It is the Supplementary Retirement Scheme (SRS) contribution season. If you are 40 and above, do check out my previous post on the 5 things you need to know about SRS. Interestingly, someone emailed me on my 6 Level Wealth Karate System Page to ask about what will happen to their SRS account if they leave Singapore.

In this article, we will talk about 3 potential scenarios (i) if you are a foreigner and continue to stay in Singapore (you should!) (ii) if you are a foreigner but decide to leave Singapore (iii) if you are local and intend to retire in overseas (Thailand, Phuket, you name it).

I’m a Singaporean and proud to be one. Singapore is a wonderful country. You should not leave =). Unfortunately, I do meet people who love Singapore but have no choice but to leave because they were asked to relocate to another country. Anyway, let’s set the context for the SRS. Most people will probably be concerned if it is worth it to contribute to their SRS when long term stay in Singapore is not confirm. We will touching on that.

I would also need to point out the withdrawal tax concession and the 5% early withdrawal penalty.

SRS Early Withdrawal Penalty (Local and Foreigner)

Withdrawal after retirement age (current age 62): You can start making penalty-free withdrawal from your SRS account. You will only be taxed 50% of the amount you withdraw for the calendar year.

Withdrawal before retirement age (current age 62): Although you can make withdrawal from your SRS account at any time that you want, you will be subjected to a penalty of 5% of the amount withdrawn. In addition, the full amount withdrawn will also be subject to income tax.

There are other special circumstances which we will not be going into detail (Death/Medical Grounds/Bankrupt)

SRS Additional Withdrawal Criteria (Foreigner)

As a foreigner, you can withdraw your SRS monies without the 5% penalty if you meet the following criteria:

(i) a foreigner for a continuous period of at least 10 years preceding the date of withdrawal.

(ii) one lump sum after maintaining your SRS account for at least 10 years from the date of your first contribution.

For such withdrawal, you will be taxed 50% of the withdrawal amount.

After understanding the above criteria, let’s consider a the few scenario that might happen to you.

Case #1: Foreigner and continue to stay in Singapore

James is a foreigner who is staying in Singapore for many years. When I first met James, he told me that he really love Singapore. He likes the sunny weather, he likes the hawker food (his favourite is chicken rice) and also a father of 2 beautiful young children.

He has an intention to stay in Singapore to raise his family.

James contributes to his SRS account every year. This is because as a foreigner, he does not have CPF contribution. By contributing to the SRS, he is able to reduce his taxable income, save on taxes and also save for retirement.

James is 45 this year and he is plan to contribute the full $35,700 into his SRS every year. He makes around $160,000 a year. Assuming no other personal tax deduction.

Without SRS: James pays $13,950 of taxes that year.

With SRS: James pays $8,595 of taxes that year. (His chargeable income is $160,000 – $35,700)

In total, he saves $5,355 worth of taxes that year. He also saves $35,7000 in his SRS which he can use to invest for his retirement.

In 10 years time, he save a total of $53,550 worth of taxes. At the same time, he would have accumulated nearly $481,462 if he decides to invest his monies in his SRS assuming it grows at 4%. He can decide if he wants to withdraw the lump sum.

If he does so, he have to pay 50% taxes on withdrawal amount. Let’s assume he does not have any income that year. He will be taxed on $241,000 (50% of $481,462). He pays a tax of $28,945. He saves about $24,605 ($53,550-$28,945) if he contributes to SRS. In this case, he benefits from this.

However, James may not want to do this at all. At age 55, he is still young and most likely have a good income, saving or investment to depend on if he does proper wealth management. James is a happy man.

Case #2: Foreigner and decides to leave Singapore

In an unfortunate case where you have to leave Singapore, there are some strategies that you might want to consider for the SRS. I met Lucy a few years back. Lucy has been in Singapore for 3 years now but have not contributed to her SRS. She’s working in an MNC in Singapore and earns around $160,000. She fears that the economic downturn will affect her job opportunities in Singapore and asked to be returned to her country. This has been escalated due to COVID-19. Similarly, if she contributes $35,700 to her SRS, these are her numbers.

Without SRS: Lucy pays $13,950 of taxes that year.

With SRS: Lucy pays $8,595 of taxes that year. (Her chargeable income is $160,000 – $35,700)

In total, she saves $5,355 worth of taxes that year. She also saves $35,7000 in her SRS which she can use to invest for her retirement.

