If you have been following my Facebook page, Wealthdojo and Pete Tan has came together to do a podcast on making good decisions. It is really my privilege to sit along side one of the best investors I have known to do a podcast together. Hopefully, by doing a podcast and chatting with him, you can all learn something from us.

Check out Episode 6: Our Best Ways to Manage Spending.

If you read until here, thank you again for your patience and your support over in 2019. I hope that in 2020, Wealthdojo can continue to value add you. Let us know what you think in the comments below. This is a working article. The above doesn’t represent my stock recommendation in anyway. Please read our disclaimer for more information.

I hope to nurture genuine relationships with all of my readers. Please feel free to contact me on my Instagram (@chengkokoh) or Facebook Page or my Telegram Channel!

Every year, Peter started out full of fire. Peter want to achieve new goals. He set a goal of wanting to learn how to invest so that he can stop worrying about money. He also says improve his public speaking skills so that he want present better and hopefully he can get a promotion. This year round, he also want to be fitter and achieve gold in his IPPT.

In January, he started to read from Seedly, plan his monthly budgeting and also emailed a few banks to ask the procedures to open up a brokerage account. He also visited a few toastmasters club to see whether he can be a good fit in there. He also signed on a gym package from Fitness First and plan to exercise at least 3 times a week.

6 months later. Peter just completed his work at 9pm. He is tired. He looked at his mobile phone to book a grab so that he can go home. He looked at his calendar and realised he have a presentation deck that he need to create for his boss by tomorrow. He ordered Macdonalds and thought what time he can sleep tonight.

In December, Peter met some friends whom he hasn’t met in a long time. Everyone was excited as it is the Christmas season. They were talking about their upcoming travel plans. In almost a complete agreement, everyone seemed to agree that this year seemed to pass very quickly.

In the next year, Peter remembered his goals again and decided that this year it will be different.

Reflection 2019 Not again

This is probably not new. For most people, this repeats every year. I know that it is hard when we are in the daily grind. Our companies have expectations for us. Our family have expectations for us. Even our friends have expectations for us. It is easy to be lost in the daily grind. Just ask Peter, Peter (Alias name of course) is a friend who graduated for 7 years from a local university. He is employed and works hard in his job. He is working beyond his stated hours and job scope to get more experience as his manager feels that it will help in his appraisal. After 5 years, his manager told him that he is a good worker but they will not be able to promote him as the economy is not doing well. He is now 30, carries a eye bags, tired and has high blood pressure and cholesterol.

Years seems to pass in a blink of an eye.

Can you remember what happened at the beginning of the year?

I strongly believe that to move forward (properly), you have to reflect on what happened in the year before. It could hold valuable lessons from mistakes we made. It could hold achievements that you are proud of. It could also hold things that we could learn from. This year, I decided to write this post to share with everyone the lessons I learn from creating Wealthdojo in 2019. I hope that some might resonate with you, maybe some might take inspiration from it and maybe it could be a good read for the end of 2019.

Reflection 2019 Mulan

1) Authenticity

This is a huge one for me in 2019. 2019 is the year I started Wealthdojo. It started of as a simple blog to talk about finances in Singapore. In the span of the year, many people came to me with “tips” to increase the traffic into the blog. As a result, I was writing articles that were Search Engine Friendly but not Human Friendly. I thought that by increasing traffic into the blog, I could get more readers. Boy, was I so wrong.

I began to realised that by doing so, I was losing connection with my audience. I started to receive feedback that my blog was like many others and was not adding value to my readings. (I sincerely apologised if you have been following this blog and have read those articles). In future, I will continue to share more about my financial journey and input my thoughts and opinions for this blog.

Thank you again for those that have been reading my articles.

2) Your Money Capacity

“I have $20 million dollars. What can I do with it?”

I was asked this question a while back. I went back to think for a while and gave my suggestion to the individual that asked me about it. In a nutshell, I was only able to use $2 million dollars of it. I was explaining how I was able to use just $2 million to help him achieve what he needs.

“You only have a money capacity of $2 million.” said that individual.

“Because you only have a $2 million mindset, you can only address a $2 million problem. What will you do if you have the other $18 million?”. He continued.

