Germany. Please remember to go to a center which will be able to provide you a test certificate showing negative results. In our case, the results came after 1 hour (phew).

We were very fortunate to be the batch that require us to go for 7 days of ART test. On the on the third and seventh days, the tests will have to be done under supervision at a combined test centre. After being tested negative, we can proceed out to do our daily activities.

Fortunately, it wasn’t very expensive. 5 days of test kits cost around $25 in total and the 2 days of ART supervision cost $30. In total, this is an extra $55 that we didn’t see coming.

Conclusion

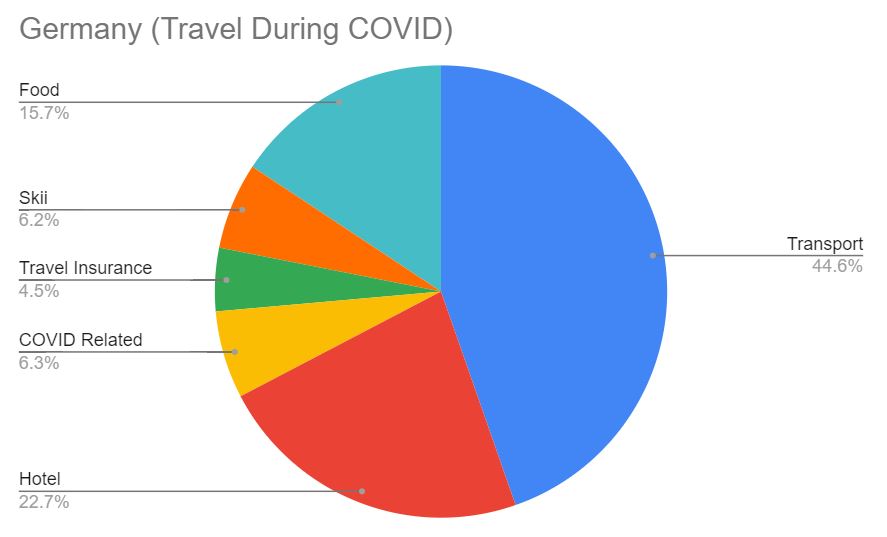

The whole trip costed around $3000 per person. Transport costed the most as airticket and the rail pass was the most hefty item. Accommodation was the second on the list. I found the hotel rates pretty similar as compared to before COVID so book according to your requirement.

I find that budgeting around SGD$100 for daily meals (with beer) is quite reasonable. You probably will have some extra to get some presents.

If you are planning to do skiing, it is not the cheapest activity but it will definitely be worth it.

There is a “new norm” COVID related expense at 6.3%. These includes my FFP2 mask, the PCR test and various ART test.

Is it worth it to travel to Germany Total CostSomebody asked me if given the choice again, will I travel to Germany?

The answer is a resounding yes. Germany is a country that treat COVID seriously. The streets are generally safe and people are friendlier than Singaporeans (I will use myself as a basis point). It is nice to try different food and walk in a different street once in a while. Overall, I enjoyed myself very much and look forward to your experience overseas.

Lastly, take note that COVID rules have changed before and are very likely to change again in future. Please check the latest requirements and let this article serves as a general guide.

Safe travels.

