Stock market has been a lackluster as S&P dropped 16.5% since the start of the year. No matter if you are invested into growth stocks or value stocks, it has been a painful year so far.

The cryptocurrency market is now under immerse pressure as stablecoin UST crashed to zero bringing the whole cryptocurrency market with it. People are now reconsidering if cryptocurrency is a true hedge towards traditional equity market.

If you have already forgotten, we still have the Russia-Ukraine conflict, the dealing with post COVID-19 and Johnny Depp-Amber Heard trial ongoing. It is one perfect long storm.

Coming back to wealth management, it always interest me to see what the experts in the field are doing. In this case, one question that fascinates me is what would Warren Buffett do?

What Would Warren Buffett Do?

What would Warren Buffett do?

In 2020, COVID19 brought about a new trend. A trend on investing in high growth companies. Cathie Wood became an instant celebrity with her ARKK fund performing being up 300% from the bottom of March 2020 at one time. Warren Buffett hit the news around the same time. However, it was one where people thought he was losing his magic as his fund was underperforming the ARKK drastically.

As time passes, you can see from the chart above that there was a huge reversal and value investing is now respected again.

Disclaimer: The below discussion will be on the actions of Berkshire Hathaway (BRK) or Warren Buffett. This does not constitute any investment advice.

What is Warren Buffett doing now?

What would Warren Buffett do

Warren Buffett invest with a mindset called value investing. In the very simplest form, it means investing into a wonderful business at a sensible price. The challenge is always to find out what is a wonderful business and what is a sensible price.

In the first quarter of 2022, BRK increase their exposure to Chevron (4th biggest position in BRK). This is a timely position as the world reconsiders to purchase oil from Russia.

Personally, I think Warren Buffett has a good grasp of business flow in the United States. Since Biden took office, one of the things he did was to revoke the permit for the Keystone XL pipeline. I read with great interest but have no idea on the implication. Perhaps, this might be a reason why he started investing into oil.

The investment into ATVI was probably a value buy. In an interview Buffett said “It is my purchases, not the manager, who bought it some months ago. And if the deal goes through we make some money, and if the deal doesn’t go through who knows what happens.” Buffett said his decision came down to the fact that Microsoft’s purchase values Activision Blizzard at $95 per share. Activision Blizzard was trading at $75.60 per share as of the close of markets on Friday. Perhaps, he was buying for a good arbitrage opportunity.

Lastly, it is about investing in yourself. Buffett spend his time investing into himself. He reads at least 80% a day. During times of uncertainty, it’s more important than ever to be as valuable as ever, and as Buffett said, the best thing we can do is “be exceptionally good at something.”

Final Thoughts

What will you do?

Personally, I will be reviewing my own portfolio. I believe this is a good time to add new positions even in this current situation. Valuation has been depressed and perhaps a good time to dollar cost average now.

What will you do?

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

Investing is a like taking a trip to a dream destination that you really want to go. You might feel it is nerve racking as this might be the first time you are going to take a long trip. You might also be unsure what to pack and bring. You might also feel anxious as you don’t know if you prepared enough for the trip.

If you have experience planning for a 10 days (or even longer) holiday, the skillset used there can be transferred over to investing. Here are 5 things to prepare before going on your trip.

Special note: Whether you are starting the journey or have already started, I wish everyone a safe journey.

#1: Determine Your Destination.

Many people stumble on this point right at the start. One of the most interesting conversation I ever had was with a friend in university. I remember him saying that he wants to get “many experiences” travelling. However, when I asked him where he wanted to go or what he wanted to experience, he couldn’t give me an answer. He simply stared at me said “anywhere lah”.

In the end, he didn’t go anywhere at all. He just couldn’t decide.

It is the same for investing, you might want to be a self directed investor because you want to make more money but you might not know how much you need to make. Although “the more the better” is relevant here, the lack of destination creates a tension in your mind because your brain don’t know what to do. In the end, most people don’t start.

Knowing your destination is simply require simple mathematics. I’m going to assume the following.

Assumption:

I want $5,000 monthly or $60,000 yearly for my retirement.

