In August 2021, MOH first talk about financing cancer treatments in Singapore. The cancer drug list was then announced to be take into effect in April 2023. I believe this is going to affect healthcare cost in Singapore. However, I don’t see many people being aware of this. In this article, I will talk about what cancer drug list is and the potential impacts on your healthcare costs in the years to come.

Why aren’t we talking about the cancer drug list CDL

Why cancer?

We are lucky that not all critical illness have a drug list now. In my knowledge, cancer drug list was created to finance future cancer treatments in Singapore. By statistics, cancer is the number 1 causes of death in Singapore. As you can see in the table below, cancer is number 1 followed very closely by ischaemic heart diseases.

Singapore’s healthcare cost will definitely be impacted if more and more people suffers from cancer. At the same time, if treatment cost were to increase, the cost may spiral out of control.

As you can see that there will now be a limit on how much medishield life can claim per month for each drug. If this is insufficient, the patient will have to pay cash for it.

I have a shield plan. Will I be affected?

Insurance companies selling the integrated shield plan will have to follow MOH guidelines to change their plans accordingly for claims on cancer treatments. I believe that each insurance will give a different limit to their coverage. Let’s take NTUC enhanced incomeshield to illustrate an example.

Cancer Drug List Example NTUC

You can see that under point 6, depending on the plan type that you are on, the multiple of your limits will be different. For example, if I’m holding on to the Enhanced Advantage, I will be having a 4X MSHL (Medishield Life Limited).

You then have to go to the cancer drug list to find the drug that you need to have find the limit. If the MSHL is $2000, your claim limit under NTUC Enhanced Advantage will be $8000 (4X of $2000) per month. This is before any co-insurance and deductible or co-payment.

Please do get a professional financial advisor to clarify the type of coverage that you have as I have no intension to go deeper into the calculations of the claims.

We have to ask whether we have enough savings to “afford” the second critical illness or cancer especially during relapse.

This is something that you will have to discuss with your professional financial advisor.

Final Thoughts By Wealthdojo

I believe that there will be more of such healthcare treatment cost changes in Singapores in the years to come. While having coverage it important, it is also important to build an asset that will be able to sustain and maintain such coverages in the years to come.

Wishing you good health!

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

Insurance is an expense, until it is not. Here, I wish to address the power of adding critical illness coverage into your portfolios.

What Is Critical Illness Coverage?

Critical illness coverage is a type of insurance that provides financial protection in the event of a covered critical illness, such as cancer, heart attack, or stroke. Many people think that traditional health insurance is enough to cover all medical expenses, but this is not the case.

5 Reason Why You Need Critical Illness Coverage

High Cost of Critical Illnesses: The cost of treating critical illnesses can be astronomical, even with health insurance. Between co-payments, deductibles, and uncovered expenses, it is common for patients to incur significant out-of-pocket costs when diagnosed with a critical illness. In addition, many people are unable to work during treatment, leading to loss of income and additional financial strain. Critical illness coverage can provide a lump sum payment to help cover these costs, giving your clients peace of mind and financial security.

Limitations of Traditional Health Insurance: Traditional health insurance policies typically have limits on the amount of coverage they provide. If your client requires an extended stay in the hospital or an expensive medical procedure, they may quickly reach their coverage limits, leaving them responsible for the remaining expenses. Critical illness coverage, on the other hand, provides a lump sum payment that can be used to pay for any expenses, including those not covered by traditional health insurance.

Maintaining Quality of Life: A critical illness can have a profound impact on a person’s quality of life. Not only do they have to cope with the physical and emotional toll of the illness, but they also face the financial burden of medical expenses. Critical illness coverage can provide the financial resources necessary to maintain your client’s quality of life, allowing them to focus on recovery instead of worrying about finances.

Protecting Savings and Investments: When a critical illness strikes, the financial impact can be devastating. In addition to medical expenses, there may also be loss of income, which can quickly deplete savings and investments. Critical illness coverage can help protect your client’s financial future by providing a lump sum payment that can be used to cover expenses and maintain their standard of living.

Peace of Mind: Perhaps the most important benefit of critical illness coverage is the peace of mind it provides. Knowing that they are protected against the financial impact of a critical illness can allow your clients to focus on their recovery and not worry about how they will pay for their medical expenses. This peace of mind is invaluable and can greatly improve their overall well-being during a difficult time.

Final Thoughts

In conclusion, critical illness coverage is an essential part of any financial portfolio. The high cost of treating critical illnesses, the limitations of traditional health insurance, and the potential loss of savings and investments can all be mitigated with critical illness coverage.

