I have never owned a credit card. Despite credit card companies having great promotions, I felt that it was simply a gimmick to go down the slippery slope. I personally saw how close friends (educated poor) raked up over tens of thousands of debts because of these shiny cards. My Telegram channel where I share one financial tip a day also know I shut this off totally.

So what changed? I want to share a new perspective of what I learnt this year and hope this can somehow change your news on these cards in our wallets.

What is a Credit or Debit Card?

Both credit and debit cards have made it easier and more convenient to do purchases whether it is online of in stores. There is one key difference.

Credit Cards: It allows you to borrow money from the card issuer up to a certain limit to purchase an item or withdraw cash.

Debit Cards: It allows you to draw money that you havedeposited in the bank.

Basically, credit card uses other people’s money and a debit card uses your money.

I want to draw on 3 points for you to consider before you make a decision for yourself.

#1: Responsibility

Do you have spending issues? Trust me, I met people who have and they were the ones who encouraged me to write The Ultimate 4 Quadrants Shopping Guide. They have been using it like a bible since then. I do think it is important to know and accept what kind person we are. It is only with this knowledge and acceptance that can allow us to create a solution for you.

Often, I see people who denies or dismiss their true self makes their debts even worse.

For people who have spending issues, get a Debit Card.

#2: Benefits

If you are well disciplined with your finances, you may explore what benefits Credit Cards have. Some offers cashbacks while others offers miles. Some might give you a luggage or even upfront cash when you sign up! This is quite straight-forward.

It is a hands down win for Credit Card here. The only thing you have to make sure is to pay it all up before your interest comes in.

#3: Security

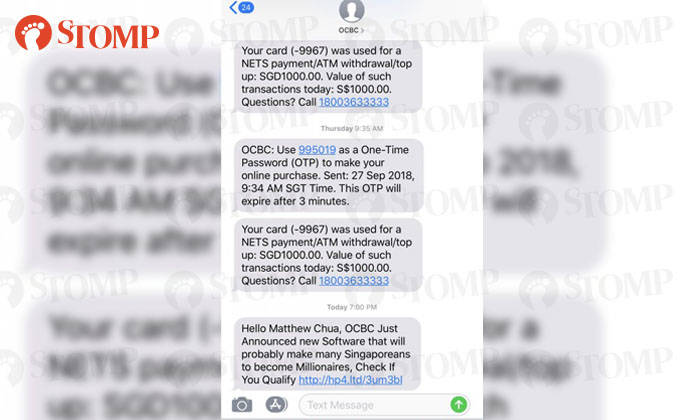

I truly appreciate this a few years ago when I received an SMS from OCBC saying that $3000 has been deducted from my debit card. This message was received when I was in office attending a training and I don’t have any transaction of that size. I logged into to my OCBC account to verify and indeed the amount was deducted. To tell you the truth, I felt nausea when I received the sms.

I have long lost that SMS but I have found something similar from Stomp.

The Great Debate Credit Card Or Debit Cards Security

I immediately dialed for OCBC. For what felt like decades (for those of you who have called the bank before, you would know how long it took), a customer service representative replied. I appreciated the representative was clear and calm. He advised some paperwork, asked me to dispose of my current debit card and arranged a new one to arrive in a few working days.

However, he was hesitant when I asked when I will receive the $3000 back. He mentioned the bank will do the appropriate investigation and will take a few weeks before the amount will be back in my bank again.

Eventually, I did get my $3000 back in my account. It took slightly lesser than 2 weeks. However, I felt worried all the time.

Credit cards on the other hand, serves as a border between your personal money and the transaction. In an event of an identify theft or stolen card, it will be less stressful as it is technically not your money. I never truly appreciated the value of Credit cards until this happened.

Final Thoughts

I have 1 credit card which I used mainly for my transactions. I reap some benefits by getting cashbacks from my transaction and yes, I do make sure I pay on time.

Which will you choose? Credit cards or debit cards? Let me know in the comments below.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

This show from Netflix needs no introduction. Amidst the games, the show highlighted the Korea Economy. One with highly-skewed income disparity, worsening household debt and survival of the fittest amid fierce competition.

While watching the show, I keep feeling that the characters behave very badly when it comes to money (or the lack of money). Just a few days after, I can’t help but think that it is an representation of what is happening in real life. (That’s probably why the show resonates to us on some level).

To avoid going down the slippery slope, I decided to consolidate the lessons we can learn from this so that we will NEVER have a situation like this EVER.