In my heart, I agreed with him. I have no idea how to use the other $18 million.

I have already experienced this twice in my life. That was when my investment portfolio went from a 4 digits to 5 digits portfolio and when it went from a 5 digits to a 6 digits portfolio. You might think it is just a change in number. However, many of us are unable to handle this change emotionally.

Looking back, when my portfolio increase to 5 or 6 digits, I realised my emotions changed from cautious to adventurous in a span of a few days. As I was investing in the stock market, there are variation in share price everyday which cause my portfolio to increase to decrease a lot. Think about a 2% variation every day when you have a 5 digit portfolio VS a 6 digit portfolio

Situation A:

Investment Portfolio: $10,000. 2% is $200 potential change every day.

(In our mind, we think that we have earn/lost $200. For most people, $200 is a acceptable number to earn/lost because we link it to perhaps a meal at Hai Di Lao. We are able to stomach this variation)

Situation B:

Investment Portfolio: $100,000. 2% is $2000 potential change every day.

(In our mind, we think that we have earn/lost $2000. For most people, that might be half of their income a month. Some would not be able to stomach this variation emotionally which lead them to self sabotage themselves by making irrational decision in the stock market)

Look no further, I experienced this not once, but twice. It was only after taking time to process the emotions and better understand myself that can manage this portfolio effectively. My money capacity is now been widen to a 6 digit portfolio size and potentially a $2 million capacity. Eventually, the time will come when I manage a 7 or 8 digits portfolio.

Situation C:

Investment Portfolio: $10,000,000. 2% is $200,000 potential change every day.

I’m still in the journey of learning how to manage this in my mind. How big is your money capacity?

PS: This isn’t the same as mind face.

Reflection 2019 Money Mind: How much can you hold in your mind?

3) Partnership

Throughout the year, I have been asked to see if I can work together with another company or an individual. They came to me to seek for a win-win-win situation and to value add each other’s community so that everyone can grow together. This is usually how the conversation grows.

Potential Partner X: “I noticed that you have this Wealthdojo. Could you help me set out some time for me so that I can speak about xxx to your participants so that I can value add them in xxx”

Me: “That sounds good. I would love to allow you to value add my community. I also noticed that you have your community. Is it okay if you also help me do the same and I would love to value add them by sharing with them my knowledge about personal finance”

Potential Partner X: “Oh. But there might be conflict of interest… Talking about personal finance is very sensitive… People might not like it… etc”

Me: “If you think there is a conflict of interest, why do you want to come to my seminar to speak about your xxx? Is there a conflict of interest?”

Potential Partner X: “…”

I’m always curious why there is a conflict of interest to share at their community but no conflict of interest to share at mine.

After talking to a few business owners, I realised it is very common in the business world. In the past, I tried to forge partnerships because I believe it was easier to do things in a team. I thought that having a team means that everyone could tap on each other’s expertise and we could do more. That naive thinking cause me several failed partnerships. A unsuitable partner actually destroyed the very culture that I was trying to create.

Over the years, I’ve learn to discern potential partners from opportunist. I’ve learn to select only those people who are genuine to have a win-win-win situation so that everyone can win together. If you are interested to work with me, kindly contact me and let’s see if we can have a win-win-win situation.

How about you? Who are you working with in your life?

Reflection 2019 Partnership

Bonus: Be Mentally Free

*Ding dong*: You have a new notification.

We talked plenty about being Financial Free and the benefits of being Financially Free in Wealthdojo (Duh). However, I feel that there is a part of life not commonly addressed and that is being mentally free.

*Ringgggggg*: Your alarm clock rings. You wake up to snooze the alarm before going back to sleep again. After the 3rd or 4th ring, you finally get up to wash up. While preparing your cup of coffee, you look at you surf Facebook and noticed that Jane is being proposed in Paris. You then receive a notification from Lazada about the latest gadgets having offers (while stock last!). You also receive a whatsapp reminder from your colleague to prepare for the presentation later.

On the way to work, you began to clear emails that you get from shoppe, starbucks and scoot.

