I remember my mom telling me to eat more vegetables when I was younger. At that time, I absolutely hated broccoli and only ate it because I can only play with my playstation after that. Years later, I can only assume eating broccoli was a great decision because I don’t really fall sick as often as my peers. I did not appreciate my mom’s nagging advice (I mean who did at that time) until years later.

Turns out that nagging found its’ way into adulthood. As a financial planner, I’m constantly giving money advice that no one wants to hear. But those who listened and applied the concepts tend to have better cashflow, protection and investment portfolio.

You might not like it, but it is for your own good.

3 pieces of money advice no one ever wants to hear

#1: You Got To Save To Have Money To Invest

“I want to invest but investing more than $100/month is too much because…”

To set the context, these are people with good monthly income of around $3000 to $6000. I find it scary to have so many conversations with people who have issues setting aside money every single month BUT wants to invest. It is like wanting to bake a chocolate cake with no chocolate. Often, not having a Level #2: Abundant Surplus Creator set up is one of the main cause of failure.

Saving more than you need will buy you opportunity and freedom in the future. The usual guideline is to set aside at least 25% of your take home salary. This 25% will buy you opportunity and also freedom that you desire.

#2: Have A Backup Plan

“You will fail in life 33% of the time. Do you have a backup plan?”

Cancer hits 1 out of 3 people in Singapore. Each and every of us have a 33% chance of our income source robbed away when we are unable to work when we are ill. If you are lucky and detected it early, the effects may be temporary. However, if it is a major critical illness, the effects will be longer term in nature.

With COVID-19 still looming over our heads, I think it is clear that the next war we will be fighting is a Health War. No one likes to imagine the worst cause situation but if something really happens, you will be glad that you have a backup plan Level 4: Aegis Of War aka insurance especially medical and critical illness coverage.

#3: Don’t Time The Market. Invest For The Long Term

“I want to wait until the market crash (like in March 2020) and invest.”

You will be waiting for a long time. Before March 2020, it was Sept 2008. Before Sept 2008, it was April 2000. From 2000 to 2021, S&P500 is up roughly 189% with a CAGR of around 6%. It is certainly very easy to look back in 2008 or 2020 to say that it is the best time to invest BECAUSE it has already happened.

It is virtually impossible to predict the market. Investing may be all sunshine in 2020. However, it is not as fun and sexy as you think it is. The recent pull back has shattered some confidence in the market and you might be wondering what to do next.

Build a strategic investment plan and stick to it. We want to invest in companies that is of value and growing and hold it until it rewards us. You can take a look at some of the largest companies now that is rewarding investors. Companies such as Apple and Facebook are rewarding investors with price appreciation and also dividends over the last 10 years whether it is market crash or not.

Final Thoughts By Wealthdojo

Eat your veggies. Trust me, it is good for you.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

This is not an April Fool’s Joke. It is real. My readers would already have known about this since last year. If you are lost or do not have a financial consultant to update you on your ISP, the bold statement is a summary of the change in the ISP structure.

Existing ISP supplementary plans will have a co-payment structure.

This means that there won’t be a 100% coverage/reimbursement anymore. Customers will have to pay a XX% co-payment (depending on the terms and conditions of your policy). You can read about co-payment and how to plan for it here.

But First: Medishield Life Premiums Increase

How Integrated Shield Plans Affect You (All Insurer Edition)

Following the announcement of 21st Dec 2020 new release from the MOH, claim limits will increase. At the same time, there will be premium adjustments to support the rising number of claims and payouts as well as the benefit changes. You will see this reflected in your renewal because Medishield Life is a component of your ISP.

Integrated Shield Plan Changes (All Insurer Edition)

In Singapore, there are seven health insurance providers. Each of them have adjusted their premiums and benefits accordingly. You should be more interested in what your existing rider has changed to. Here is a summary for the 7 health insurer in no particular order. These are all public available information and I will be putting a link of each insurer here.