Hope you enjoy the read.

Spoiler Alerts: Please do not read this as it contains spoilers on the show. We invite you to come back after you finish the series.

We Have Emotions

Financial Lessons From The Squid Game Emotion Greed Fear (Source: Distractify)

I feel that this is something that isn’t acknowledged much in the financial world. It is often thought that most financial decision can be made logically easily. The basic assumption in most economic literature is that humans are rational in nature. However, behaviour economics proven time over time that this couldn’t be more wrong.

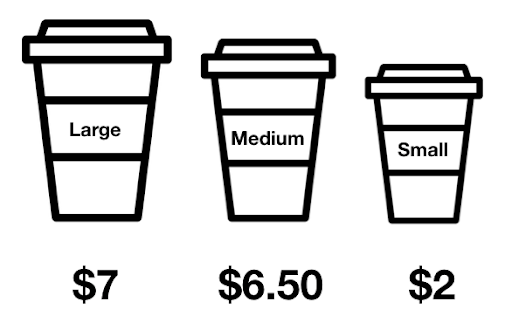

Consider this, you walk into Starbucks (or any other coffee places) to get your daily small dose of coffee. After looking at the prices, most people end up getting the big cup not because they wanted it but because it is a “much better price” than the medium. If you have also chosen the big cup, congratulations, you have experienced the Decoy Effect.

The Decoy Effects explains how an inclusion of an inferior 3rd choice (medium cup) will affect your consideration of between the initial 2 choices (large and small). When there is a decoy alternative, most people makes decision based less on what suits their needs and what we considered as a more beneficial alternative. This results in people spending more as a result at Starbucks.

This is just one of the many cognitive bias that we experience.

These makes it very tough to be rational in a body where we feel so much. Today, most people only focus on the rational side which makes it tough to have a good conversation on finances. I hope that more and more people can come to acknowledgement with their emotions in future.

You Can Win With The Right Strategy

Financial Lessons From The Squid Game Right Strategy

In this very epic game of tug of war, strength is very important. In the team of 10 people, the protagonist team have 3 ladies, 1 weak elderly and 6 men. They faces off a stronger team consisting of all men.

While it feels like the protagonists team have a clear disadvantage in this game, the weak elderly share his wisdom and experience on how to strategize and win against teams that are bigger and stronger than them.

The protagonists team barely escape death by execute the strategy and winning against a team far stronger than them.

In the financial world, you can consider the 10 people the resources that we have. Some of my peers have rich parents, some are left properties under their names, some have good networks and have parents financially independent. But, they may not be financially as well off.

I also have friends who have siblings who depend on them, a study loan, parents who believes that children is the ultimate retirement plan. In spite of this, some of them do succeed in their financial goals by having a right strategy and executing it well.

Having a strong 10 people/resource is important. It is as important as having the right strategy and executing it well.

Learn From Others Mistakes

Financial Lessons From The Squid Game Learning From Mistakes

In another nerve wreaking game called the glass stepping game, participants are made to cross a glass bridge. Participants are presented 2 choices. Stepping on the right choice would mean safety, stepping on the wrong one would meant death. In any event the participant chooses the wrong one and dies, the one after him/her can choose the right one and proceed with the game.

In this game, it is awful being the first one.

In the financial world, money was first originated some where as early as 5000 B.C., in which tons of literature has already been written. One of the classics of financial books is The Richest Man in Babylon. Many important clues have been record and it is up to us to follow that roadmap presented to us.

Another way is to learn from the people around us. If our parents have achieve a certain level of financial freedom, we can learn from it. If our parents have not achieve any, we can also learn from that too.

In whichever case, there is always something to learn.

People Can Behave Badly When It Comes To Money

Financial Lessons From The Squid Game Bad Behaviour

In the final game of the series, Squid game, the 2 protagonists face off in a brutal, savage and barbaric fight. As their lives and the prize money was on the line, they really had a lot to fight for.

I was reminded of estate planning stories and divorce stories that were shared during my recent IBF Certification for Private Banking. Most of the stories were very unfortunate. In almost all cases, humans behaves very badly when it comes to money issues.

