We don’t really talk about taxes in 6 Levels Wealth Karate Methodology. In a simple gist, taxes are bittersweet to me. On one hand, I don’t like to pay taxes as it is an expenses to me. On the other hand, if I pay higher taxes, it would mean that my income is higher! I’m just glad that in Singapore, we have a really attractive tax program and we pay significantly lesser taxes as compared to people in other countries. Without going too deep into that, here’s how how much to pay for your income taxes in 2021.

Do you need to pay taxes or not?

Yes. You only pay income taxes if your chargeable income is greater than $20,000. Some income are chargeable and some are not. Fun fact: your winning from your TOTO/4D is not a chargeable income. Check out the full list here.

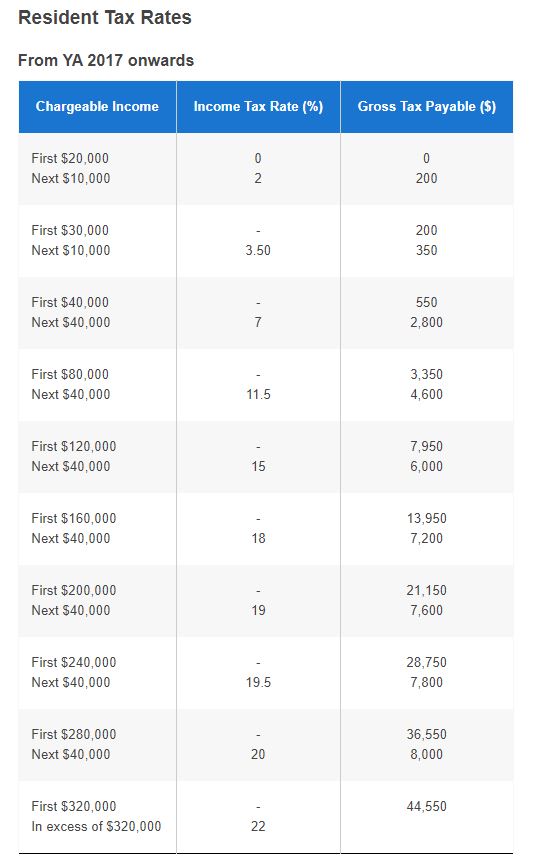

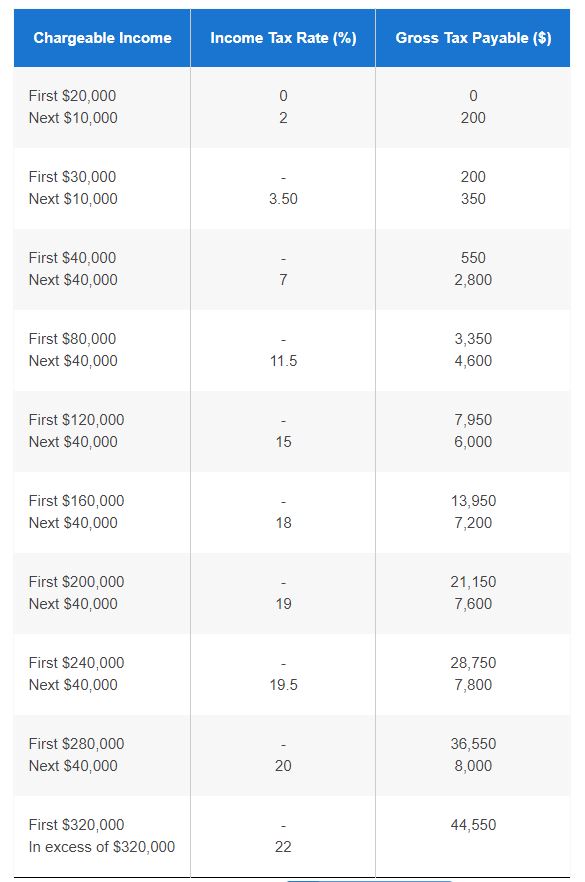

If your chargeable income in 2020 is above $20,000, you will be taxed with the progressive income tax system. Singapore follows a progressive income tax system. This means that the higher your income, the more you pay in taxes. The resident tax rates are as follows.

How To Reduce My Income Taxes Resident Tax Rates

However, this does not show the effective income taxes for your income. When I first saw this table, I thought that if I earn $80,000, my tax bracket would be 7% or $5,600. This is untrue.

How To Reduce My Income Taxes Effective Income Tax Rates

If you are earning $80,000, you will be paying $3,350 in taxes which means my effective income tax rates are 4.19%. Personally, I think it is quite fair. With the same $80,000, you would be paying $23,571 or 29.46% effective income taxes in USA.