What if Lucy were to leave Singapore? Her fears are valid. It would mean that $35,700 would be stuck in her SRS. What if she leaves Singapore AND really needs the money? In this unfortunate situation, she will have to pay a 5% penalty and also be taxed on 100% of the withdrawal amount. This can be avoided if Lucy plans using the 6 Level Wealth Karate System.

Ideally, she can wait for 10 years from her first contribution to avoid the penalty and be taxed on 50% of the lump sum.

Case #3: Local but wants to retire overseas

This has been a dream of many Singaporeans. Andrew has been working in Singapore all his life and contributes to his SRS account regularly. He has been telling his colleagues about his retirement which is happening in a few years time. He dreams that he will be able to retire in Thailand. He enjoys Thai food a lot and can’t wake to wake up on the beach of Phuket every day for the rest of his life.

We are in the midst of checking if SRS will be taxed differently due to the change of tax residency. We will update this article accordingly.

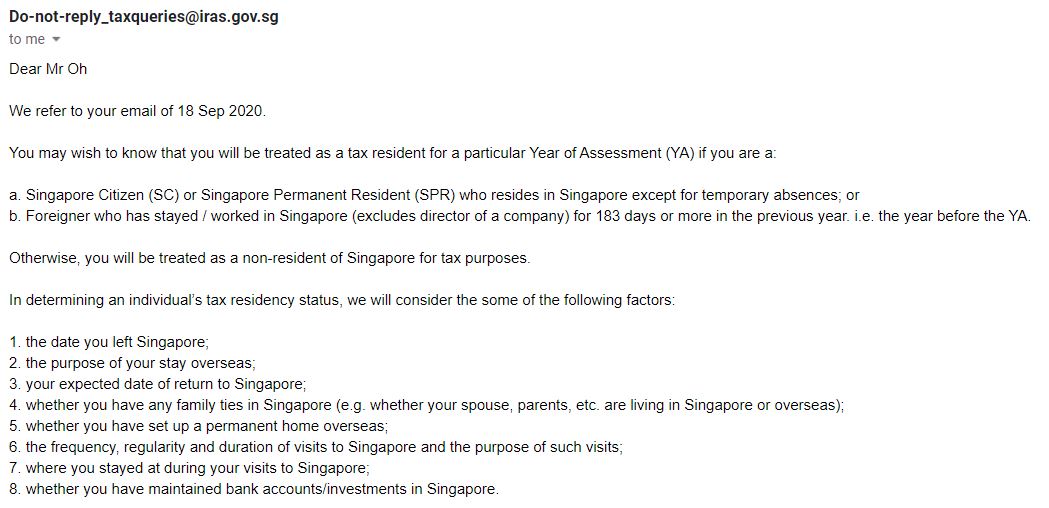

Update: SRS will be taxed according to tax residency and it depends on the following factors.

Final Thoughts

Please check in with your tax advisors for the above strategies. We also note that the rulings change from time to time so we want to be mindful about that.

Whether you are a local or a foreigner, it make sense to contribute to SRS (as discussed in the previous article). I will be talking about what to invest in using your SRS in the next article. Stay tune.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

Feel Free To Reach Out To Share Your Thoughts.

Contact: 94316449 (Whatsapp) chengkokoh@gmail.com (Email)

Telegram: Wealthdojo [Continuous Learning Channel]

Reviews: About Me

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

Hi

For the 3rd scenario, if one is a retiree living in Thailand without any earned income or professional fees but withdrawing from SRS, the individual is taxed at Non-resident rates for the withdrawal amount?

Hi Ci2fi,

That’s a great question. I posted the question to IRAS and they replied me with the photo i attached above. Apparently, it depends on a couple of factors to determine whether one is a tax resident or a non tax resident.

Hope that answers your question!

[…] There were various strategies. Properties, Tax Lien, Value Investing, Options Trading, E-commerce, SRS hacks, you just have to name […]

[…] this is one question that is commonly asked: 3 things you need to know about SRS if you plan to leave Singapore. This is for people who wants to live in another country during […]

Yes, I love this place

I enjoy what you guys are usually up too. This type of clever work and reporting! Keep up the good works guys I’ve included you guys to our blogroll.