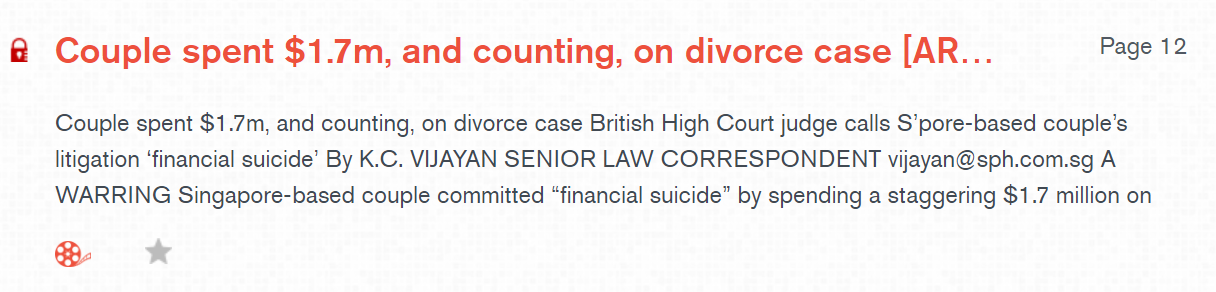

A old example happened in 2013 when a Singapore based couple committed “financial suicide”. Both have spend SGD$1.7 million on legal costs – just to decide where the divorce should be heard as well as litigation costs linked to the child. You can find the article from multimedia stations from NLB Libraries. It is written in The Straits Times dated Friday, 2 Aug 2013 by Senior Law Correspondent K.C. Vijayan.

Divorce Case Financial Suicide

In a more recent example, siblings are suing their elder brother over 2 properties worth SGD$3.1 million. As the estate planning was not poorly set up, it has resulted in a messy inheritance battle of which relationship will be ruined. Though it is not known what the legal costs are, I believe their relationship will never be the same again.

The Financial Journey

Financial Lessons From The Squid Game The Journey

In the most iconic game called Green Light, Red Light, participants win by making their way towards the end of the line in a given time limit. They can only move when it is Green Light (when the doll is not facing them) and they have to stop any movement during Red Light (when the doll is facing them).

At the start, the participants don’t really understand what to do. 2 brave souls started the journey but ended up dead. This causes panic to everyone and people scrambled towards the “exit”. Unfortunately, they were all shot dead.

The cooler headed participants began their journey again. Unfortunately, some tripped either because they were moving too fast or just unlucky to bump into themselves. They died in their attempt to reach the end.

As some participants crossed the line and won the game, there were others that couldn’t cross the line and died as well.

In this game, it closely symbolizes our journey with money. In a given period of time (working years), we want to reach the end (retirement). Some people panic when they see others lost money in the investment and ran towards the exit (panic selling). Some people overleverage (move too fast), some people suffers from critical illness (bump into themselves), some people start too late (couldn’t reach the end). In all these cases, it resulted in people having a less than ideal lifestyle.

Final Thoughts

Overall, this show was a dark, ghastful and yet awfully realistic in showcasing the behaviour of humans put in those desperate situations.

I recommend watching a comedy after the show.

What other financial lessons have you learn from this show? Let me know in the comments below.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