Is it automatic?

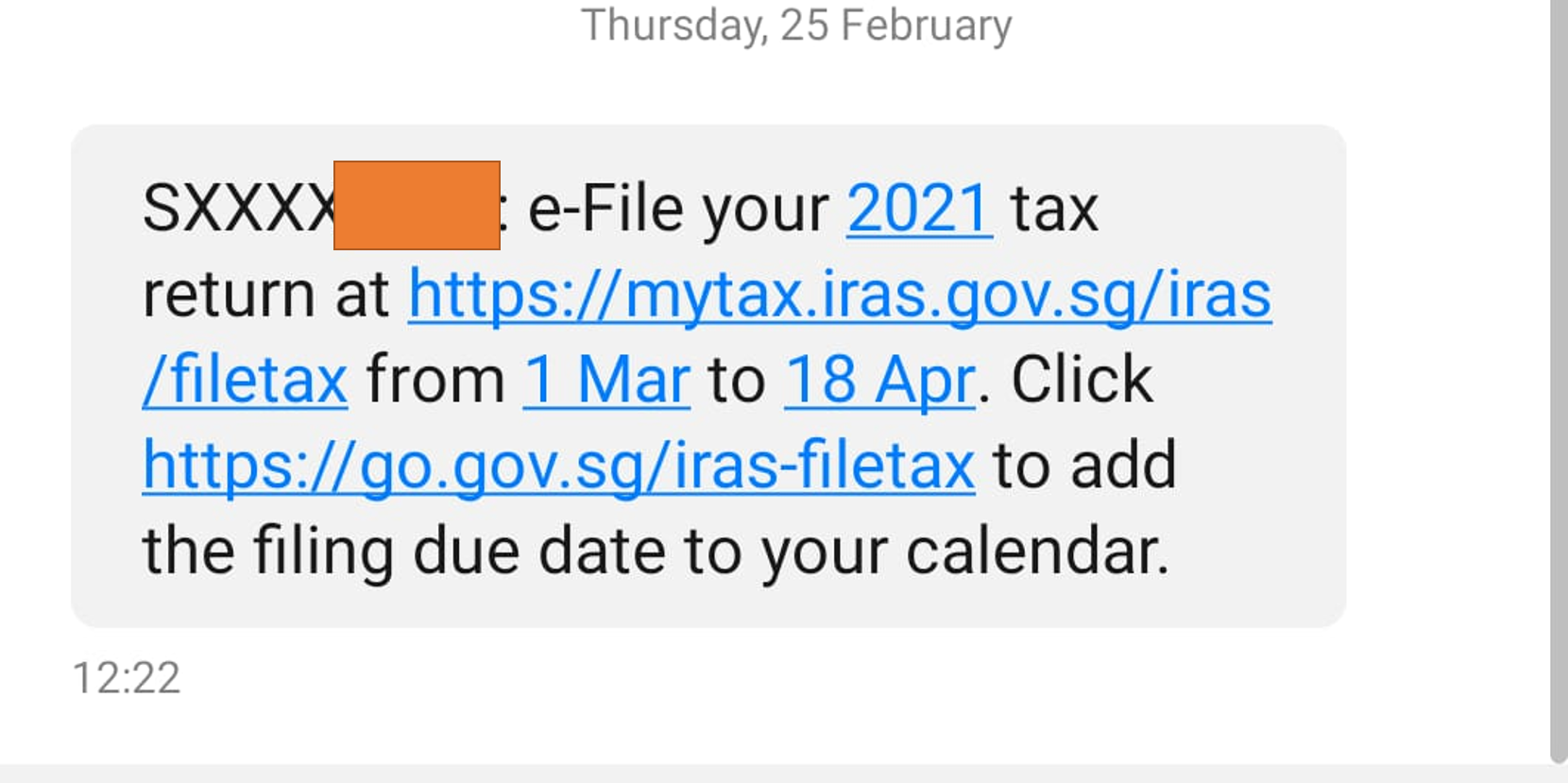

If you received a letter/SMS/form that tells you to file your income tax, you will have to log in and file it yourself. This sms below is one that I received from IRAS. Typically, most of my income have already be pre-filed as I’m a self-employed working with AIA.

Income Tax 2021 Filing

If you received a letter/SMS/form that tells you NOT to file your income tax, you don’t have to do it. But please verify if your information is correct and accurate.

If you didn’t receive anything from IRAS, you will still need to file a tax return if your:

annual net business income exceeded $6,000, OR

annual income (inclusive of rental income) was more than $22,000 last year

Tax Deductibles

Since 2020 is over, you can’t really do much changes into your deductibles. You can start planning for 2021 instead. In Singapore, we have a list of deductibles given to encourage social and economic objectives such as filial piety, family formation and the advancement of skills.