I wish to retire at age 55. Since male mortality is age 83 (female is 88), I would require 28 years of $60,000 or $1,680,000.

In this simple illustration, you would have already determined your destination. It is time to start packing.

#2: Buy A Map / Make Sure You Have Google Maps

If I were to ask you to drive from your house to Tuas Crescent 1, would you be able to do it? Unless you know Tuas very well, it would be very difficult and time consuming. This issue escalates for longer journeys. Imagine, asking someone to drive to Four Season Hotel in Thailand, Bangkok without a map.

For self directed investors, one of the most important thing is to have a map. This map is a strategic game plan that allows you to move from Point A to Point B. It is a map that would show you where are the possible danger spots and route to take.

In investing, we call this a game plan. There are several game plans out there. Each and every of them will eventually get you to your end goal. Some example of game plans are like ETF dollar cost investing, Robo-investing, Value investing, Growth investing, Value-Growth investing, Options investing, Momentum Growth Investing, Multi-Asset Value-Growth investing or trading. These game plans are created by people who have gone ahead of us and are itineraries that we can consider.

You might prefer certain itineraries to others. Some of more “adventurous”, some take the safer route. However, the lack of tour guides means that you have to take ownership of the trip.

You might find yourself stuck at this stage because you don’t know which is the best route to follow. My advice is to try out any path. This is because you will quickly understand which paths fits you the best ONLY IF you step on that path. You can also change your path along the way.

#3: Get Your Passport

A passport allows to travel across countries. For investing, the passport is your brokerage account. It allows to buy and sell. This is the most straight forward step for self directed investors.

You can consider between the brokerage account in the traditional banks or the new brokerage accounts like Moomoo or Tiger.

There may be promotions at different periods. If you have enjoyed reading this article, I would appreciate if you could register an account with my referral above. Appreciate it loads!

#4: Leave The House

I remember leaving my house for my student exchange in Sweden. There was a mixture of excitement, fear, uncertainty and I missed home suddenly. Of course, that trip turned out to be one of the best trips I ever did in my life.

Our house is our “comfort zone” and in the same way, investing into the stock market is usually outside our comfort zone especially if you have never invested before.

The journey of a thousand miles begins with the first step. It is only when you put in real money into investing can your journey truly begin.

Leave The House: One of my favorite photos of Uppsala, Sweden

#5: Keep Track of Your Progress

Nothing is more scary than being lost. One of my first solo trips was to Taiwan. My plane landed in Taipei and I was trying to get to Kaohsiung. In my very silly attempt to save money, I decided on taking the bus to Kaohsiung instead of taking the train.

It took me 8 hours from Taipei to Taichung by bus and I knew something is wrong. My phone battery was going to be flat and I was meeting a friend in 3 hours time. I transferred to the next train to Kaohsiung (in the end, I spent even more money) and landed at Zuoying Station. I happily told my friend that I will be waiting for them at MacDonald. My friend asked me which one? Who knew that there was Zuoying Station and Xin Zuoying Station. My phone battery took one last breath before shutting down.

Luckily~ my friends found me on their first try.

It is the same for investing. Sometimes we do get caught up in the moment and make irrational decisions. It is crucial to acknowledge when you are lost and change directions immediately. It would be easier especially if you have a group of mentors whom are familiar with the workings of the market.

Even if you are on the right direction, take note of your milestones and celebrate them when it comes.

Final Thoughts

Being a self directed investor gives you a lot of control but you have to learn how to control it. It will take both time and effort. Starting is very scary but once you start, I can assure that it will be a well lived life.

Are there any other tools you feel you need to get started? Let me know in the comment below.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

5 Principles To Self Directed Investing: Nope, that’s not my arm.

Self directed investing is an interesting journey. I struggle to write this article as the “interesting” journey was not a fun one at all. The old cliche “there are ups and downs” barely scratch the surface of investing with confidence.

As I get more and more requests to teach investment, I realised I keep repeating certain concepts for people who wants self directed investing. These concepts can be summarized into the 5 key principles. These 5 key principles separates investors from speculators.