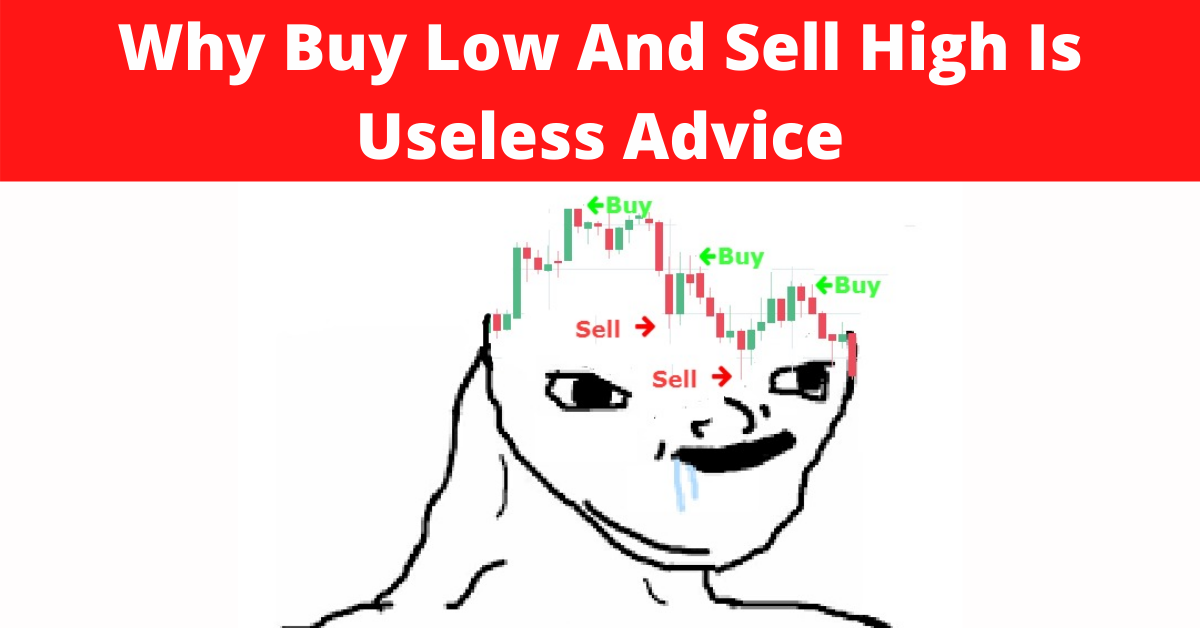

Today, the article focus mostly on the strategy buy low, sell high and why it is useless.

Why Buy Low And Sell High Is Useless Advice

What is Buy Low and Sell High?

The intention for investment is very simple. It is to make money (repeat this in your mind). When you make an investment, you must have every intention for your investment to grow in value in future. Take an example of Facebook (FB). In 18 May 2012, the share price of FB was $38. When you invest into FB at that time, you would have strongly believe it would grow. Today, 9 July 2021, the share price is $350. You would have made 816% by “buying low and selling high”.

Why Buy Low And Sell High Is Useless Advice: Meaningless Facebook Stock Chart

This advice is often easy to say but in reality very difficult to do. Worse, there are many experts out there who will confidently claim that they have a secret system to buying low and selling high.

I offer you 3 reasons why this advice often does more harm than good.

It Assumes A Trading Mindset

If you see any guru who preach about “investing in the long run” and “buy low and sell high”, run away and run away fast. These 2 concepts simply DO NOT mix well together.

The notion of “buying low and selling high” suggests that there is a certain price that you would like to buy and let go. Often, these entry and exit points are obtain from the study of charts (technical analysis). In most cases, the timeframe of this strategy is shorter in nature to make a profit in the stock market.

If you have invested into FB for the long run in 2012, you would be in a lot of pain thinking when to sell simply because FB would have repeated tested the all time highs every few months. The whole intention of “investing in the long run” would be thrown off course because this person is constantly thinking when to sell. Simply put, “investing in the long run” and “buy low and sell high” do not mix well.

At this juncture, I would like to state that if this individual is having a trading mindset. The “buy low and sell high” make sense. It is the essence of his investment thesis as much as “trend is your friend”. But not if you are a long term investor.

It Assumes A Symmetry of Returns

The phrase “buy low and sell high” implies that the stock market goes up 50% of the time and goes down 50% of the time. I believe that it would work well in that situation.

However, in reality this isn’t the case. Bull market are persistent. Bear market don’t last very long. Therefore, the cost of waiting for the “low” is extremely high.

#2: Sells when the S&P 500 hits a new all-time high, buying back into the market after a 5% drop

#3: Sells at S&P 500 record highs, buying back after a 10% correction

Starting from 1960, an USD$100 investment would be worth the following in 2018 (when the article was written)

#1: $28,645 (Yes. No typo here)

#2: $422

#3: $390

You can see that strategy #1 beats the other “buy low, sell high” strategy hands down. The cost of waiting is terribly high if you follow a strict “buy low, sell high” strategy.

It Assumes A Strong Psychological Mindset

While, it is almost impossible to know when the worst days are, buying low is not easy at all. I will take the most current event as an example.

Disclaimer: This is not a buy/sell recommendation.

Alibaba (BABA) stock price plunged down to a new low at $205 (9 July 2021).

In 31 March 2021, revenue for BABA is 798.6 B Yuen. Share price was $229.

While revenue increased 250%, share price only grew 19%. This new low has been attributed to the CCP (Chinese Communist Party) clamping down on Chinese Technology Stocks. Several gurus are calling “sell” because of regulatory risk. Many bloggers are also selling BABA because of “opportunity cost” and believe that money could be put into other counters that is in momentum now. Honestly, I don’t blame them. It is not easy to see your stock price being beaten again and again. It isn’t psychologically easy when price is down. Nobody likes to be wrong. Nobody likes to be wrong for days, months or years. Often, people may even sell at a lost because it may be psychologically difficult.