Income – Deductibles = Chargeable Income

As mentioned above, you will pay taxes on your chargeable income. This means that deductibles will play a big role in the taxes you are paying.

There were only two things certain in life Death and Taxes

Co-incidentally, these two can be well managed by proper financial planning or using insurance tools to achieve your financial goals. This article is meant to be a general article on how to pay taxes in Singapore. If you would like to know more, just comment on this post or contact me and I would love to have a conversation with you on the above.

Stay healthy. Stay Safe and pay your taxes.

Thank you for your contribution to nation building.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

If you are reading this, you probably have an amount of money in your SRS account. As the interest in the SRS account is 0.05%, you are also probably thinking of investing that amount. In the 6 Levels Wealth Karate, one of the key pillars of your financial journey is building up your investment portfolio and that includes your SRS account.

If you are unsure what SRS is, please refer to comprehensive SRS guide that was written previously.

Today, we focus on the 10 Investments you can consider using your SRS.

(Disclaimer: We will be explaining each concept with a real life examples. Please note that, those are not buy/sell recommendations. The suitability of the investment vehicle depends on each individual. Please talk to a competent financial advisor for more details.)

Investment #1: Fixed Deposits

A fixed deposit is an investment vehicle that pays account holders a fixed interest in exchange for depositing a certain sum of money for a certain period of time. It is very popular among the older generation as it is virtually risk free as long as the bank doesn’t collapse. Even if it does, your deposits are still protected, up to $50,000, thanks to the Singapore Deposit Insurance Corporation.

I have pulled up an example to showcase fixed deposits. It is worth noticing that after the 13th month, the interest will become more significant. Also if you are putting your money for 6 months or less, the interest is 0.05% which is indifferent for you to not put into a fixed deposit anyway.

10 SRS Investments to Consider Especially if you are 40 and older fixed deposit

Investment #2/3/4: Singapore Government Securities

Singapore Government Securities are debt instruments that are fully backed by the Singapore Government. Singapore Government Securities includes Singapore Saving Bonds (SSB), SGS Bonds and also Treasury Bills.

For SSB and SGS Bonds, you will receive interest every 6 months. If we put the definition loosely, it means you are lending money to the Singapore Government to receive a interest.

For Treasury Bills, it does not issue interest/coupons. You will receive the face value at maturity. If we put the definition with an example loosely, you are paying $0.95 now to get $1.00 in a xxx time frame.

I have taken a screenshot of the detailed comparison of the 3 securities here. Do check out more information on the MAS Website.

DBS has also created an extremely useful step by step guide to help you in your purchase of the securities.

10 SRS Investments to Consider Especially if you are 40 and older Singapore Government Securities

Investment #5: Bonds

Bonds are basically debt instruments as mentioned above. However, I have separated bonds with the above SSB/SGS bonds because bonds can issued by companies etc. In a simple nutshell, the better the credit rating of the bond issuer, the lower the returns (or the coupon rate).

There are 3 main ones that you can purchase. Firstly, individual bonds, Bond ETF Funds, and Bond Unit Trusts (more on ETF/Unit trust in a while).

A popular example of a bond is the Astra V PE Bonds Class A-1. It was popular because the bond was issued by Temasek Holding’s subsidiary, Azalea. It was offering 3.85% annual interest for it’s bonds and was 7.2x oversubscribed in 2019. In this bond, you can see their investment diversification on their website. (Again, this is not a recommendation)

10 SRS Investments to Consider Especially if you are 40 and older Astrea V Bonds

Investment #6: Stocks

A stock (or equity) is a security that represents the ownership of a fraction of a corporation. Loosely define, you are a partial owner of the company when you purchase the company’s stock.

There are several methodologies that you can use to invest in stocks. Recently, the hottest topic around is whether Value Investing Is Dead Or Maybe Not. I have also written about a hidden gem in the Singapore Stock Exchange that might have short term capital appreciation in the next 6 months. If you are interested in banks, I have written about DBS business and opportunity.

The example I will be using is an evergreen stock in the Singapore Stock Exchange called Singtel. It is important to know what you are investing in. Most people only recognized Singtel for its’ mobile and data internet service, but do you know that >50% of their revenue comes from something else? Stock investing require greater skills and mental fortitude. I strongly encourage you to learn more about stock investing before dipping your toes into it.

PS: You can only invest in stocks listed in the Singapore Stock Exchange using your SRS.