How Integrated Shield Plans Affect You (All Insurer Edition)

AIA Singapore

Premium increase for HealthShield Gold Max A

Premium increase for Max VitalHealth A rider

Max Essential riders to be converted to riders with co-payment

– Essential A convert to Max VitalCare

– Essential A Saver convert to VitalHealth Awith EOCB Booster

– Essential B convert to VitalHealth B

– Essential B Lite convert to Vital Health B Lite

– Essential C (no conversion but there will be premium reduction)

I believe this will not be the first or the last change when it comes to medical cost. It is therefore, important to have a trusted advisor who communicates the changes in a timely manner and navigate your retirement accordingly. As a financial consultant, I believe that this communication is vital because we never know such treatment and the affordability will arise.

Wishing you the best in your day ahead.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

We don’t really talk about taxes in 6 Levels Wealth Karate Methodology. In a simple gist, taxes are bittersweet to me. On one hand, I don’t like to pay taxes as it is an expenses to me. On the other hand, if I pay higher taxes, it would mean that my income is higher! I’m just glad that in Singapore, we have a really attractive tax program and we pay significantly lesser taxes as compared to people in other countries. Without going too deep into that, here’s how how much to pay for your income taxes in 2021.

Do you need to pay taxes or not?

Yes. You only pay income taxes if your chargeable income is greater than $20,000. Some income are chargeable and some are not. Fun fact: your winning from your TOTO/4D is not a chargeable income. Check out the full list here.

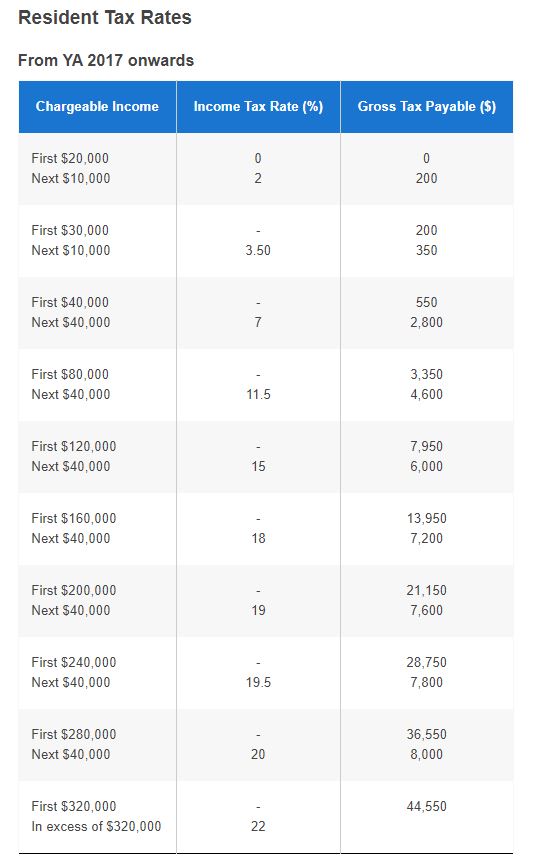

If your chargeable income in 2020 is above $20,000, you will be taxed with the progressive income tax system. Singapore follows a progressive income tax system. This means that the higher your income, the more you pay in taxes. The resident tax rates are as follows.

How To Reduce My Income Taxes Resident Tax Rates

However, this does not show the effective income taxes for your income. When I first saw this table, I thought that if I earn $80,000, my tax bracket would be 7% or $5,600. This is untrue.

How To Reduce My Income Taxes Effective Income Tax Rates

If you are earning $80,000, you will be paying $3,350 in taxes which means my effective income tax rates are 4.19%. Personally, I think it is quite fair. With the same $80,000, you would be paying $23,571 or 29.46% effective income taxes in USA.

Is it automatic?