Long term value investors however are adding into BABA. Among which, Charlie Munger and Mohnish Pabrai are the more noticeable names that are adding into BABA.

Final Thoughts

Disclaimer: I have mentioned some companies above for illustrative purposes. These are not and should not be taken as a buy/sell recommendation.

Personally, I think “buy low and sell high” is an over-simplistic investment thesis. While, it is easy to explain it in theory, reality often paints a different picture. I feel that you should focus on simple, actionable and personalized investment thesis to help yourself achieve the financial freedom that you want.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

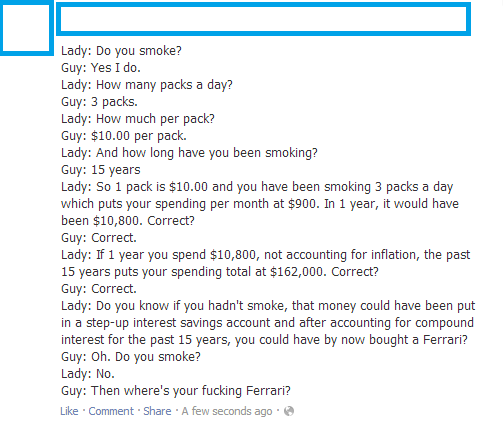

Why Buy Term And Invest The Rest Is Bad Advice: Ferrari Joke

Most of you might have read this joke before. Personally, I think it is easy to give a “good advice” like “stop smoking, invest the money and you will get a Ferrari in 15 years”. Realistically, is that true? I discovered that most people do not take context or circumstances into account before giving “good advice”. This “good advice” might serve as no practical value at all if it is not applicable to the person.

In the financial world, we have many “good advice” around. In this article, I hope to debunk one “good advice”: “Buy Term And Invest The Rest”.

John (imaginary figure) wants to plan for his financial journey. He read a few articles online and discovered that there are many people recommending “Buy Term And Invest The Rest”.

Buy Term: He can consider buying a Term policies for his insurance needs. A Term policy’s regular premium are generally cheaper than Whole Life Policies or an Investment Linked Policies (ILP) that serves his insurance needs (broadly speaking).

Invest The Rest: Because his regular premiums are generally cheaper, he now has more budget to invest in the stock market. He wants to invest in low cost ETFs (exchange traded funds) to reduce any fees. With low charges, this will take care of his wealth accumulation needs.

This sounds great. Personally, I think this is a great advice and a possible strategy for John to consider in his investment journey.

Then Why Do I Think It is “Bad Advice”?

Why Buy Term And Invest The Rest Is Bad Advice

This very simplistic advice often do more harm than good. One example that I would like to draw reference is giving advice to someone to lose weight. The secret to losing weight is very “simple”. All you need to do is just “Eat Healthy Food, Eat Less, Exercise More”. Yet, adult obesity rates in the USA (2017) is a shocking 42.4%. If people already knows this secret, then why are there still so many people who are obese?

This is because everyone’s circumstances and context is different! Duh.

Do you know 95% of diets fail? For a person who has been on a donut diet for most of his/her life, would it be easy to follow this diet?

The conversation today is not about diet. By using the example of weight lost, I hope to be emphasize that everyone is different. This same advice could work for someone with a certain set of mindset and circumstances (maybe he is rich, having a 6 hours work week and a can-do mindset). But not for everyone.

So Why Is Buy Term and Invest the Rest “bad advice”?

Frankly, this advice works. But it only works with a given set of circumstances and context. You can consider this advice if you resonate with the following.

Balanced/Adventurous Risk Profile

I have the privilege of speaking to many people in my career. I have came across some partners and clients who are risk adverse in nature. They do not enjoy fluctuations in their asset prices nor do they like to see losses in their assets. Their favorite asset classes are typically fixed deposits, endowment or bonds. A stock portfolio may not be very suitable for this person’s character. Imagine if you force this individual to buy the ARK K ETF, I willing to bet that he/she will not be able to sleep well at night.

Long Holding Period

In theory, we should all be like Warren Buffett who has an “infinite” holding period. Buy term, invest the rest works ONLY if the person invest the rest and continues to invest the rest. However, this is something we don’t see practically.

A simple question to ask yourself or your friends would be this: when was the last time you sold a stock?