10 SRS Investments to Consider Especially if you are 40 and older Singtel Business Revenue

Investment #7: Reits

Reits (real estate investment trusts) are the same as stocks except they invest only in real estate. They tend to have higher distribution yield as compared to stocks because of their consistent cashflow from rental. Similarly, you can only invest in a Reits that is listed in Singapore. At the end of 2019, Singapore has 35 REITs, six stapled trusts and two property trusts.

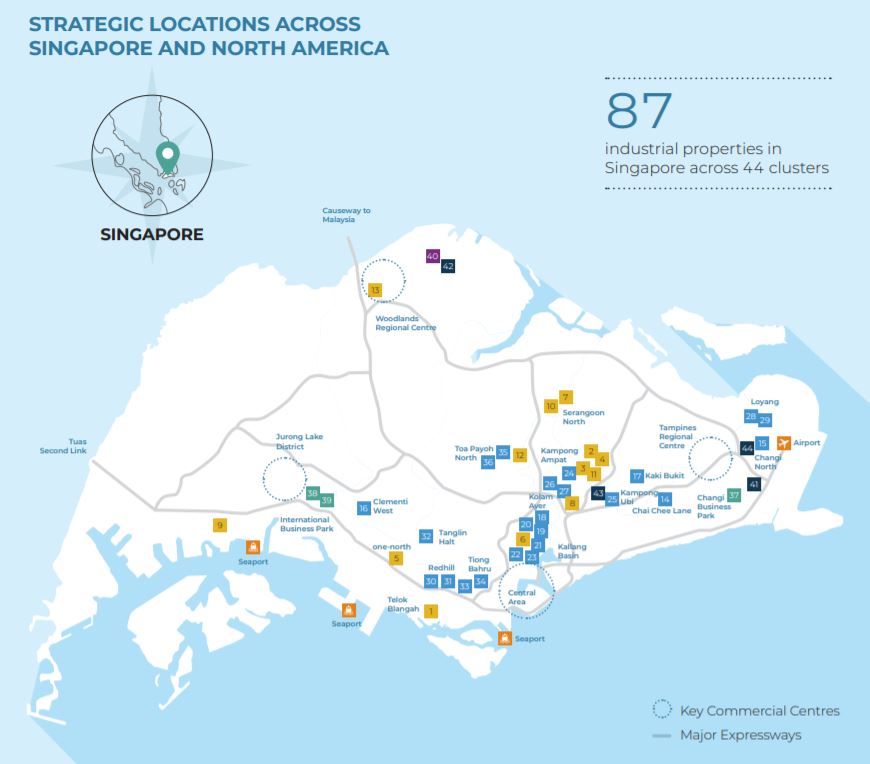

An example is the Mapletree Industrial Reits. Its principal investment strategy is to invest in a diversified portfolio of income-producing real estate used primarily for industrial purposes in Singapore and income-producing real estate used primarily as data centres worldwide beyond Singapore, as well as real estate-related assets.

As at 30 September 2020, MIT’s total assets under management was S$6.6 billion, which comprised 84 properties in Singapore and 27 properties in North America (including 13 data centres held through the joint venture with Mapletree Investments Pte Ltd). MIT’s property portfolio includes Data Centres, Hi-Tech Buildings, Business Park Buildings, Flatted Factories, Stack-up/Ramp-up Buildings and Light Industrial Buildings.

10 SRS Investments to Consider Especially if you are 40 and older Mapletree Industrial REITS

Investment #8: ETFs

ETFs are called exchanged traded funds. An ETF typically replicates a specific index (for example, the Straits Times Index or the Singapore Market). The main feature of an ETF is that it is passively managed and do not try to outperform the underlying index. They usually have lower fees and charges as compared to actively managed investment funds such as unit trust.

One example is the SPDR® S&P 500® ETF Trust (S27). They are investing in the 500 companies in the S&P500. You can take a look at the top 10 holdings of this ETF.

10 SRS Investments to Consider Especially if you are 40 and older SPDR ETF

You could invest in a dividend fund, a growth strategy fund, a commodity fund, a growth strategy in emerging countries, a dividend strategy fund in a developed market (I think you get the point now), etc. Because unit trust is so broad, we will not be giving an example. I feel it is best to work with a financial advisor to discuss and find the most appropriate unit trust for you.

Investment #10: Single Premium Insurance Product

A single premium insurance are usually retirement/annuity/accumulation products. Not all insurance products can be bought using the SRS.

There are 2 strategies in general. One being a lump sum payout at maturity or a stream of income in the future, starting from a date of your choice. A portion of your investment returns are guaranteed as compared to investment #5/6/7/8/9. This appeals to those that are seeking a more conservative and steady income stream during retirement. There is also a possibility of bonuses that are non-guaranteed.

Please feel free to contact me to have more information on these.