Is it worth it to travel to Germany 2021

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

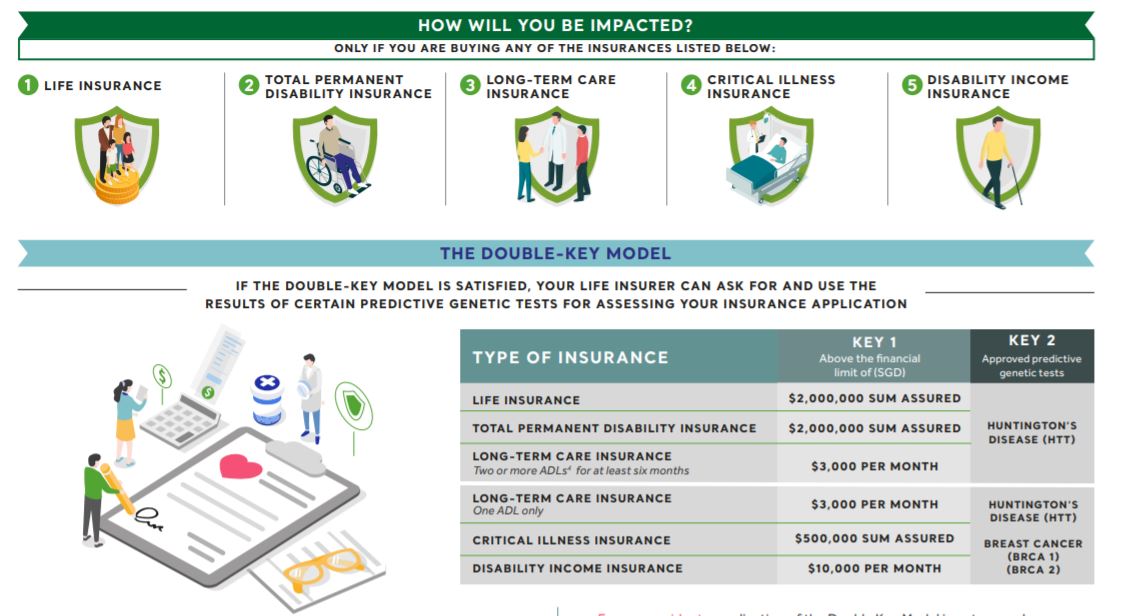

Genetic testing is getting more common as the medical scene evolves. If you find out that you have a “bad” result from the testing, you might fear whether your insurability will be impacted or worried that this is considered a pre-existing condition.

Please refer to the complete details on the LIA’s website. In an event of doubt, please refer back to the complete details as hyperlinked above.

Impact Of Genetic Testing On Insurance Singapore

A Brief Background

If you know that you have a higher chance to develop a condition in future (via those gene testing), you might load up on more insurance now. Insurers knowing that will ask for those test results. To then prevent this from happening, you might be deterred to undergo such testing anyway.

This Moratorium serves as a safeguard to prevent unfair discrimination during risk assessment (or insurance purchase) andadverse selection against insurer.

The Summary

Life Insurers in Singapore are NOT ALLOWED to ask applicants for their predictive genetic test results if they have taken the test. They will not be allowed to use those results for underwriting purposes.

However, given certain criteria are satisfied, life insurers may ask and use results of approved predictive genetic test for underwriting.

This is applicable for Singapore Residents only (Singaporeans, PR and valid pass holders). Non Singaporean residents are required to disclose genetic test results. If genetic test are done for biomedical research, applicants are not required to disclose those results.

This is also applicable to the following insurance policies (Life Insurance, Total Permanent Disability Insurance, Critical Illness Insurance, Long Term Care Insurance, Disability Income Insurance) only.

The Criteria Of Being Asked

Impact Of Genetic Testing On Insurance Singapore LIA Infographic

There will be 2 keys that need to be satisfied before the life insurer can ask for and use the results of the certain predictive genetic tests.

The first key involves the sum assured you are considering. This sum assured refers to the total insurance coverage under all policies issued by insurers in Singapore (including concurrent insurance application). If you require a high sum assured, you might have satisfied the first key.

The second key involves the approved predictive genetic test for Huntington’s disease (HTT) and Breast Cancer (BRCA 1 and BRCA2). If you have done a predictive genetic test for the above, you would have satisfied the second key.

A simple example:

Sarah wants to buy $1,000,000 sum assured for critical illness. She would have satisfied key 1 because she is buying a sum assured more than $500,000 for critical illness.

If she have taken a predictive genetic test for breast cancer previously, she would have satisfied key 2.

As both keys are satisfied, Sarah will have to declare the result of the predictive genetic tests for her insurance application review.