By providing a lump sum payment to cover expenses and protect your client’s financial future, critical illness coverage can give them the peace of mind they need to focus on their recovery. As a world-class financial planner, it is important to educate your clients on the benefits of critical illness coverage and help them determine the right coverage for their specific needs.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

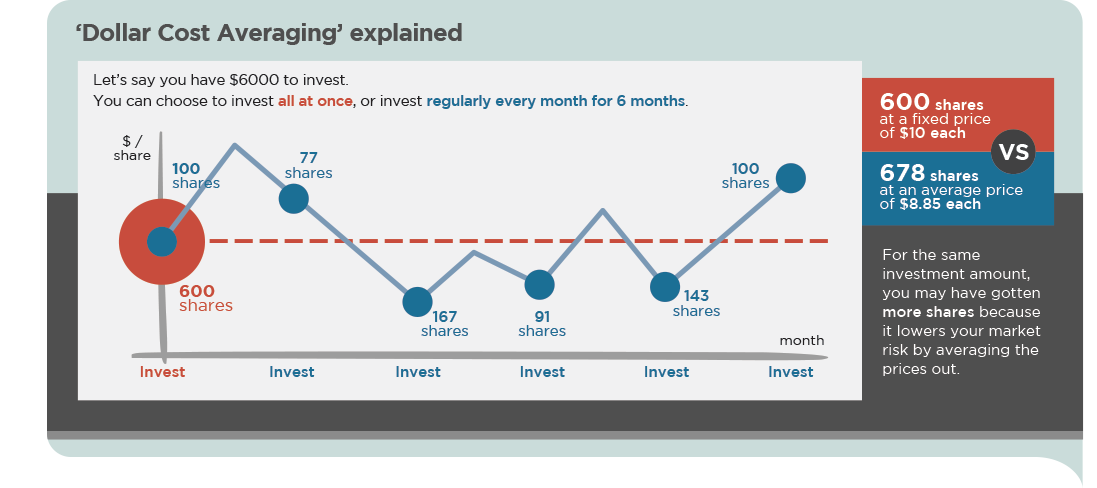

You might be thinking this is “another of those dollar cost averaging article”. I assure you that this is not. It is always during a Bear Market Survival that the topic of dollar cost averaging surfaces. Rarely, this topic is popular during a upward trending market.

Once a for all, I will discuss on the value of dollar cost averaging and what it can do in your portfolio. If you have been investing in China over the last year, you might think that dollar cost averaging is not working on China’s stocks? Read on and consider the pros and cons.

What is Dollar Cost Averaging (DCA)?

Dollar Cost Averaging is a popular investment method of investing equal amounts of money over a period of time. The opposite of this would be to invest a lump sum of money at once. I will leave you to read up about summary of DCA in this photo below.

One question you can ask yourself today ( 1st June 2022), are you still averaging down?

The Pros

Simple and systematic (if you set rules that continuously invest during ups and down): You don’t really “think” when you employ a DCA strategy. You simply trust the system and invest through the ups and downs. It will work BEST if it is via auto-transfer rather than manually transferring.

Downside protection: In a downward market, you will see a “bigger lost” if you do a lump sum strategy. For example, if the market corrected 20% in a month, your initial investment of $100,000 will be left with $80,000 (lost of $20,000). Now, if you do a DCA investing $10K per month, your initial investment will be left with $8,000 (lost of $2,000). You also have capital to continue investing at the “down” on the second month. For those that is retiring soon, this have great psychological benefits. I believe there is nobody that wants to lose 20% of their nest egg 6 months prior to retirement.

The Cons

FOMO (Fear of missing out): If this is an upward market, you risk missing out on the extra capital gains and compounding benefits. Using the same scenario as above, someone who invested $100,000 with a 20% run-up would make $20,000, while the investor DCA their first $10k would’ve only made $2k.

Being too passive: DCA works best if the asset have a long term upward tread in nature. If the underlying investments are downward/sideways moving (take a look at the Japan market), DCA will not be the best strategy.

Final Thoughts

A big shout out to one of the most loyal reader of Wealthdojo Mr Sinkie. He sums up my thoughts on DCA in a single sentence. “DCA works best for assets that are volatile but have very long history of uptrend”. Thank you for being so patient and contributing to the blog. For those that are interested in his elaboration (I think you should), go over to Bear Market Survival Tips.

Looking forward to more people commenting on the blog.

If you guys need help, please reach out. I will be more than happy to have a conversation with you.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

Genetic testing is getting more common as the medical scene evolves. If you find out that you have a “bad” result from the testing, you might fear whether your insurability will be impacted or worried that this is considered a pre-existing condition.

Please refer to the complete details on the LIA’s website. In an event of doubt, please refer back to the complete details as hyperlinked above.

Impact Of Genetic Testing On Insurance Singapore

A Brief Background

If you know that you have a higher chance to develop a condition in future (via those gene testing), you might load up on more insurance now. Insurers knowing that will ask for those test results. To then prevent this from happening, you might be deterred to undergo such testing anyway.