You finally arrived in office and sat down to prepare for the day. You noticed 10 emails in your inbox marked as URGENT , giving a soft sigh you worked on those emails and you noticed that your candy crush notification reminds you to log in for the day. You struggle through your meeting while looking at your friends in group chats chat about the latest McBurger offer.

By the time, you finished work. You take the train home only to see that you have several email from jetstar and ezbuy telling you what great deals they is today.

You wonder why you are tired.

Reflection 2019 Mentally Free: Have you thought about what you do to your own mind?

I call this the mental drain. In develop countries, we are exposed constantly to new stimulants such as incoming messages or email. Every notification that you received takes up a certain bandwidth in our mind. Like money, we only have a finite amount of mental bandwidth. Once we finish it, we will feel tired.

Take an example of an email from a newsletter you subscribed years ago. Your phone lit up showing the notification from xxx. You look at it. Press into the app. Ponder for a while and press delete. That may take 5 seconds. By making the decision to delete or not, you have started to accumulate mental fatigue. It is no wonder why we feel tired all the time.

This was my personal experience. It was only much later that I realised I was spending so much time on my phone that I decided to do a mental detox. I wrote down everything that was taking my time away and was not productive. As a result, I unsubscribed to not important email newsletters, off my sound and vibration notification for messages and delete the games in my phone.

At first, it felt weird as there was nothing. Nothing for me to do at any one point. I soon realised that was the freedom that I have sought. I was then able to complete more task (in a shorter time), focus more and still remain mentally free.

How about you? Are you mentally free too?

Conclusion

To conclude, it has been a year full of mistakes, lessons and not forgetting fun. I hope you learnt something from my mistakes, lessons and also fun. Hope you have the same too!

If you read until here, thank you again for your patience and your support over in 2019. I hope that in 2020, Wealthdojo can continue to value add you. Let us know what you think in the comments below.

I hope to nurture genuine relationships with all of my readers. Please feel free to contact me on my Instagram (@chengkokoh) or Facebook Page!