Please refer to the complete details on the LIA’s website. In an event of doubt, please refer back to the complete details as hyperlinked above.

Stay safe and take care.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

This show from Netflix needs no introduction. Amidst the games, the show highlighted the Korea Economy. One with highly-skewed income disparity, worsening household debt and survival of the fittest amid fierce competition.

While watching the show, I keep feeling that the characters behave very badly when it comes to money (or the lack of money). Just a few days after, I can’t help but think that it is an representation of what is happening in real life. (That’s probably why the show resonates to us on some level).

To avoid going down the slippery slope, I decided to consolidate the lessons we can learn from this so that we will NEVER have a situation like this EVER.

Hope you enjoy the read.

Spoiler Alerts: Please do not read this as it contains spoilers on the show. We invite you to come back after you finish the series.

We Have Emotions

Financial Lessons From The Squid Game Emotion Greed Fear (Source: Distractify)

I feel that this is something that isn’t acknowledged much in the financial world. It is often thought that most financial decision can be made logically easily. The basic assumption in most economic literature is that humans are rational in nature. However, behaviour economics proven time over time that this couldn’t be more wrong.

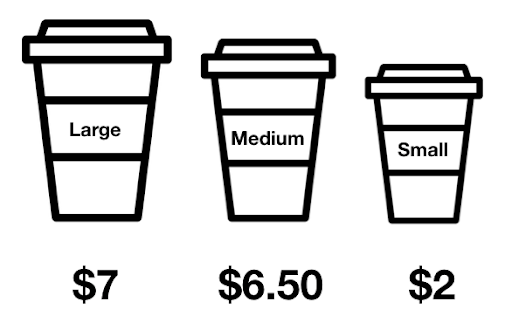

Consider this, you walk into Starbucks (or any other coffee places) to get your daily small dose of coffee. After looking at the prices, most people end up getting the big cup not because they wanted it but because it is a “much better price” than the medium. If you have also chosen the big cup, congratulations, you have experienced the Decoy Effect.

The Decoy Effects explains how an inclusion of an inferior 3rd choice (medium cup) will affect your consideration of between the initial 2 choices (large and small). When there is a decoy alternative, most people makes decision based less on what suits their needs and what we considered as a more beneficial alternative. This results in people spending more as a result at Starbucks.

This is just one of the many cognitive bias that we experience.

These makes it very tough to be rational in a body where we feel so much. Today, most people only focus on the rational side which makes it tough to have a good conversation on finances. I hope that more and more people can come to acknowledgement with their emotions in future.

You Can Win With The Right Strategy

Financial Lessons From The Squid Game Right Strategy

In this very epic game of tug of war, strength is very important. In the team of 10 people, the protagonist team have 3 ladies, 1 weak elderly and 6 men. They faces off a stronger team consisting of all men.

While it feels like the protagonists team have a clear disadvantage in this game, the weak elderly share his wisdom and experience on how to strategize and win against teams that are bigger and stronger than them.

The protagonists team barely escape death by execute the strategy and winning against a team far stronger than them.

In the financial world, you can consider the 10 people the resources that we have. Some of my peers have rich parents, some are left properties under their names, some have good networks and have parents financially independent. But, they may not be financially as well off.

I also have friends who have siblings who depend on them, a study loan, parents who believes that children is the ultimate retirement plan. In spite of this, some of them do succeed in their financial goals by having a right strategy and executing it well.

Having a strong 10 people/resource is important. It is as important as having the right strategy and executing it well.

Learn From Others Mistakes

Financial Lessons From The Squid Game Learning From Mistakes

In another nerve wreaking game called the glass stepping game, participants are made to cross a glass bridge. Participants are presented 2 choices. Stepping on the right choice would mean safety, stepping on the wrong one would meant death. In any event the participant chooses the wrong one and dies, the one after him/her can choose the right one and proceed with the game.

In this game, it is awful being the first one.

In the financial world, money was first originated some where as early as 5000 B.C., in which tons of literature has already been written. One of the classics of financial books is The Richest Man in Babylon. Many important clues have been record and it is up to us to follow that roadmap presented to us.