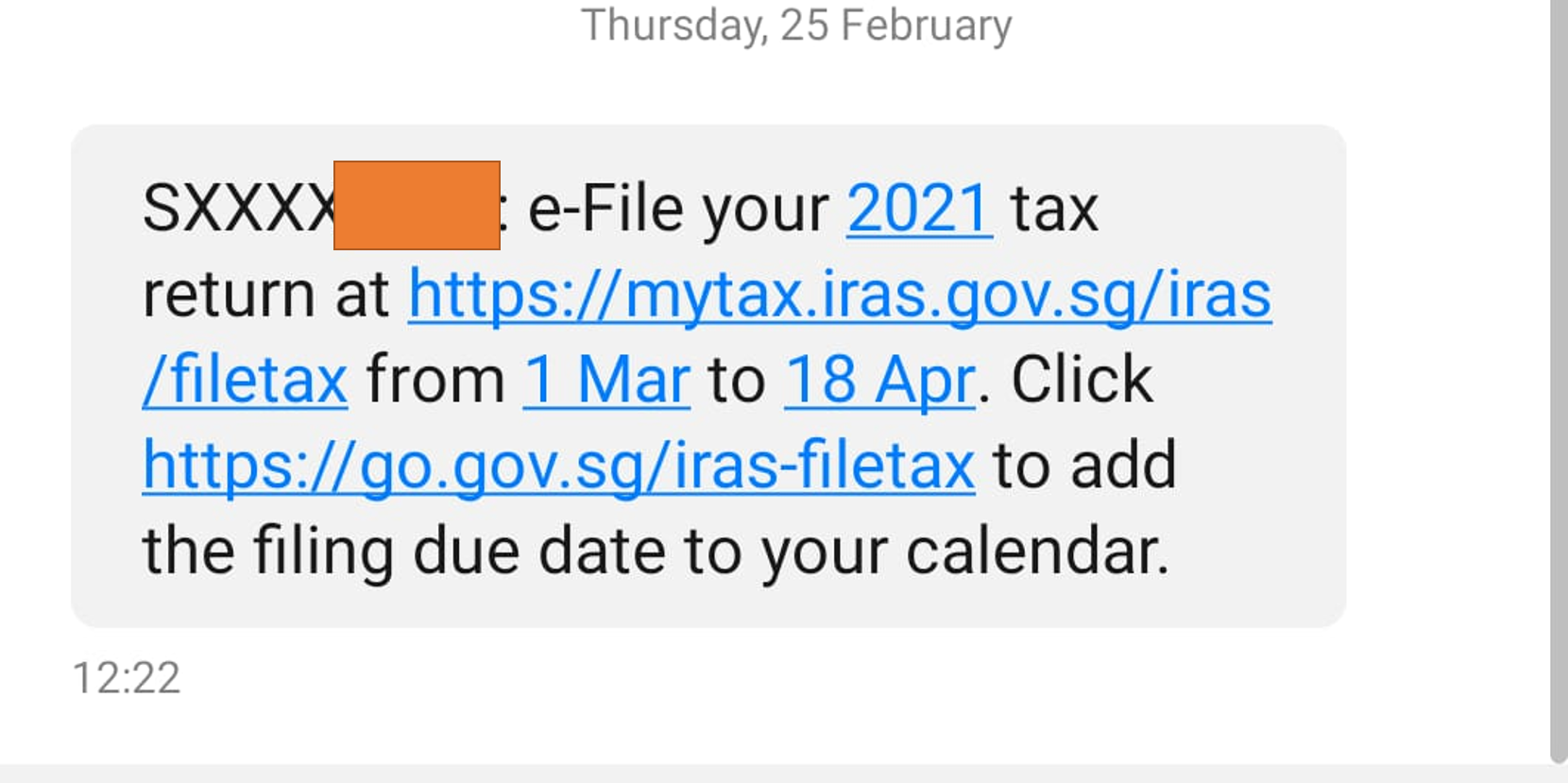

If you received a letter/SMS/form that tells you to file your income tax, you will have to log in and file it yourself. This sms below is one that I received from IRAS. Typically, most of my income have already be pre-filed as I’m a self-employed working with AIA.