This Moratorium serves as a safeguard to prevent unfair discrimination during risk assessment (or insurance purchase) andadverse selection against insurer.

The Summary

Life Insurers in Singapore are NOT ALLOWED to ask applicants for their predictive genetic test results if they have taken the test. They will not be allowed to use those results for underwriting purposes.

However, given certain criteria are satisfied, life insurers may ask and use results of approved predictive genetic test for underwriting.

This is applicable for Singapore Residents only (Singaporeans, PR and valid pass holders). Non Singaporean residents are required to disclose genetic test results. If genetic test are done for biomedical research, applicants are not required to disclose those results.

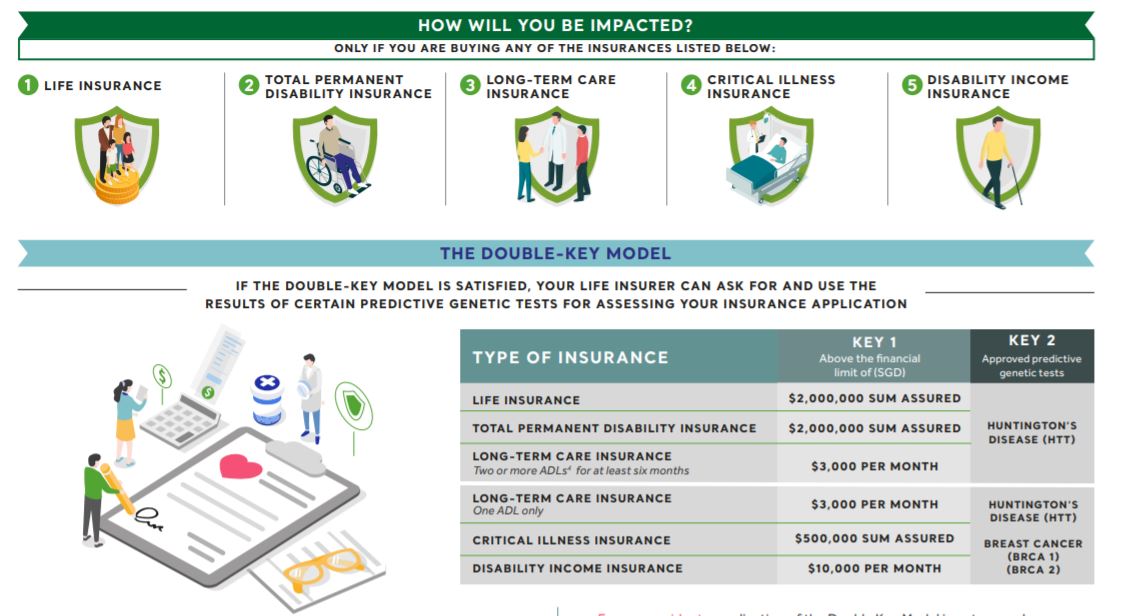

This is also applicable to the following insurance policies (Life Insurance, Total Permanent Disability Insurance, Critical Illness Insurance, Long Term Care Insurance, Disability Income Insurance) only.

The Criteria Of Being Asked

Impact Of Genetic Testing On Insurance Singapore LIA Infographic

There will be 2 keys that need to be satisfied before the life insurer can ask for and use the results of the certain predictive genetic tests.

The first key involves the sum assured you are considering. This sum assured refers to the total insurance coverage under all policies issued by insurers in Singapore (including concurrent insurance application). If you require a high sum assured, you might have satisfied the first key.

The second key involves the approved predictive genetic test for Huntington’s disease (HTT) and Breast Cancer (BRCA 1 and BRCA2). If you have done a predictive genetic test for the above, you would have satisfied the second key.

A simple example:

Sarah wants to buy $1,000,000 sum assured for critical illness. She would have satisfied key 1 because she is buying a sum assured more than $500,000 for critical illness.

If she have taken a predictive genetic test for breast cancer previously, she would have satisfied key 2.

As both keys are satisfied, Sarah will have to declare the result of the predictive genetic tests for her insurance application review.

Please refer to the complete details on the LIA’s website. In an event of doubt, please refer back to the complete details as hyperlinked above.

Stay safe and take care.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

That being said, Jack Ma has spoken wisdom on life, business and relationship. I have compiled Top 5 quotes which I particularly enjoy.

Hope that Chinese stocks turn around soon.

Jack Ma’s 5 Best Quotes On Life, Business and Relationship (Photo Source)

#1: On the path to success, you will notice the successful ones are not whiners, nor do they complain often.

After thinking for a long time, I personally felt that this should be the first one on the list (or on any list). If you ask someone what are the ingredients of success, you might get answers like family background, intelligence, the amount of money they have, the school they come from or being hardworking.