Another way is to learn from the people around us. If our parents have achieve a certain level of financial freedom, we can learn from it. If our parents have not achieve any, we can also learn from that too.

In whichever case, there is always something to learn.

People Can Behave Badly When It Comes To Money

Financial Lessons From The Squid Game Bad Behaviour

In the final game of the series, Squid game, the 2 protagonists face off in a brutal, savage and barbaric fight. As their lives and the prize money was on the line, they really had a lot to fight for.

I was reminded of estate planning stories and divorce stories that were shared during my recent IBF Certification for Private Banking. Most of the stories were very unfortunate. In almost all cases, humans behaves very badly when it comes to money issues.

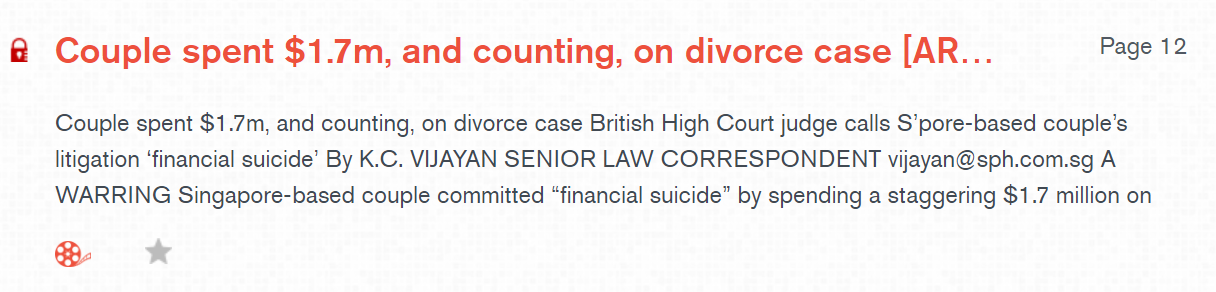

A old example happened in 2013 when a Singapore based couple committed “financial suicide”. Both have spend SGD$1.7 million on legal costs – just to decide where the divorce should be heard as well as litigation costs linked to the child. You can find the article from multimedia stations from NLB Libraries. It is written in The Straits Times dated Friday, 2 Aug 2013 by Senior Law Correspondent K.C. Vijayan.

Divorce Case Financial Suicide

In a more recent example, siblings are suing their elder brother over 2 properties worth SGD$3.1 million. As the estate planning was not poorly set up, it has resulted in a messy inheritance battle of which relationship will be ruined. Though it is not known what the legal costs are, I believe their relationship will never be the same again.

The Financial Journey

Financial Lessons From The Squid Game The Journey

In the most iconic game called Green Light, Red Light, participants win by making their way towards the end of the line in a given time limit. They can only move when it is Green Light (when the doll is not facing them) and they have to stop any movement during Red Light (when the doll is facing them).

At the start, the participants don’t really understand what to do. 2 brave souls started the journey but ended up dead. This causes panic to everyone and people scrambled towards the “exit”. Unfortunately, they were all shot dead.

The cooler headed participants began their journey again. Unfortunately, some tripped either because they were moving too fast or just unlucky to bump into themselves. They died in their attempt to reach the end.

As some participants crossed the line and won the game, there were others that couldn’t cross the line and died as well.

In this game, it closely symbolizes our journey with money. In a given period of time (working years), we want to reach the end (retirement). Some people panic when they see others lost money in the investment and ran towards the exit (panic selling). Some people overleverage (move too fast), some people suffers from critical illness (bump into themselves), some people start too late (couldn’t reach the end). In all these cases, it resulted in people having a less than ideal lifestyle.

Final Thoughts

Overall, this show was a dark, ghastful and yet awfully realistic in showcasing the behaviour of humans put in those desperate situations.

I recommend watching a comedy after the show.

What other financial lessons have you learn from this show? Let me know in the comments below.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.