Income Tax 2021 Filing

If you received a letter/SMS/form that tells you NOT to file your income tax, you don’t have to do it. But please verify if your information is correct and accurate.

If you didn’t receive anything from IRAS, you will still need to file a tax return if your:

annual net business income exceeded $6,000, OR

annual income (inclusive of rental income) was more than $22,000 last year

Tax Deductibles

Since 2020 is over, you can’t really do much changes into your deductibles. You can start planning for 2021 instead. In Singapore, we have a list of deductibles given to encourage social and economic objectives such as filial piety, family formation and the advancement of skills.

Income – Deductibles = Chargeable Income

As mentioned above, you will pay taxes on your chargeable income. This means that deductibles will play a big role in the taxes you are paying.

There were only two things certain in life Death and Taxes

Co-incidentally, these two can be well managed by proper financial planning or using insurance tools to achieve your financial goals. This article is meant to be a general article on how to pay taxes in Singapore. If you would like to know more, just comment on this post or contact me and I would love to have a conversation with you on the above.

Stay healthy. Stay Safe and pay your taxes.

Thank you for your contribution to nation building.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

It was a tough change. It is no secret that medical inflation is raising in Singapore and is showing no signs of slowing down. Medical inflation is expected to rise to 10.1 per cent in 2020. In the midst of finding fault with greedy doctors, overpaid agents or kiasu parents, I prefer to find a solution to plan for medical expenses after 1st April 2021.

To provide some context to this, the MOH has welcomed insurer’s move adjust terms for full-rider IPs, require co-payment of hospital bills. This would mean that the day will come when there is no longer 100% coverage hospital plan. This will change the way we plan for our retirement and the associated hidden costs.

Planning for Medical Expenses After Changes In Full-Rider IP Copayment

The Current Situation

Planning for Medical Expenses After Changes In Full-Rider IP Insurance Companies

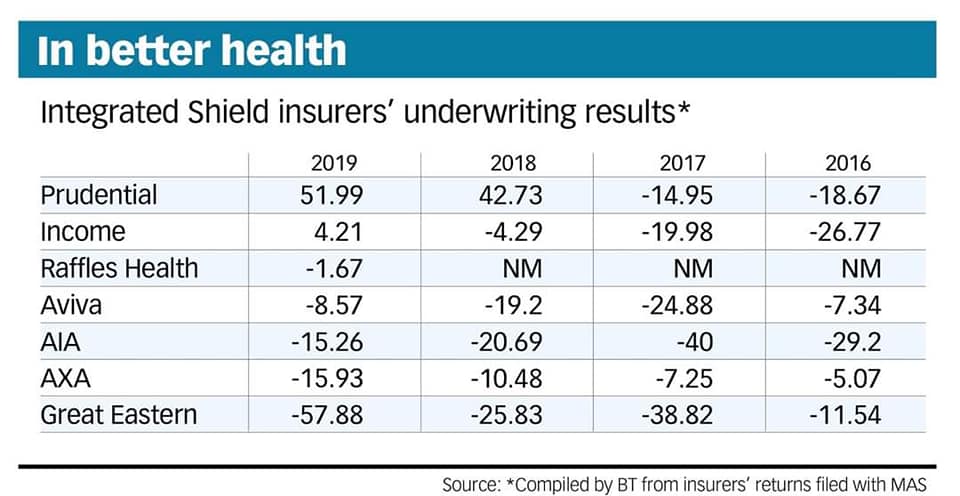

Shield Plans Underwriting Profits And Losses Singapore

Reviewing the Integrated Shield Plan underwriting losses from Business Times, GE has the greatest underwriting losses in 2019 and it is likely for them to have the incentive to transit their customers to a co-payment plan. AIA has roughly the same underwriting losses with AXA. Although both companies have not officially reported the change (at least to the press), I believe they would have a strong incentive to do so.