PS: An article isn’t complete unless there is a photo of retirement with 2 loving elderly =)

10 SRS Investments to Consider Especially if you are 40 and older Retirement

Final thoughts by Wealthdojo

Whichever the financial vehicle that you are deciding, it is important to understand and know your risk profile, knowledge level, budget, income etc to make a good investment decision.

I wish you all the best in your investment. Do contribute to your SRS before 31 Dec if you wish to have tax benefits for your financial year.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

It is 45 days before the end of the year. Have you accomplished your 2020 goals? Whether it is a financial goal or a fitness goal, the good news is that we have another 52 days left.

In the 6 Levels Wealth Karate, we talked about many strategies while you embark on your wealth management journey. Today, I want to congratulate each and every one of you for being invested in your financial journey. If my blog has helped you, I would appreciate if you could comment how you have benefited in the comments below.

If you have not started, it’s okay. This article will be the easiest way to start to start.

This is because it is likely that your income is more than $80,000. There will be great substantial tax savings. Plus, we might need liquidity for housing/renovation/marriage/children purposes before that. This will post an liquidity issue. Someone 40 and above might fit into such a category.

In the “best case scenario”, you will be withdrawing $40,000 per year and that income will be tax-free (assuming you are not working).

Please read the above post to learn more about the details.

The $1 SRS Strategy

This strategy is the most important strategy of all. This is because we need to first start!

Yes. Most goals failed because they have not even started. Think about it, did you “renew” your 2019 new year’s resolution in 2020 because you didn’t accomplished it in 2019? It need not be a financial goal. What about your fitness goal? What about your learning goal? If this seems like the case, you have the opportunity to change now. By doing so today, you will shave off up to 3 years of your retirement age. If that is not enough, all it takes is $1.

How is that possible? Let’s gather a few facts.

You can make penalty free withdrawals from your SRS on or after the statutory retirement age (currently at 62) that was prevailing at the time of your first SRS contribution. In 2019 National Rally Speech, PM had announced the retirement age to be raised to 63 in 2022 and 65 in 2030.

This will mean that if you still refuse to open your SRS account by 2022, your penalty free withdrawal will increase by 1 year. If you still refuse to open your SRS account by 2030, your penalty free withdrawal increase by 3 years.

The minimum that you can contribute is a grand total of $1. If you are above 18, all you need is to contribute $1 to “lock in” your retirement age to be 62.

The $1 SRS Strategy Retirement Age

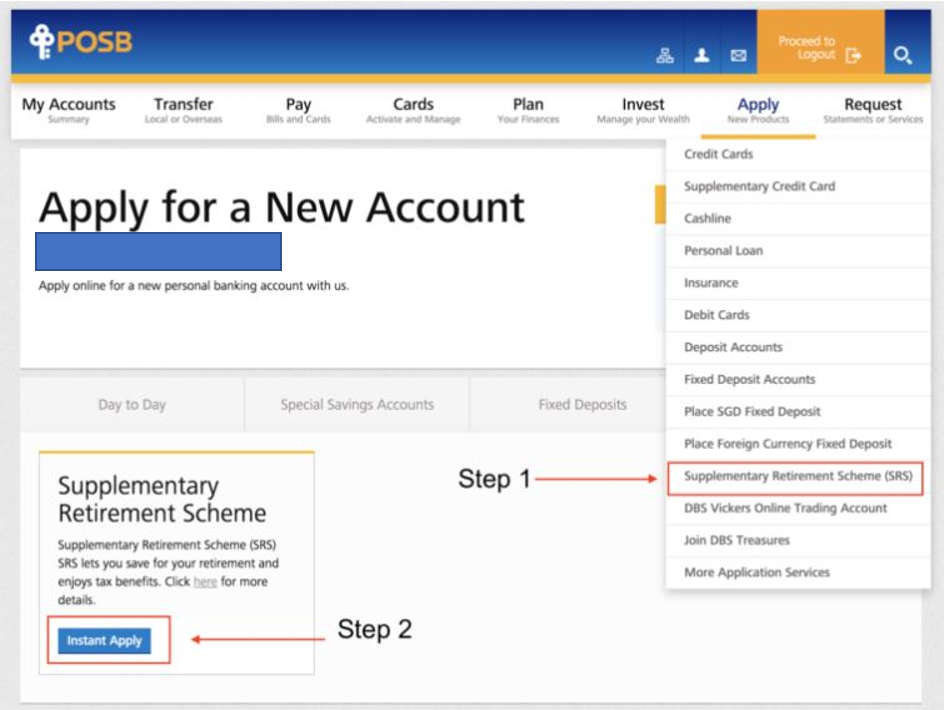

Your 1 Minute Opening Guide

You no longer need to go to the physical bank branch to open up your SRS account anymore. All it takes is 1 minute.