This article will be more crucial to those who wants to focus on investing rather than speculating. If you thinking of speculating the market, this article may not be beneficial to you.

Disclaimer: The example shown below are not and should not be used as a buy/sell recommendation.

#1: First Principles

I learnt about First Principles from Elon Musk. This term was coined over 2000 years ago by Greek Philosopher Aristotle. Basically, first principle is a basic assumption that cannot be deducted any further.

One simple question that I ask people is what constitute a good company/instrument to invest in? I’m always met with weird stares and raised eyebrows because the answer is typically the flavour of the month. It used to be Cloud, then Electric Vehicles or ESG investing in the recent years. Metaverse is probably going to be a typical answer in the next few quarters.

While they are not wrong, it says nothing about the companies’ underlying business.

When you do self directed investing, you want to find companies’ whose underlying business have a certain advantage over others (otherwise coined as economic moat). This business have to exhibit certain growth potential in the years ahead. If you can’t find a business with an advantage over others, why invest in this business? If you don’t see a growth potential in this business, why risk your money in this business?

When you break investing into First Principles, it becomes easier to understand. However, it takes time to understand a business and it also take time for the company to grow. Ask yourself, are you spending enough time understanding a business and allowing it to grow?

5 Principles To Self Directed Investing First Principles

#2: Learn The Language Of Money

I remember asking for directions to a famous bakery in France and it didn’t go well. A kind hearted gentlemen (at least I believed he was) asked if I wanted some pain. I will leave it to you to imagine how scared and confused I was. Anyway, pain means bread in French.

5 Principles To Self Directed Investing Language Of Money

You see harmless jokes like these appearing at random times in our lives. We laugh about it because it don’t really impact us that much. However, it is very different when it comes to the language of money. It WILL hurt when we misinterpret this language.

The language of money in investing is basically accounting. Doing self directed investing without learning about accounting is basically suicide. While you don’t need to learn every single word in the dictionary to understand a language, you will need a certain basic level of grammar rules, vocabulary and sentence structure.

This also takes time to understand but it can be learnt quickly especially if you have a trainer or a teacher who can explain to you what the more important jargons are.

#3: The Wait is as important as the investment

5 Principles To Self Directed Investing The Wait

In the era where everything can be obtained in a snap of a finger, the wait is especially difficult. Amazon’s Prime Now, our 4G internet connection, 24/7 island delivery has made things more convenient but has altered our expectation of waiting. We have to relearn how to wait.

“The stock didn’t move much.” (In 2 days)

An extreme example of a company that “didn’t really move much” is Microsoft. Microsoft is now the biggest company (by market capital) in the world right now. However, it went through decades of underperformance until it finally bore fruit for investors. Even if you have invested at the peak of the dotcom bubble until now, you would have average a CAGR of 9%.

5 Principles To Self Directed Investing The Wait MSFT

Thankfully, not all companies are as extreme like this. That being said, we need to relearn how to wait.

#4: The Price To Pay

In business, everything has a certain value or worth to it. I plan to write an article on property prices in Singapore very soon as I note that there are more and more Million Dollar HDB flats in Singapore. Who determines the prices? The buyers? The sellers? The property agents?

The “smart” answer in this case is the market.

Even though the market determines the prices, it does not mean you need to accept those prices. You on the other hand have 3 decisions to make. To buy, to hold or to sell.

The market prices changes every single day which gives an opportunity to buy at a price that you want. Being a self directed investor, it is important to decide what is the price that you are willing to pay for the company. The danger comes when you are overpaying for the company.

5 Principles To Self Directed Investing The Price To Pay

#5: Seek Other Experts

We specialise in certain topics at a very young age of 16 to 21. We go to polytechnic and/or university and are required to take a certain discipline that we will be sticking to for at least 3 years. We then proceed to the workforce and work on that role for a good period of time.

For me, it was finance and economics. While I’m celebrating my decade in the financial institution I’m representing next year, I’m always reminded (especially during COVID-19) that I have little or no knowledge about pharmaceutical companies.