For the people like you and me, we have to embrace the Co-Payment nature of the policy moving forward.

What is Co-Payment?

A co-payment basically it is out-of-pocket amount paid by an insured. In the context of shield rider in Singapore, there may be other conditions like going to list of panel doctors, pre-authorisation, deductive waiver pass etc. For discussion, we will assumed that those requirements are fulfilled (please check with your financial consultant for those requirements).

5% Co-payment for every bill, up to $3000 per policy year.

Case #1

First Bill is $10,000. No other claims in the policy year.

Client pays $500 (5% of $10,000)

Case #2

First Bill is $100,000. Second Bill is $100,000 in the same policy year.

Client pays $3000 for first bill. (Although 5% of $100,000 is $5,000, there is cap of $3,000 per policy year). Client pays $0 for second bill (max payment per year is $3,000).

Having a copayment will further encourage prudent use of healthcare services as the patient will pay part of the bill. It is worth noting that the maximum a patient will pay per year (assume the requirements are satisfied) is $3000. This should be incorporated into your emergency funds.

How to fund co-payment?

There are a couple of ways to pay for co-payment and these are 4 possible ways that you can consider.

#1: Medisave: There is a limit which you can pay using Medisave.

#2: Company Insurance: This is only applicable if you are currently employed.

#3: Accident Plan (Accidental Medical Reimbursements): For hospitalisation arising from accidents, the accidental medical reimbursement helps with the co-payment payment.

#4: Emergency Funds: It is important to set this up as soon as possible.

Final thoughts by Wealthdojo

Hopefully, this will be one of the final time that there is such a major change in medical insurance scene. This will definitely affect the way we plan for our retirement and also our emergency funds.

Please note that the terms and conditions for your IP may vary. It is best to talk to me or your preferred financial consultant on the upcoming changes on 1st April 2021 (if any).

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

Investment Linked Policies or ILPs have been an ideal target to be bashed by many personal finance groups and investment gurus. In your wealth management journey, perhaps an agent might have ethically (common assumption used by those groups/gurus) told you or sold you an ILP before. Hence, you might start to think whether the ILP does make sense for you.

These Groups/Gurus’ bottom line: Cancel Your ILPs. The fees are expensive. Buy term, invest the rest. You can get better investment returns.

Wealthdojo’s bottom line: ILP is suitable if you are looking for a booster in coverage for a short period of time and plan to accumulate shares/units in a systematic way. You have a more passive approach to investment. An ILP works ideally when you are younger.

3 Brutal Truths about Investment Linked Policy You Wish You Knew ILP Confused

So what now? Disclaimer aside, I hope to share with you 3 brutal truths on ILP and the current narration on ILP in the market.

Short Recap

Investment Linked Plans are policies that have life insurance coverage and investment components. Your premiums are used to pay for units in one or more sub-funds of your choice. Some of the units purchased are then sold to pay for insurance and other charges, while the rest remain invested. (Moneysense Definition)

In a layman structure, it looks like this.

Pay Premium > Buy units of the funds at today’s price > Some units are sold to pay for insurance > Wait for next month premium

The units accumulates every month via dollar cost averaging and will build up substantially in a long run. Let’s go on to the brutal truths for ILP.

Truth #1: You will pay fees.

This reminds me of a story of a man buying cake for his son’s birthday. After looking at various cakes, his eyes soon fell on a 7-inch strawberry fresh cream cake that stood at the center of the display. This shop is famous for their fresh cream and his son loves fresh cream.

Man: “This cake looks beautiful. How much is this cake?”

Baker: “It costs $97 sir”

Man started to be agitated: “That’s ridiculous. It is just a bunch of strawberries, flour, eggs and sugar. This is a rip-off!”