I believe that one point stands above all of those listed above. I’m not undermining any of them but without this one point, the rest might fall short.

The Right Positive Attitude.

In my industry and in the previous companies that I worked for, I noticed a similar pattern. The top performers are usually silent (of course they will be loud performers too) and they do what they are suppose to do diligently. Most of them look at the bright side and are often grateful for what they receive or accomplish in their work. Don’t be mistaken though. They do complaint (they are not saints). After releasing the negative energy, they will pick themselves up again and continue preserving in what they do. In time, most of them find success.

Observe the “more successful” colleagues that you have. Are they like what I have described? Do you want to be like that too?

#2: You need the right people, not the best people.

I was inspired by this book called Good To Great by Jim Collins. Jim Collins put together 5 years of research to explain how a company can grow from good to great. In one of the chapter, Jim Collins writes about “getting the right people on the bus“. He didn’t say the best people, but the right people.

The right people or team will figure out how to drive the bus to the direction they want. I believe that everyone gives out a different kind of energy and it is your job (as a leader) to manage that energy. In the world, there are really smart people/best people out there. But if they won’t be able to have the right resonance with the team, they are not right at all. The bus might be driven in a different direction or be broken down entirely.

The right culture takes time to build up and seconds to be broken down. You might have friends who “overstayed” in a role because they enjoyed their colleagues company too much. You probably might have heard of friends who quit their jobs immediately because of a bad manager.

The book Good To Great will give a different dimension in explaining this.

#3: When people think too highly of you, you have the responsibility to calm down and be yourself.

One word can summarise this entire sentence: Ego. This comes as a bad joke because I felt that ego might have gotten better of Jack in the last few years.

As we become more successful and people start looking up to you, I believe it is important to remember our roots and how we get there. I have met people who got successful very quickly and (very quickly as well) became arrogant. I like this quote from Will Smith: Money and success don’t change who we are; they merely amplify what is already there. People will see how you treat people and that is an indication on who you are as a person whether successful or not.

The price of ego could be a heavy one and it is up to us to have humility whether successful or not.

What kind of person do you want to be?

#4: When doing sales, the first people who will trust you will be strangers. Friends will be shielding against you, fair weather friends will distance from you. Family will look down upon you. The day you finally succeeded, paying the bills for every get-together dinner, entertainment, you will realised: everyone else is present except strangers.

I don’t blame them. As Walter Bradford Cannon once said fight or flight is a physiological reaction that occurs in response to a perceived harmful event, attack, or threat to survival. A sale may seem like a harmful attack to their wallets (whether or not the product/service is useful for them or not). Any and every exposure to a sale person might seem daunting for some.

I know of some friends who put down everything to start a business. It isn’t as glamorous as it seems. Behind the nice Facebook post lies hard work, sweat and tears (not exaggerating). There are also countless heart aches that they (myself inclusive) have experienced in the course of running a business.

Working well beyond 9am to 5pm. Some quit their jobs and suddenly they are working 24/7

Some might face discouragement from family or their close ones. Some very hurtful sentences include “You have a degree, why do you want to do this?”, “Why don’t you find a proper job?”, “Why are you not setting aside time for the family, is money that important?”, “Why are you not working hard enough (when things are not going well), do you know we have a family to support?”, “I can get this cheaper from Taobao”, “I can do this myself by reading up” etc

Yet, the day you succeeded in the world eyes. Suddenly, the applause comes in. Comments like “I knew you could do it all this time”. I heard this first hand from a friend who successful sold away his business for millions of dollar. However, I would have to say it is not easy. It is hard to suddenly trust someone to buy something straight away. It is even harder to refer them to someone that you know. But for those of you who did, a big thank you.

Do you know someone who is running a business or a practice? Lend them a helping hand. Here are some from I know run great business and I would like to extend to them a helping hand.

Disclaimer: I do not get any referral fees for promoting them. I personally feel that their products and services are great.

#5: Buying Life Insurance cannot change your life; instead it prevents your lifestyle from being changed. After tolling for decades, an illness can wipe out an entire family’s saving by medical bills incurred.

You will not turn bankrupt because of buying insurance but you will cause your loved ones to turn bankrupt if you don’t.

There are certain things we want to happen and certain things we don’t want to happen. In the 21st century, humanity is facing one of the greatest war ever: the war against critical illness. Mortality has improved over the years because of medical innovation. At the very same time, the cost of medical provision has also increase. What seems to be like a death sentence decades ago can now be cured.. but you need money to have access to that treatment.

After chatting with past critical illness survivors, I realised that concern of falling ill runs deeper than just the cost. At the end, affording the treatment is the start. Recovering from the illness is the end game. Give yourself a chance to win this game by having the adequate insurance.

Final Thoughts

Let’s all thrive in our lives, business and relationships.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.