To understand these pharmaceutical companies such as Pfizer and Moderna, I would have to ask experts in those fields if I ever would want to invest in them.

For self directed investors, it is crucial to reach out to other experts (or a community) especially if you want to find out more about those companies. These experts will probably know one or two things more than you do and that would make or break your investment decision.

Final Thoughts

Being a self directed investor gives you a lot of control but you have to learn how to control it. It will take both time and effort. Are you prepared?

Are there any other principles you feel should be included? Let me know in the comment below.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

I have never owned a credit card. Despite credit card companies having great promotions, I felt that it was simply a gimmick to go down the slippery slope. I personally saw how close friends (educated poor) raked up over tens of thousands of debts because of these shiny cards. My Telegram channel where I share one financial tip a day also know I shut this off totally.

So what changed? I want to share a new perspective of what I learnt this year and hope this can somehow change your news on these cards in our wallets.

What is a Credit or Debit Card?

Both credit and debit cards have made it easier and more convenient to do purchases whether it is online of in stores. There is one key difference.

Credit Cards: It allows you to borrow money from the card issuer up to a certain limit to purchase an item or withdraw cash.

Debit Cards: It allows you to draw money that you havedeposited in the bank.

Basically, credit card uses other people’s money and a debit card uses your money.

I want to draw on 3 points for you to consider before you make a decision for yourself.

#1: Responsibility

Do you have spending issues? Trust me, I met people who have and they were the ones who encouraged me to write The Ultimate 4 Quadrants Shopping Guide. They have been using it like a bible since then. I do think it is important to know and accept what kind person we are. It is only with this knowledge and acceptance that can allow us to create a solution for you.

Often, I see people who denies or dismiss their true self makes their debts even worse.

For people who have spending issues, get a Debit Card.

#2: Benefits

If you are well disciplined with your finances, you may explore what benefits Credit Cards have. Some offers cashbacks while others offers miles. Some might give you a luggage or even upfront cash when you sign up! This is quite straight-forward.

It is a hands down win for Credit Card here. The only thing you have to make sure is to pay it all up before your interest comes in.

#3: Security

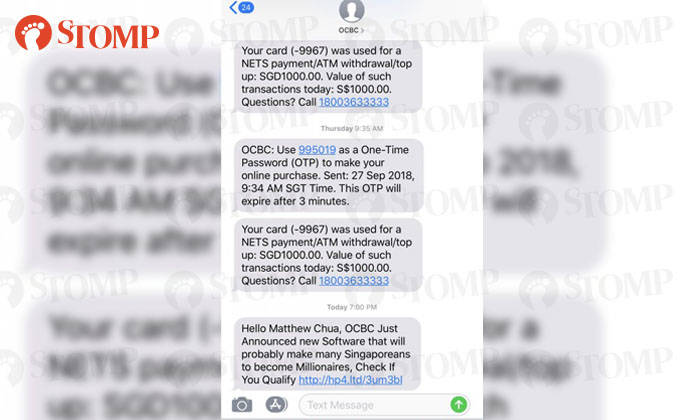

I truly appreciate this a few years ago when I received an SMS from OCBC saying that $3000 has been deducted from my debit card. This message was received when I was in office attending a training and I don’t have any transaction of that size. I logged into to my OCBC account to verify and indeed the amount was deducted. To tell you the truth, I felt nausea when I received the sms.

I have long lost that SMS but I have found something similar from Stomp.

The Great Debate Credit Card Or Debit Cards Security

I immediately dialed for OCBC. For what felt like decades (for those of you who have called the bank before, you would know how long it took), a customer service representative replied. I appreciated the representative was clear and calm. He advised some paperwork, asked me to dispose of my current debit card and arranged a new one to arrive in a few working days.

However, he was hesitant when I asked when I will receive the $3000 back. He mentioned the bank will do the appropriate investigation and will take a few weeks before the amount will be back in my bank again.

Eventually, I did get my $3000 back in my account. It took slightly lesser than 2 weeks. However, I felt worried all the time.

Credit cards on the other hand, serves as a border between your personal money and the transaction. In an event of an identify theft or stolen card, it will be less stressful as it is technically not your money. I never truly appreciated the value of Credit cards until this happened.