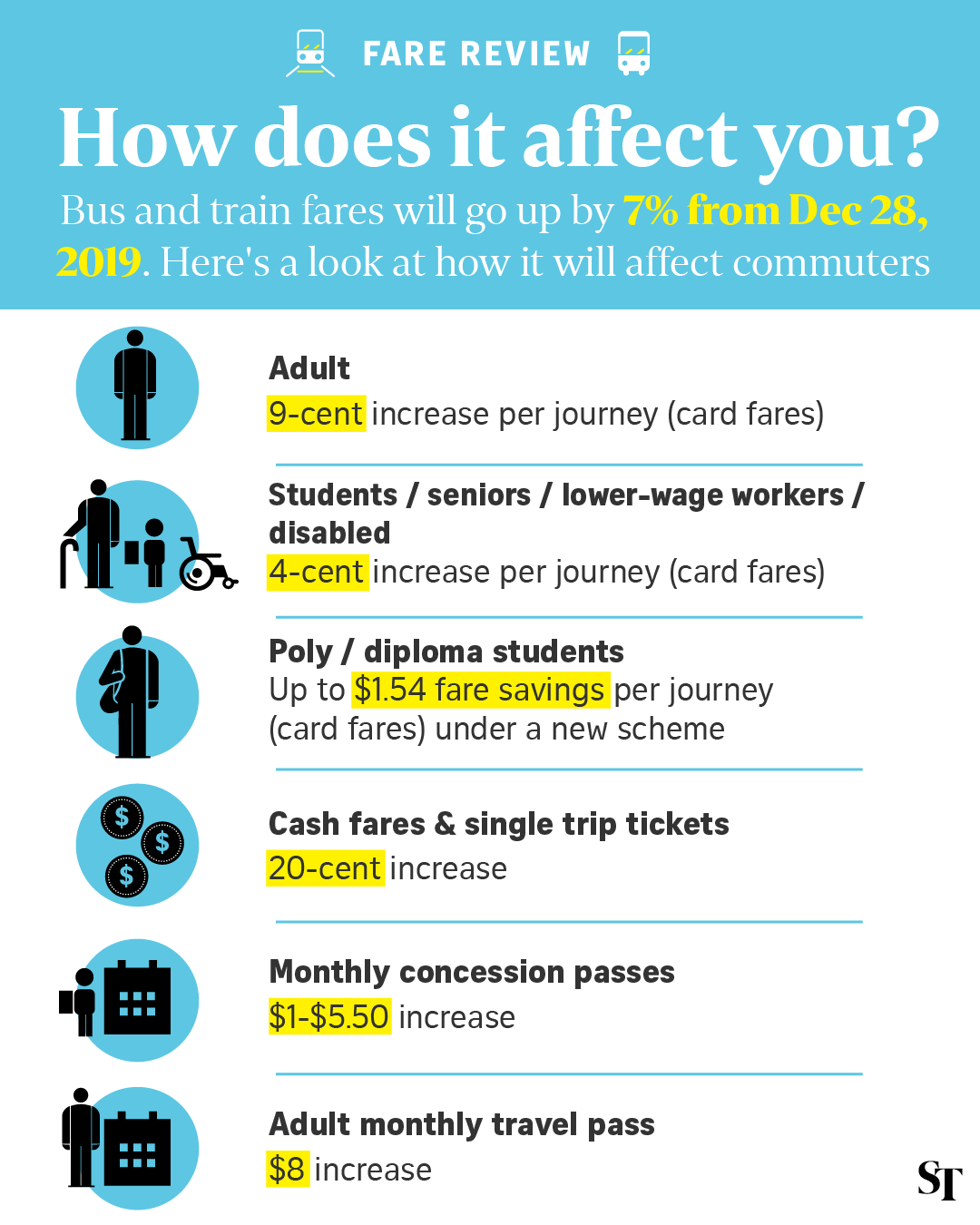

Price hikes for public transportation in Singapore is set to increase. This will include the buses and trains fares that majority of Singapore takes every day to work or school. The public transport counsel has hinted the fares could go up by 7% after they have conducted their fare review exercise. (Read More: Fare Exercise Review)

The reasons cited for the rates increase has been put on the increase in energy prices, rail reliability and also introduction of new buses and MRT over the last few years. This isn’t a shock to me at least. Over the years, fare price hikes has been slowly increasing. (Read more: Public Transport Counsel Chronology). As a nation progress, there will be need for a more reliable public transportation and this will result in higher cost of maintenance over time.

Price Hikes Public Transportation Singapore: Source: Straits Times

For majority of us, the amount of money we spend on public transportation will soon increase in December 2019. We can either lament all we want about the $0.09 increase per journey or we always do something about it. (Read More: Sandwich Generation: Is it still possible to be rich?)

We have created a system to help an individual save up to 5% a year on transportation cost. This comes in timely as it can “cancel out” the effect of increase just by following this system.

Price Hikes Public Transportation Singapore Budget

If you can’t beat them, join them

I’m always excited about companies that are able to increase their prices even during a recession. While we are somewhat in a economy that is slowing down, there are a few companies that are STILL ABLE to raise prices and people have no choice but to pay for it! This is what we called Pricing Power. Investing in companies with pricing power are the ones that can survive and thrive. As Wealthdojo believes in dealing with real life situations, please refer to our disclaimer section for more information.