Baker said calmly: “Sir. You are right. Therefore, we have something just for you”

The baker brought him to the corner and showed him a bunch of strawberries, flour, eggs and sugar and said: “Those will be $13”

Man: “I don’t understand. What do I do with a bunch of strawberries, flour, eggs and sugar?”

Baker: “Well, that’s what we are paid to do.”

3 Brutal Truths about Investment Linked Policy You Wish You Knew ILP Fees: Source

The simple truth is that there will be fees. When you enroll into an ILP, you are paying for insurance, you are paying for wealth management and miscellaneous administrative fees which includes commission for the consultant. You are paying to enroll to a service which consist of insurance protection and investment accumulation.

The narration in the market is that an ILP’s charges are expensive and expensive is a subjective word. Perhaps, it is better to put things side by side with insurance and investment.

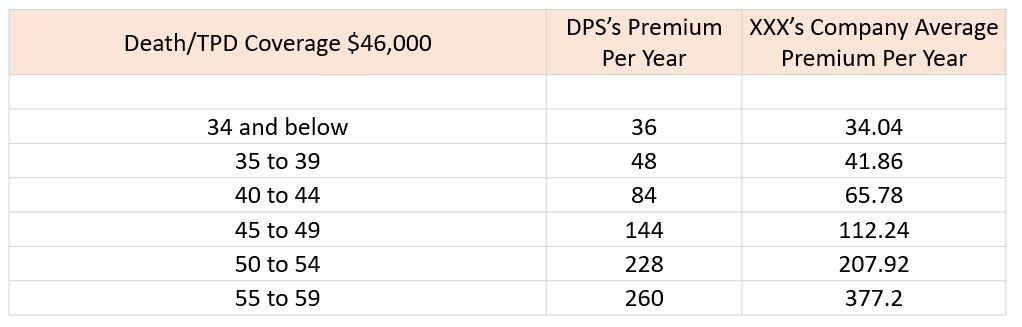

Let’s take a look at insurance. I will be comparing our National Insurance Dependent Protection Scheme (DPS), as compared to XXX company’s ILP charges per age band (I personally believe the charges are very similar across companies). We will compare using a basis of $46,000 sum assured for Death and Total Permanent Disability (TPD).

3 Brutal Truths about Investment Linked Policy You Wish You Knew ILP Insurance Charges

As you can see, the charges for XXX’s company is lower than DPS for all ages except for 55 to 59. This shows that rates are quite competitive. As you become older, you pay more for insurance as the chances of you suffering from Death and TPD increases.

You can also see an element of the popular advice buy term invest the rest here. On an ILP, we contribute a premium monthly. Part of it is used to pay insurance. In the table, we pay for the required insurance charges at that age and the rest goes into investment. If you add on other unit deducting riders like critical illness and early critical illness, you should pay more premium so that you won’t have too little going into investment.

Note: DPS is due for a change and there could be a chance the insurance companies might follow as well.

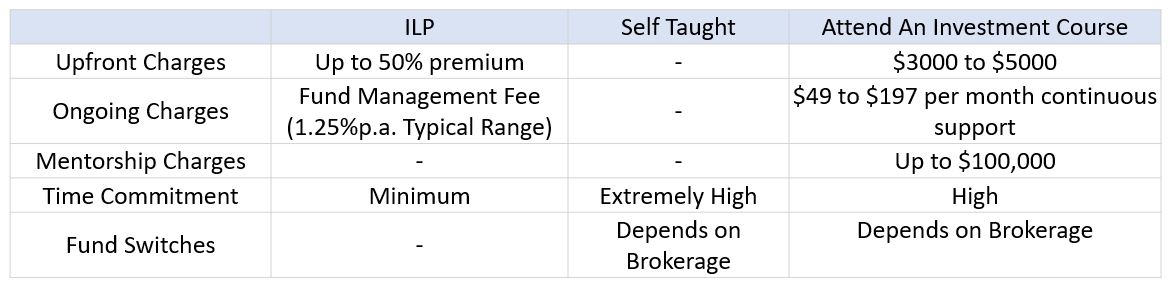

Let’s talk about investment now. As the strategy for an ILP is mostly passive, it might not be a fair comparison to other investment methods that might be more active. I will give an attempt to compare the fees across various personalities.