Final Thoughts

I have 1 credit card which I used mainly for my transactions. I reap some benefits by getting cashbacks from my transaction and yes, I do make sure I pay on time.

Which will you choose? Credit cards or debit cards? Let me know in the comments below.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

This show from Netflix needs no introduction. Amidst the games, the show highlighted the Korea Economy. One with highly-skewed income disparity, worsening household debt and survival of the fittest amid fierce competition.

While watching the show, I keep feeling that the characters behave very badly when it comes to money (or the lack of money). Just a few days after, I can’t help but think that it is an representation of what is happening in real life. (That’s probably why the show resonates to us on some level).

To avoid going down the slippery slope, I decided to consolidate the lessons we can learn from this so that we will NEVER have a situation like this EVER.

Hope you enjoy the read.

Spoiler Alerts: Please do not read this as it contains spoilers on the show. We invite you to come back after you finish the series.

We Have Emotions

Financial Lessons From The Squid Game Emotion Greed Fear (Source: Distractify)

I feel that this is something that isn’t acknowledged much in the financial world. It is often thought that most financial decision can be made logically easily. The basic assumption in most economic literature is that humans are rational in nature. However, behaviour economics proven time over time that this couldn’t be more wrong.

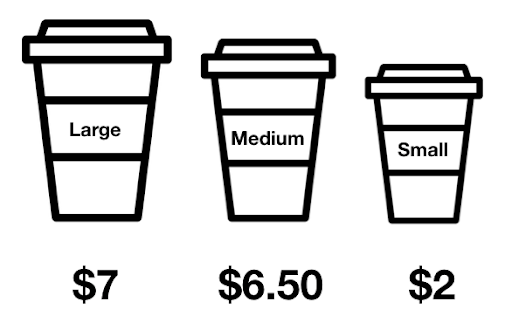

Consider this, you walk into Starbucks (or any other coffee places) to get your daily small dose of coffee. After looking at the prices, most people end up getting the big cup not because they wanted it but because it is a “much better price” than the medium. If you have also chosen the big cup, congratulations, you have experienced the Decoy Effect.

The Decoy Effects explains how an inclusion of an inferior 3rd choice (medium cup) will affect your consideration of between the initial 2 choices (large and small). When there is a decoy alternative, most people makes decision based less on what suits their needs and what we considered as a more beneficial alternative. This results in people spending more as a result at Starbucks.

This is just one of the many cognitive bias that we experience.

These makes it very tough to be rational in a body where we feel so much. Today, most people only focus on the rational side which makes it tough to have a good conversation on finances. I hope that more and more people can come to acknowledgement with their emotions in future.

You Can Win With The Right Strategy

Financial Lessons From The Squid Game Right Strategy

In this very epic game of tug of war, strength is very important. In the team of 10 people, the protagonist team have 3 ladies, 1 weak elderly and 6 men. They faces off a stronger team consisting of all men.

While it feels like the protagonists team have a clear disadvantage in this game, the weak elderly share his wisdom and experience on how to strategize and win against teams that are bigger and stronger than them.

The protagonists team barely escape death by execute the strategy and winning against a team far stronger than them.

In the financial world, you can consider the 10 people the resources that we have. Some of my peers have rich parents, some are left properties under their names, some have good networks and have parents financially independent. But, they may not be financially as well off.

I also have friends who have siblings who depend on them, a study loan, parents who believes that children is the ultimate retirement plan. In spite of this, some of them do succeed in their financial goals by having a right strategy and executing it well.

Having a strong 10 people/resource is important. It is as important as having the right strategy and executing it well.

Learn From Others Mistakes

Financial Lessons From The Squid Game Learning From Mistakes

In another nerve wreaking game called the glass stepping game, participants are made to cross a glass bridge. Participants are presented 2 choices. Stepping on the right choice would mean safety, stepping on the wrong one would meant death. In any event the participant chooses the wrong one and dies, the one after him/her can choose the right one and proceed with the game.

In this game, it is awful being the first one.