This is the way I do it. My personal SRS account is with DBS (for convenience sake). You can also open your SRS account with OCBC or UOB. It is only 2 steps, click click and you will have an SRS account. If you are unsure how much to contribute, you can always contribute $1 to your SRS account first to “lock in” your retirement age.

The $1 SRS Strategy DBS

This guide serves to let you under how $1 can lock in your statutory retirement age. In fact, do it now! Log into your DBS/OCBC/UOB internet account and do it now!

What can you do with your SRS account?

By popular demand on my Telegram group, I’m currently writing on how to invest using your SRS account now. If you have any questions that you want to be addressed in that article, do drop me a comment and I will include that in the article.

We wish you the very best in your 2020 goals. Otherwise, we hope that this will be your first financial milestone.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

In this article, we will talk about 3 potential scenarios (i) if you are a foreigner and continue to stay in Singapore (you should!) (ii) if you are a foreigner but decide to leave Singapore (iii) if you are local and intend to retire in overseas (Thailand, Phuket, you name it).

3 things you need to know about SRS if you plan to leave Singapore: Don’t leave =(

I’m a Singaporean and proud to be one. Singapore is a wonderful country. You should not leave =). Unfortunately, I do meet people who love Singapore but have no choice but to leave because they were asked to relocate to another country. Anyway, let’s set the context for the SRS. Most people will probably be concerned if it is worth it to contribute to their SRS when long term stay in Singapore is not confirm. We will touching on that.

SRS Early Withdrawal Penalty (Local and Foreigner)

Withdrawal after retirement age (current age 62): You can start making penalty-free withdrawal from your SRS account. You will only be taxed 50% of the amount you withdraw for the calendar year.

Withdrawal before retirement age (current age 62): Although you can make withdrawal from your SRS account at any time that you want, you will be subjected to a penalty of 5% of the amount withdrawn. In addition, the full amount withdrawn will also be subject to income tax.

There are other special circumstances which we will not be going into detail (Death/Medical Grounds/Bankrupt)

SRS Additional Withdrawal Criteria (Foreigner)

As a foreigner, you can withdraw your SRS monies without the 5% penalty if you meet the following criteria:

(i) a foreigner for a continuous period of at least 10 years preceding the date of withdrawal.

(ii) one lump sum after maintaining your SRS account for at least 10 years from the date of your first contribution.

For such withdrawal, you will be taxed 50% of the withdrawal amount.

After understanding the above criteria, let’s consider a the few scenario that might happen to you.

Case #1: Foreigner and continue to stay in Singapore

James is a foreigner who is staying in Singapore for many years. When I first met James, he told me that he really love Singapore. He likes the sunny weather, he likes the hawker food (his favourite is chicken rice) and also a father of 2 beautiful young children.

He has an intention to stay in Singapore to raise his family.

James contributes to his SRS account every year. This is because as a foreigner, he does not have CPF contribution. By contributing to the SRS, he is able to reduce his taxable income, save on taxes and also save for retirement.

James is 45 this year and he is plan to contribute the full $35,700 into his SRS every year. He makes around $160,000 a year. Assuming no other personal tax deduction.

Without SRS: James pays $13,950 of taxes that year.

With SRS: James pays $8,595 of taxes that year. (His chargeable income is $160,000 – $35,700)

In total, he saves $5,355 worth of taxes that year. He also saves $35,7000 in his SRS which he can use to invest for his retirement.

In 10 years time, he save a total of $53,550 worth of taxes. At the same time, he would have accumulated nearly $481,462 if he decides to invest his monies in his SRS assuming it grows at 4%. He can decide if he wants to withdraw the lump sum.

If he does so, he have to pay 50% taxes on withdrawal amount. Let’s assume he does not have any income that year. He will be taxed on $241,000 (50% of $481,462). He pays a tax of $28,945. He saves about $24,605 ($53,550-$28,945) if he contributes to SRS. In this case, he benefits from this.

However, James may not want to do this at all. At age 55, he is still young and most likely have a good income, saving or investment to depend on if he does proper wealth management. James is a happy man.

3 things you need to know about SRS if you plan to leave Singapore happy family

Case #2: Foreigner and decides to leave Singapore

In an unfortunate case where you have to leave Singapore, there are some strategies that you might want to consider for the SRS. I met Lucy a few years back. Lucy has been in Singapore for 3 years now but have not contributed to her SRS. She’s working in an MNC in Singapore and earns around $160,000. She fears that the economic downturn will affect her job opportunities in Singapore and asked to be returned to her country. This has been escalated due to COVID-19. Similarly, if she contributes $35,700 to her SRS, these are her numbers.