3 Brutal Truths about Investment Linked Policy You Wish You Knew ILP Investment Charges

The current narrative from investment gurus are that the ILP has high upfront charges of up to 50% of the premium. It is the same for investment courses as well. They do charge a high upfront course fee of around $3000 to $5000. Furthermore, I assume there are no other upsell programs after that.

Another common narrative is that the 1.25% p.a. fund management fee will reduce the investment returns in the long run. This is a true statement as any expenses will reduce your investment returns. Recently, investment courses are also changing to provide continuous support at a fee of $49 to $197 per month. This is akin to having a “fund management fee”.

For those that are self taught investors, he/she might have save on the cost. However, I can only imagine how huge the time commitment he/she dedicated into learning how to invest. One can say to invest in a passive S&P500 index fund with low expense ratio. Then again, how long will you take to reach this decision? How many mistakes might this person make before doing that?

Fees will have to be paid. It is just a matter of to who and how.

Side note: It may not be fair to compare anyway. An investment course does not have insurance coverage. Similarly, an ILP is not an active strategy as compared to some investment courses. The lessons you learn from investment courses are also priceless.

Truth #2: If you pay peanuts, you will get peanuts.

Whether it is an ILP, endowment or ETF, if you pay peanuts, you will get peanuts.

This is rather straightforward. I know some people who may have unrealistic expectations on the money they are saving or investing. A $100/month policy or a $100/month ETF is not going to buy you your financial freedom. If you invest $100/month for 30 years with an 10%, you will get $197,392 which is decent but definitely not enough for retirement.

3 Brutal Truths about Investment Linked Policy You Wish You Knew ILP Invest Small

This year, I presented a few maturity cheques varying from $15,000 to $60,000 to some of my clients. I excitedly told one of my clients that his maturity cheque is coming in August 2020 and told him to look out for it. He took me out for coffee and asked me how much he was getting. After checking my portal, I told him the amount was $22,000.

He took a sip and exclaimed “Why only $22,000? I has been paying for 25 years.”

“Uncle, you were saving $50/month. In total, you saved $15,000. Personally, I think this is a decent return.”

Imagine there is an investment that can give you 100% returns. If you invest $100 in it, the maximum you will get back is $100. $100 in absolute is not a lot. Therefore, it is very important for us to save up our first pot of gold or simply increase the amount of regular contributions every month.

Truth #3: Not everyone you meet will be interested in investing

Sometimes, we forget that we look at others with our tinted lens. We tend to judge a decision and call foul when it is a decision that is not consistent to our own belief. In a recent viral article, a young couple in their 30s paid off their $470K HDB loans in 2 years.

3 Brutal Truths about Investment Linked Policy You Wish You Knew ILP Opinions

This is a feat that is not easy to many. However, this sparked off a huge debate on many personal finance groups saying how financial “Illiterate” they are. They could have made use of the low interest environment to pay off their loans and use the money to invest in other things.

First, I would like to congratulate them. They are debt-free and it is something money *ahem* can buy. If their objective in life is to live a life that is debt free, they are already successful.

Not everyone you meet will be interested in investing or willing to spend loads of time to look into investment. Therefore, the ILP gives a simple disciplined dollar-cost-averaging strategy to accumulate the units of the recommended portfolio funds.

I’m not advocating ILPs. At the end of the day, the ILP is a wealth accumulation and insurance tool that can fit into a certain profile of individuals. It may be suitable for certain groups of individuals. Personally, I feel that the narration of the ILP has been viewed with tinted lens. Those people are right in their own aspects and life stages.

If you are unsure if the ILP is still suitable for you, please feel free to write in to me. I would love to help you understand it together.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.