In the financial world, money was first originated some where as early as 5000 B.C., in which tons of literature has already been written. One of the classics of financial books is The Richest Man in Babylon. Many important clues have been record and it is up to us to follow that roadmap presented to us.

Another way is to learn from the people around us. If our parents have achieve a certain level of financial freedom, we can learn from it. If our parents have not achieve any, we can also learn from that too.

In whichever case, there is always something to learn.

People Can Behave Badly When It Comes To Money

Financial Lessons From The Squid Game Bad Behaviour

In the final game of the series, Squid game, the 2 protagonists face off in a brutal, savage and barbaric fight. As their lives and the prize money was on the line, they really had a lot to fight for.

I was reminded of estate planning stories and divorce stories that were shared during my recent IBF Certification for Private Banking. Most of the stories were very unfortunate. In almost all cases, humans behaves very badly when it comes to money issues.

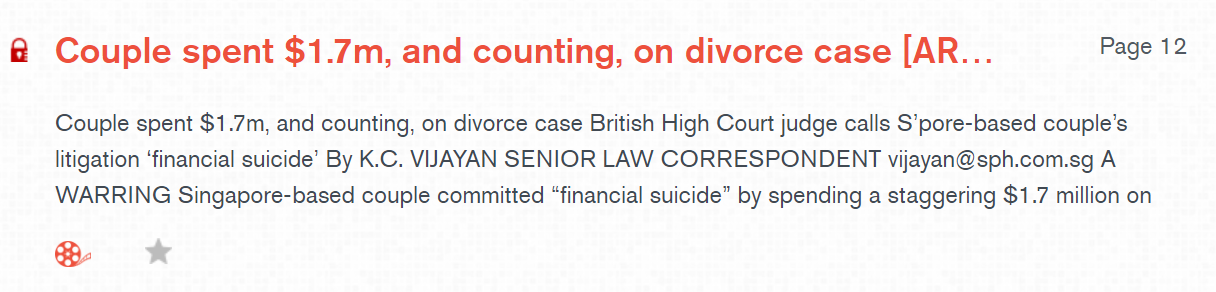

A old example happened in 2013 when a Singapore based couple committed “financial suicide”. Both have spend SGD$1.7 million on legal costs – just to decide where the divorce should be heard as well as litigation costs linked to the child. You can find the article from multimedia stations from NLB Libraries. It is written in The Straits Times dated Friday, 2 Aug 2013 by Senior Law Correspondent K.C. Vijayan.

Divorce Case Financial Suicide

In a more recent example, siblings are suing their elder brother over 2 properties worth SGD$3.1 million. As the estate planning was not poorly set up, it has resulted in a messy inheritance battle of which relationship will be ruined. Though it is not known what the legal costs are, I believe their relationship will never be the same again.

The Financial Journey

Financial Lessons From The Squid Game The Journey

In the most iconic game called Green Light, Red Light, participants win by making their way towards the end of the line in a given time limit. They can only move when it is Green Light (when the doll is not facing them) and they have to stop any movement during Red Light (when the doll is facing them).

At the start, the participants don’t really understand what to do. 2 brave souls started the journey but ended up dead. This causes panic to everyone and people scrambled towards the “exit”. Unfortunately, they were all shot dead.

The cooler headed participants began their journey again. Unfortunately, some tripped either because they were moving too fast or just unlucky to bump into themselves. They died in their attempt to reach the end.

As some participants crossed the line and won the game, there were others that couldn’t cross the line and died as well.

In this game, it closely symbolizes our journey with money. In a given period of time (working years), we want to reach the end (retirement). Some people panic when they see others lost money in the investment and ran towards the exit (panic selling). Some people overleverage (move too fast), some people suffers from critical illness (bump into themselves), some people start too late (couldn’t reach the end). In all these cases, it resulted in people having a less than ideal lifestyle.

Final Thoughts

Overall, this show was a dark, ghastful and yet awfully realistic in showcasing the behaviour of humans put in those desperate situations.

I recommend watching a comedy after the show.

What other financial lessons have you learn from this show? Let me know in the comments below.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.