Without SRS: Lucy pays $13,950 of taxes that year.

With SRS: Lucy pays $8,595 of taxes that year. (Her chargeable income is $160,000 – $35,700)

In total, she saves $5,355 worth of taxes that year. She also saves $35,7000 in her SRS which she can use to invest for her retirement.

What if Lucy were to leave Singapore? Her fears are valid. It would mean that $35,700 would be stuck in her SRS. What if she leaves Singapore AND really needs the money? In this unfortunate situation, she will have to pay a 5% penalty and also be taxed on 100% of the withdrawal amount. This can be avoided if Lucy plans using the 6 Level Wealth Karate System.

Ideally, she can wait for 10 years from her first contribution to avoid the penalty and be taxed on 50% of the lump sum.

3 things you need to know about SRS if you plan to leave Singapore: I don’t want to go

Case #3: Local but wants to retire overseas

This has been a dream of many Singaporeans. Andrew has been working in Singapore all his life and contributes to his SRS account regularly. He has been telling his colleagues about his retirement which is happening in a few years time. He dreams that he will be able to retire in Thailand. He enjoys Thai food a lot and can’t wake to wake up on the beach of Phuket every day for the rest of his life.

3 things you need to know about SRS if you plan to leave Singapore Phuket

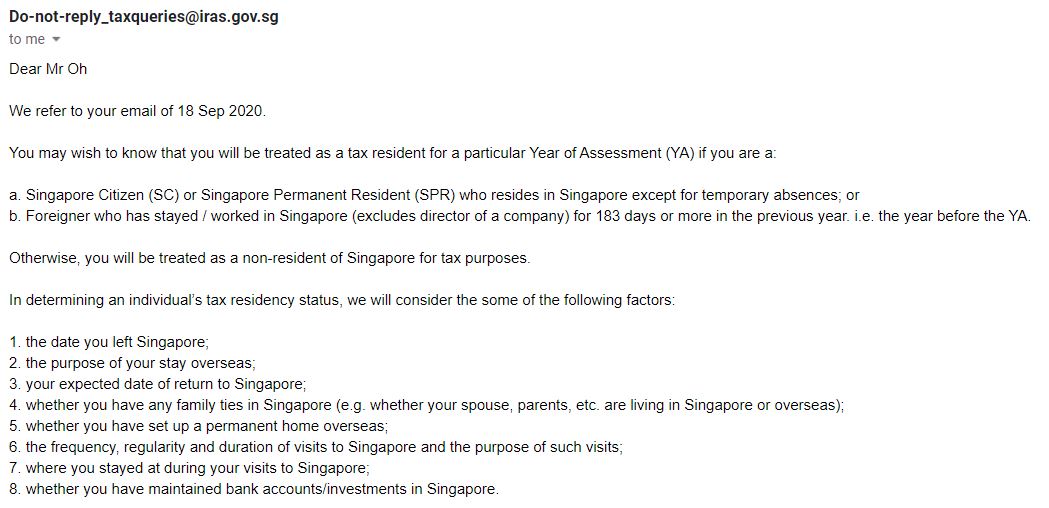

We are in the midst of checking if SRS will be taxed differently due to the change of tax residency. We will update this article accordingly.

Update: SRS will be taxed according to tax residency and it depends on the following factors.

3 things you need to know about SRS if you plan to leave Singapore Tax Resident

Final Thoughts

Please check in with your tax advisors for the above strategies. We also note that the rulings change from time to time so we want to be mindful about that.

Whether you are a local or a foreigner, it make sense to contribute to SRS (as discussed in the previous article). I will be talking about what to invest in using your SRS in the next article. Stay tune.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

During the end of the year, the topic of Supplementary Retirement Scheme (SRS) and Central Provident Fund (CPF) contributions will become frequently searched topics for wealth management. This is because for every additional dollar contributed, we might pay lesser in taxes. If you are 40 and older, this article is for you. We are going to talk about taxes, retirement and worse case situations.

5 things you need to know about SRS when you are 40 and older

#1 Quick Summary of SRS

SRS is a voluntary program started in 2001 to help individual (local and foreigners) to save more money for retirement. You are eligible for tax reliefs by contribution to SRS subjected to the cap of the personal income tax relief (currently $80,000). There is also a maximum that you can contribute to SRS (currently $15,300 for Singapore Citizens and Permanent Residents; and $35,700 for foreigners).

For example, I earn $100,000. I contribute $15,000 into my SRS. My taxable income will now be $85,000 (assuming I have not hit the cap of the personal income tax relief).