I do acknowledge that there is a combination of factors that contribute to the short holding period. One example is cheap transactional cost. This seemingly good benefit actually destroyed wealth all around the world. In the past, transaction costs to trade was relatively higher that people are more willing to do it only when necessary. Because of the cheap transactional cost now, people are entering and exiting the market as if they are buying groceries in the market. Where did the long term investing go?

But my favourite is the “fear of market crash”. From 2008 until 2020, there have been thousands if not millions of articles/youtubers/gurus world wide calling for market crashes every single year. This keeps people from “investing the rest” into the stock market because they are afraid the market will crash every other month (read this again). Missing the five best days when you’re otherwise fully invested drops your overall return by 35%! Missing the best 10 days will more than halve your long-term returns. Research has again shown that not fully invested will have disastrous effects in the long run. Are you really investing in the long run?

Strong Emotional Stability (in the market)

Investing in the market is not easy. It does not matter if it is a passive strategy or an active one. Imagine if you open your brokerage account one day to see your robo-investing strategy lost 20% of your capital, will you feel afraid and fear that it will continue to drop?

I know there are some who will feel excited. However, I doubt this will apply to the general population.

Investment/Financial Planning Knowledge

When you buy term and invest the rest, there is a strong assumption that you know very specifically the kind of coverage you want and the structure for your insurance needs. At the same time, it also suggests that you know enough about stocks or ETFs to invest appropriately for the long run.

I do acknowledge that there are indeed talented individuals out there that really can do it. They don’t spend hours, they spend decades of their lives to master their financial planning.

Are you spending enough time to acquire these knowledge?

So What Is A Better Advice?

An advice is only good when an individual is able to act upon it in his unique circumstances and context. The best advice are often discovered through brainstorming, asking and answering good questions and also working with someone who is good at doing that.

Just like the best companies in the world hire the best minds in their strategy department, you should also “hire” the best minds to help you in your financial journey.

“Buy term and invest the rest” is a great strategy. However, it only works for a very specific group of individuals. You may or may not be suitable for this strategy. Remember, everyone is different.

Final Thoughts

I believe it is more important to focus on your priorities and your financial needs instead. It would be wise to rethink if these heavily blogged strategies (buy term and invest the rest) can serve you in your financial needs in your unique circumstances and context.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.