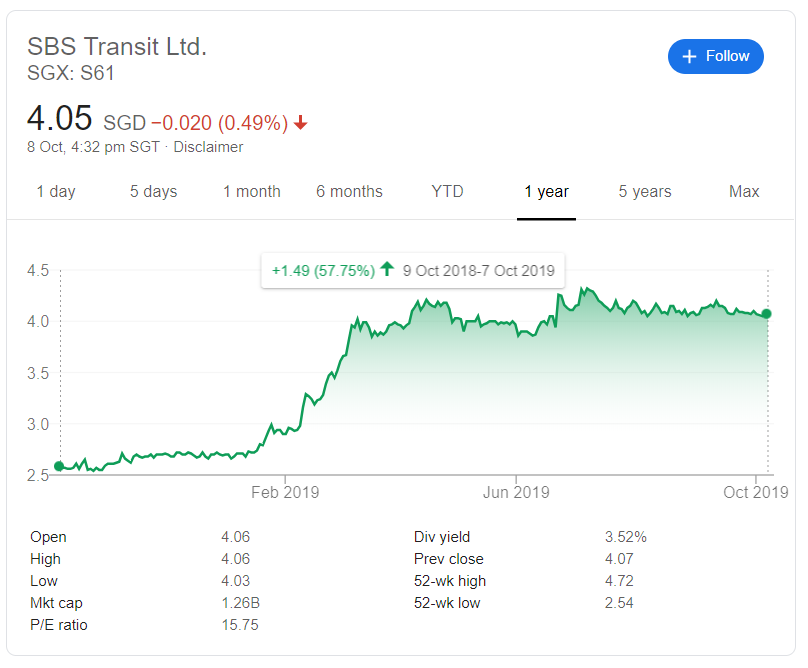

Everyone in Singapore probably knows of this company called SBS Transit (SGX: S61)

SBS Transit Stock Price ComfortDelGro

Basically, they are our train and bus providers in Singapore. Over the last 1 year, this humble share has increase 57%. I have talked about in our Facebook Closed Group (Contact Us to be invited to the Facebook Group). It is a simple business, easy to understand and has a certain pricing power in Singapore. Just to point out an illustration, will you walk all the way to Changi Airport by foot just because your bus fare has increase by $0.09? 99.99% will definitely continue using this service.

In addition to the 57% increase this year, the dividend yield is at 3.52% right now. While it isn’t the highest yielding dividend stock out there, this is clear about our inflation rate this year.

I recommend everyone to study more into this stock before making a decision. This is not a buy/sell recommendation.

We wish you the best in your financial journey.

In Wealthdojo, we believe in bespoke financial planning. Whether it is money maximization, insurance or investing, we believe that everyone is different and the planning should be suited for you.

All opinions above are my own. Please view our disclaimer page to understand more.

I hope to nurture genuine relationships with all of my readers. Please feel free to contact me on my Instagram (@chengkokoh) or Facebook Page!

Now that you’ve read about learnt about how to benefit from What you can do about price hikes for public transport in Singapore. I challenge you to read this article (Things To Consider Before Investing In Foreign Dividend Stocks )to push your understanding further!

Transportation in Singapore is one of the most convenient in the world. We can just tap and go using our Ez-Link card and we can have access to most of the public transportation in Singapore.

Typically, a working adult in Singapore clocks in 2 to 4 trips a single day. This works out to be roughly 60 to 120 trips a month on a public transportation in Singapore.

Save Money on Transportation Singapore

Assuming one trip cost in about $1.50, we spend on average around $90 to $180 a month on public transportation in Singapore.

While this is not a major expenditure, what if there is a way to actually save money on public transportation in Singapore?

Yes. There are actually many ways.

In Wealthdojo, we like to keep things simple especially for money management. We believe that execution > complexity.

We will like to recommend 2 ways to save money on public transportation in Singapore

Tip 1: Get an adult concession card

If you are spending more than $120 a month, this will be an obvious choice to you. (Read more: Adult Monthly Travel Card)

Adult Concession Card Singapore

The Adult Monthly Travel Card (AMTC) is a concession card for adults who travels on public transportation a lot in Singapore. I strongly recommend Sales Representatives (i.e. Insurance Consultants, Property Advisers) to really consider this. It is priced at $120, and it allows for unlimited travel on Singapore’s basic bus services and rail services within the validity period.

For those of you spending less than $120/month on public transportation, great news. In April 2019, we can finally use our credit cards for public transportation in Singapore. Good bye EZ-Link cards. This feature is called SimplyGo (Read More: SimplyGo).

From what we observe there are a couple of benefits for this.

Reduce the number of cards in our wallet

We no longer need to waste time topping up our EZ-Link cards

Receive cashbacks or miles from our credit card.

How does SimplyGo works?

SimplyGo Save Money Public Transportation Singapore

There you go. As simple as that. With just a simple switch, you will be able to open yourself up to a world of benefit in credit card expenditure.