Your returns in the SRS account will be tax-free and 50% of the withdrawals from SRS are taxable at retirement.

Your contributions must be made before the 31 Dec of the year to quality (hence, the interest at the end of the year).

You can make withdrawals on or after the statutory retirement age (currently at 62) for you to enjoy penalty free withdrawals. Withdrawals are made in a 10 years window.

For investments in life annuities, the 10-year withdrawal period does not apply. So long as you continue to receive your annuity streams in perpetuity, 50% of the annual stream will be subject to tax.

A 5% penalty will be imposed for early withdrawals.

For more information about withdrawals, head over to IRAS withdrawals to understand more.

#2 The Best Case Scenario

The best case scenario is to have $400,000 in your SRS account at the age of 62 and you are not working by then. We assume that we will be drawing out $40,000 evenly over the next 10 years. Since 50% of the amount withdrawn will be taxable, the taxable income is $20,000 (assuming no other income). At $20,000, there is no income tax payable.

This rigid best case scenario creates a conundrum because it creates a happy problem that you have ALOT MORE than $400,000 due to excellent investment returns AND you still have a well paying job by then.

#3 The “Worse Case” Scenario

Suppose you are 30 year old today and contribute the maximum of $15,300 into the SRS account every year until age of 62. If your ROI is 20%, you would have $31 million in your SRS account. You would have to withdraw around $3 million yearly and be subjected to the highest income bracket.

If we manage our expectations and have a reasonable ROI of 5%, you would have $1.2 million in your SRS account. In this case, you would have to withdraw roughly $120,000 yearly. If you are still working and at the peak of your career getting a good income, you will be possibly subjected to a highest income bracket.

The “worse case” is to have really good investment skills and still be working by then. However, I feel this as a “happy” problem to have.

#4 What if I’m just a normal human being?

$1.2 million sounds big and you might not even be sure you will still have a job then at 62. Most of my client ask me what if they are a normal human being, how does SRS still make sense to a layman?

Firstly, we have to start with the question of contribution. How much should you make a year before SRS contributions make sense?

SRS is a tax planning tool. Hence, it is important to know at which chargeable income bracket (after CPF contribution, tax relief) will it make sense for us to contribute to SRS.

Personally, SRS contribution will start to make sense after the $80,000 chargeable income bracket. Any other income after the $80,000 is subjected to a tax rate of 11.5%. Hence, I find it reasonable to contribute to SRS unless I can find an investment instrument that can give me 11.5% easily. Of course, there are other reasons as well.

#4.1 Tax Savings

To give an example, Amy earns $120,000 annually (after all personal tax relief).

Without SRS, she pays $7950 on taxes.

With SRS, her chargeable income becomes $104,700. She now pays $6190 on taxes.

She saves $1760. (which is a probably an extra month of family expenses)

However, in a situation where by you need liquidity for big purchases such as down-payment for a property, you might want to skip this year’s contribution. The balance of liquidity and tax saving should be taken into consideration.

#4.2 Emergency Funds

If you already have money in your SRS and have a URGENT need for cash, you can still withdrawal from SRS with a 5% penalty instead of having it locked up like the CPF. Of course, we ideally do not want to withdraw from our SRS. However, in an event of a unforeseen circumstances, the funds are still available.

#5 Then why after age 40?

I’m assuming that after age 40, it is likely that our income is more than $80,000. Plus, we might need liquidity for housing/renovation/marriage/children purposes before that. There is also an (irrational) fear is that if we contribute too early, we might compound it too much by then.

Hence, 40 years is ideal because there will be possible substantial tax saving, not having a liquidity issue and also closer to retirement age (lesser compounding period).

A potential solution to the “worse case” scenario is to get an annuity (but you will still be effectively taxed on half the annuity’s payouts every year).

#6onus How should you open a SRS account?

To open a SRS account, simply go to the 3 SRS operators (DBS/POSB, UOB & OCBC) website and you can do it online. You can register an account with any of them. There is little difference which bank you choose because you can invest in SRS approved assets from any institutions.

I suggest that you wait until the end of the year before applying. Typically, there are promotions to open a SRS account at the end of the year. On a side note, I’m don’t think there will be a promotion this year (2020) due to the COVID-19 situation. The banks have also been reducing their benefits this year.

5 things you need to know about SRS when you are 40 and older OCBC Promotion 2017

Final Thoughts

I believe that SRS is a great tax saving tool for you if you are 40 and above. Your contribution might save your family one month worth of household expenses. When we are younger, it is important to balance tax-saving and liquidity. Upon retirement, SRS can provide a source of income for us in addition to possibly rental, dividends etc.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.