Winning the BTO lucky draw is a bonus for many of young married couples. Pinnacle @ Duxton, Natura Loft @ Bishan, The Peak @ Toa Payoh are among the few that has made headlines for being sold at over a million dollars. These BTO are typically are matured areas.

The government then came up with the PLH model to discourage property inflation especially in the matured area.

In this article, I hope to share whether you should apply for River Peaks @ Rochor in the aspect of financial planning (affordability). I will seek to illustrate how much you should be earning monthly to be able to afford this property comfortably.

The Assumptions

Buying price for River Peaks is $635,000 (Average of $582K to $688K).

The couple is eligible for BTO application, no debts, no grant whatsoever. They pays for equal portion of the HDB downpayment and the loan. They starts from zero with no help from parents.

We are using HDB loan that requires the couple to pay at least 10% downpayment ($63,500) of the purchase price. We do not use bank loan as it require 25% downpayment and we assume that it is not an easy sum to pay.

We do not include stamp duties and misc expenses.

Illustration #1: Young Couple that just started working

If your partner and yourself are young with a few years of work experience, HDB loan might be the only option if you do not have capital.

Taking the medium monthly gross $3468 for the age group 25-29, your CPF-OA contribution will be $797.85 monthly. It will take you roughly 40 months / 3.5 years to have $31,750 in your CPF-OA. This means that you can consider applying for this BTO if you have already worked at least 3.5 years. Of course, if you have a good saving habit, you can use cash to pay for the downpayment (see #1A).

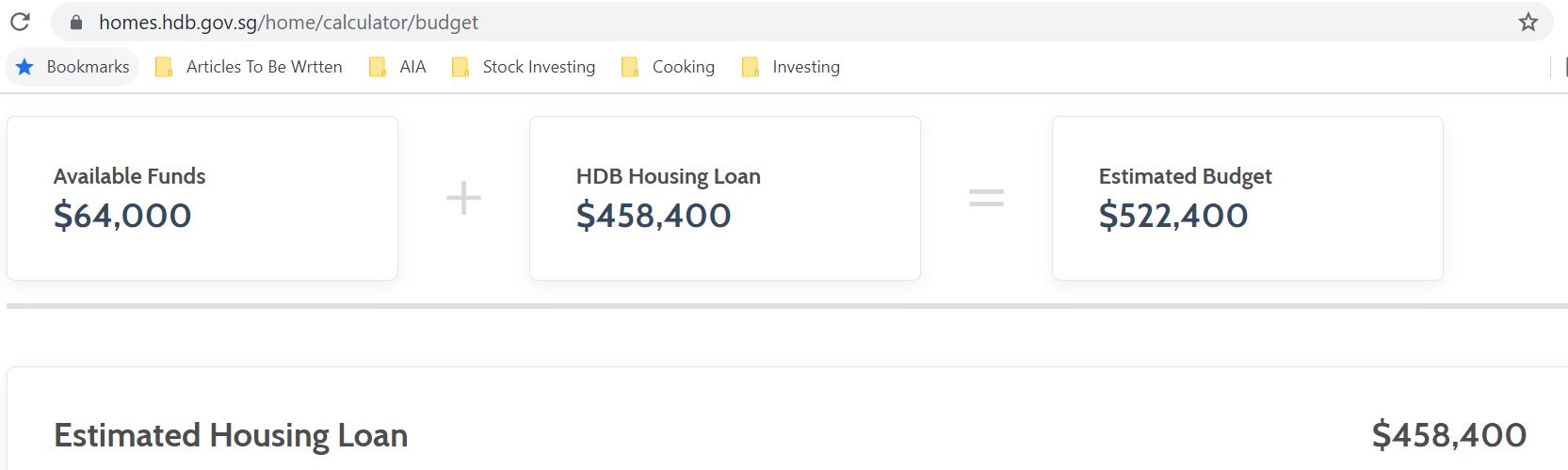

However with the monthly gross salary of $3468, the available HDB loan that is $458,400 and this is insufficient as the loan amount required is $571,500. There is shortfall of $113,100.

In this case, you cannot apply for the Rochor BTO unless you have saved an extra $113,100.

Illustration #1A: Young Couple that just started working and are savers

Let’s push the assumption one step further and assume that the young couple saves 30% of their income for downpayment. This translates to $1040.4 cash and $797.85 CPF-OA per person per month.

Shortfall: $635,000 (property value) – $458,400 (potential loan amount) = $176,600

Monthly Couple Saving Towards Property: [$1040.4 + $797.85]*2= $3,676.5

This translates to 48months or 4 years.

Their estimated monthly mortgage repayment will be $2,080 for a 25 years payment at 2.6%. This works to be cash of $242.15 per person monthly.

This is doable but not easy. However, majority of their equity will be in their house.

Illustration #2: Young Couple that just started working with higher median monthly income

Given that the constant is the amount of loan that can be obtained, I did the reverse calculation and found out that a monthly income of $4,400 will produce the HDB loan of $576,000.

In this case, a monthly income of $4400 would mean your CPF-OA would have $1012.09 being contributed monthly. It will take around 32 months or 2.7 years to have $31,750 in your CPF-OA.

Similarly, their estimated monthly mortgage repayment will be $2,080 for a 25 years payment at 2.6%. This works to be cash of $55.82 per person monthly.

Definitely suggest that you probably need a higher income to be comfortable to afford this property.

Final Thoughts

I expect that people applying for this BTO is probably going to be couples that have worked for at least 4 to 6 years (maybe 28 to 32 years old). I expect that their income to be at least $4000 to consider this project.

This assumption means that they have both time to save in their CPF and their saving account to afford for this project.

The downside is that the project have a waiting time of 71 months or close to 6 years (without delay). This means you would not be able to have a home until you are close to the mid 30s.

What do you think about this project? Let me know in the comment below.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

Feel Free To Reach Out To Share Your Thoughts.

Contact: 94316449 (Whatsapp) chengkokoh@gmail.com (Email)

Telegram: Wealthdojo [Continuous Learning Channel]

Reviews: About Me

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.