Match it up with credit card rebates

There are 2 camps for this. The cashback camp and the air-miles camp. Whichever you are on, select the credit card that best fits your lifestyle.

I estimate that a typical person will save around $50 a year on public transportation. This number don’t really seem much. However, the effort is minimal here to save this amount of money. (Why not?). I have shortlisted a few cards that my wealthdojo readers who have been trained in the Money Maximization: REV to consider.

DBS Visa Debit Card (3% Cashback. $400 minimum spending.)

For those who are new Wealthdojo readers, these cards are also pretty decent.

HSBC Advance Card (1.5% Cashback. No minimum spending)

Standard Chartered Unlimited Card (1.5% Cashback. No minimum spending)

DBS Black Visa Card ($1 = 1.2 miles)

Credit Cards Save Money on Transportation Singapore

Bonus Tip*: Double your benefits using Samsung/Apple Pay

Reduce your number of cards in your wallet further by now using an electronic wallet such as Samsung pay or Apply Pay. Both of them have their own reward system on top of the credit card rebates you will be having.

All the best in your Financial Planning.

In Wealthdojo, we believe in bespoke financial planning. Whether it is money maximization, insurance or investing, we believe that everyone is different and the planning should be suited for you.

All opinions above are my own. Please view our disclaimer page to understand more.

I hope to nurture genuine relationships with all of my readers. Please feel free to contact me on my Instagram (@chengkokoh) or Facebook Page!

Now that you’ve read about learnt about how to benefit from Save Money on Transportation I challenge you to read this article (How to Benefit from the Enhanced CPF Housing Grant )to push your understanding further!

Life Insurers in Singapore are making the shift in the definition of critical illness next year (Aug 26, 2020). Life Insurance Association Singapore (LIA Singapore) said claims assessment and benefits will follow the definitions, and the terms and conditions stated in their existing policy contracts.

Life Insurers to change definition of Critical Illness

What does all these means?

In Singapore, the definition of Critical Illness have been standardized so that there will be no dispute on why an insurer is able to claim for a Critical Illness and another insurer is unable. The last time the definition of Critical Illness have been updated was in 2014.

If you have bought your Life Insurance with the Critical Illness rider from 2014 until now, you can view the definition of the Critical Illness here (Critical Illness Definitions 2014). Your policy will continue to follow this current definition.

Moving forward, new policies will follow the new definition if you buy your policy after Aug 26, 2020.

How will you be affected?

As mention above, if you buy your life insurance with the critical illness rider before Aug 26, 2020, your policy definition will follow the critical illness definition for Version 2014.

New policies after Aug 26, 2020 will follow the new definition.

For policies from now until Aug 26, 2020 the insurer can adopt either Version 2014 or Version 2019 (Critical Illness Definitions 2019) definitions. If the insurer chooses Version 2014, the CI product must be withdrawn by 26 August 2020.

Why was this done?

The objective of the review exercise was to bring LIA’s 2014 common definitions up to date and aligned with advances made in medical technology and medical practice and also to address areas of ambiguity based on insights gained from the past five years of experience.

The definitions of 21 CIs were revised whilst 16 definitions remained unchanged. The names of 14 CIs were enhanced to better reflect the intent of coverage.

This is very subjective and you will not be able to find an absolute answer. Insurers or the LIA will not commit to this answer. Instead of asking this question, perhaps a better question will be whether you are well-insured or not.

A working adult in Singapore has critical illness cover of just $60,000, well under the LIA recommendation of about $316,000 which translates to about 3.9 times the average annual pay of $81,663. These are just ball park figures give a guide on what you should have.

In Wealthdojo, we believe in bespoke financial planning. Whether it is money maximization, insurance or investing, we believe that everyone is different and the planning should be suited for you.

All opinions above are my own. Please view our disclaimer page to understand more.

I hope to nurture genuine relationships with all of my readers. Please feel free to contact me on my Instagram (@chengkokoh) or Facebook Page! Now that you’ve read about learnt about Life Insurers to change definition of Critical Illness, I challenge you to read this article (National Day Rally 2019: Retirement Impact) to push your understanding further!

Don't miss your learning opportunity. Subscribe to us.