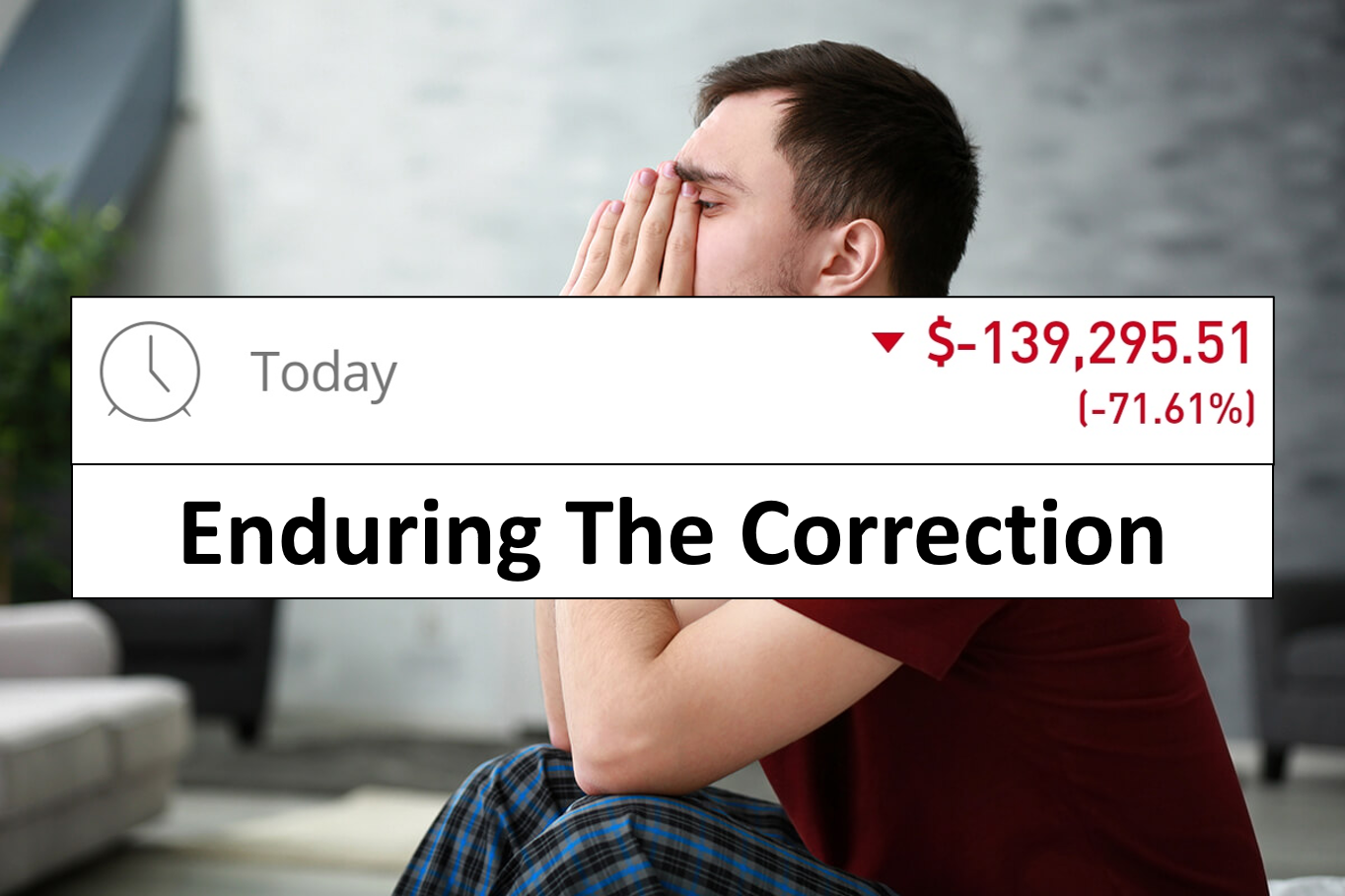

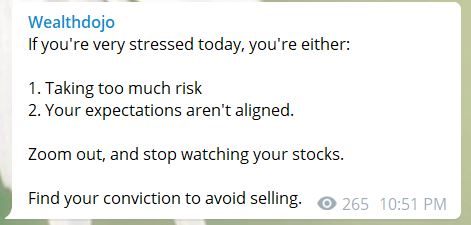

The last few days was beginning to spook investors. Global investors are concerned about rising inflation, coupled with raising 10 year Treasury Yield. This send the S&P500 down with growth stocks taking the lead. You might have the same concerns seeing your portfolio dipped. There were many people that reached out to me. Enough of them for me to put out a message in my telegram channel.

Enduring The Correction Advice

For those of you who started investing in March 2020, this might be your first major correction / bear market (if it is coming). If you feel uncomfortable to see losses, rest assured this is very normal. No one likes to lost money.

Instead of sharing logical data of how each correction ends up higher, I have consolidated a few great quotes from investors I respect. In your wealth management journey, investment is both logical and also an emotional experience.

Enjoy the ride. Hope you find strength in these quotes.

“Stock prices are not business prices. The company you have invested in will not stop/pause to sell their products just because their share price dropped by a few dollars. Whether there is a correction or not, invest in quality companies/portfolios that continue to grow” – Chengkok, Founder of Wealthdojo.

“Unless you buy a stock at the exact bottom (which is next to impossible), you will be down at some point after you make every investment. Your success entirely depends on how dispassionate you are towards short term stock price fluctuations. Behavior matters.” – Joel Greenblatt, American hedge fund manager.

“I deleted my (brokerage) app from phone yesterday so (that) I don’t see again and again. I will (continue to) add money every month and wouldn’t sell a share. I have quality in my portfolio and would evaluate things in 2021 Dec whether to sell anything.” – Rajeev, Singapore Investor.

“In times like these, the best thing to do is to research companies… and then come away with optimism that “wow… so much growth yet to happen!” – Ser Jing, Portfolio Manager of Compounder Fund.

“The principles have not changed. #1 Buy great companies #2 Buy them at fair value.” – Dr Daniel Kao.

“Rotation is the lifeblood of any bull market.” – Ralph Acampora, Director of Technical Analysis at Prudential Securities.

“Market is just price movement, it is never about the whole business. Where-else the underlying asset which the company that provide the goods and services is the real deal biz to the industry.” – Singapore Investor #2.

Final thoughts by Wealthdojo

Once again, I would like to thank all who have contributed to the above quotes. Enjoy the ride.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.