We have a problem.

We have a big problem.

We are living in a post war era. Majority of the world are living in peace. Education are not meant for the privileged rich anymore. We have access to knowledge to Universities and Google. Jobs are readily available. We are literally working at home right now. Our system being flushed with money.

According to the World Bank, the 2019 literacy rate is at 86.47% as compared to 66.91% in 1976. Back closer to home, Singapore’s literacy rate stands at 97.34%, with 88.89% of our population having enrolled in tertiary education. It is impressive how far we have become in terms of literacy.

Despite that, CareerBuilder found that 78% of U.S. workers are living paycheck to paycheck. In Singapore, we can only guess the amount of people who is living from paycheck to paycheck as we do not have a statistic on it. Based on an article by HRAsia in 2015, 14% (of Singaporeans) have no savings at all and the most surprising find was the 37% of the top-income bracket is essentially spending everything they earn.

While we are getting more educated, we might be leading into a new generation that will be known as “The Educated Poor“.

To save this generation of the Educated Poor, I have created the 6 Levels Wealth Karate to guide and help them escape misery. Are you one of them?

Are You the Educated Poor?

We assume that the more educated we are, the more successful we will be. This was in fact, the mindset that has been ingrained into us by our parents since we were young. Our parents live in a different era. My parents often told me stories of the rich having the privilege of going to school. The rest of them had to help out at home, their family’s businesses or take care of their younger siblings. Some of their siblings who are lucky to have some education went to the workforce and saw how they missed out on promotion because someone else had a “higher qualification”. Therefore, their generation are willing to sacrifice, to eat less, to work overtime to give their children the opportunity of higher education. It is to some of their greatest regret that they did not have a Degree and their greatest pride when their children got their Degrees. Hence, it is of no surprise that the current generation is more educated.

As the current generation becomes more educated, it is less of a signaling effect (You might have studied this in your Economics modules) to the employers anymore. Education is now a necessity and less of a differentiating factor.

Before this article gets too scholarly, I have observed some similarities in the Educated Poor and hope that by identifying them, you can have clarity if you are one of them. If you are, we welcome you to be enlightened.

#1: The Great Paper Chase

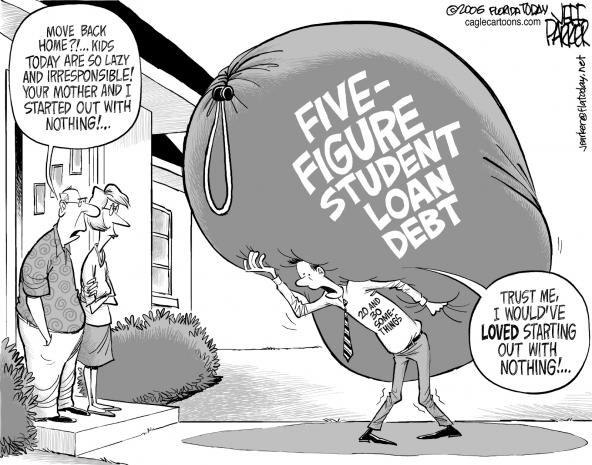

Much has been said about the pursue of education. If you reading this, you are probably among the 88.89% of Singaporeans who have a tertiary education. If left unplanned by your parents, it will become your first biggest expenditure after University.

With reference to another article on how to be free from the burden of university debt, I graduated in 2013 with a Bachelor (Hons) in Mathematics and Economics in Nanyang Technological University. I cut my University studies short from 4 years to 3.5 years to save on cost. In total, my degree costed $20K. My peers and I have a typical debt of between $20K to $40K after graduating. We will then spend the next 2 to 5 years to clear your University debts.

During the time when you are working, you might have anxious peers who have Masters or taking a Part-Time Masters. Some of you might be job hunting and while waiting, started a Masters to boost your resume. This is known as the great paper chase.

To remain competitive, the first instinct that the Educated Poor have is to get a higher qualification.

Don’t get me wrong. I believe in education and also believe in higher qualification IF it is necessary. For example, I will appreciate my surgeon to be academically competent.

However for most of us, we believe that having a higher qualification will lead to a higher pay. From my peer’s experience, not only the pay increase was insignificant, they are now “too over qualified academically” for their job and to add insult to injury, they are down with a heavier debt to repay in the next 5 years.

Do consider getting higher qualification if it make sense. Here are some examples (not limited to the following) when it make sense.

- Your qualification is necessary for your career advancement

- You can only attain the skill set from the Masters

- It fits your long term goal

- Networking in your industry

The mindset of an Educated Poor is to “remain competitive” by getting a higher qualification. However, they may suffer the debt consequence IF the qualification does not open the doors for them.

#2: The Great Material Chase

Money can buy many things. Our minds are programmed to keep wanting something new, something better, something different. Rachel did a guest post for me that talked about 3 Money Beliefs That Will Destroy Your Life. Let me quote for you my favourite phrase she used.

It’s funny, though, because our happiness actually comes from the absence of wanting. When we’ve gotten that new [insert material thing here], for a moment we don’t want anything else. But once our mind gets bored, it looks for something else to focus on…

This is just one reason why we want to buy something.

However, I believe this stems deeper. You may have experienced buying something on impulse, used it once or twice and then allowed it to collect dust after that. You are not alone in this. I have many random objects in my house which I bought because I thought it looked cool. It has been sitting on my table coolly after that. Actually, you are really not alone, the whole world is together with you on this. In May 2020, consumer debts hits new record of $14.3 trillion. People are buying things on credit!

People buy things based on emotional needs or wants, and then justify their purchase logically.

A common observation I have noticed is that some people connect their self worth to the things they have. This lead to great material chase. I once known a lady who spent $6,000 on a Channel Boy to show the world (her friends and colleagues) that she is doing well in life. The Channel Boy was bought on credit. She racked up a total more than $10,000 worth of credit card debts, was only servicing the minimum amount every month with her cashflow maxed out. When I found that that Channel Boy had a good resale value, I suggested selling the Channel Boy to improve her financial situation.

“What if her colleagues looked down on me because I’m using an xxx bag? Everyone in office is using a Channel or an LV”.

While I hear her point of view, the response shocked me.

PS: The Channel Boy was just the tip of the iceberg.

I’m observing a world where purchases are made because of the emotional need of significance. We have money. Men buy luxury watches and continental cars (maybe Tesla?) to feel powerful. Women buy branded handbags and expensive wallets to feel important. While the items can be different, you are in a world where buying/owning something makes you feel special. Perhaps, that is the thing that is missing in our generation. In the generation of the Educated Poor, we don’t feel special. We feel like a gear in life. We wake up, we go to school, we graduate, we get a job, we buy a house, we have children, we retire and then we die.

To fill up that void, the Educated Poor embarked on the Great Material Chase.

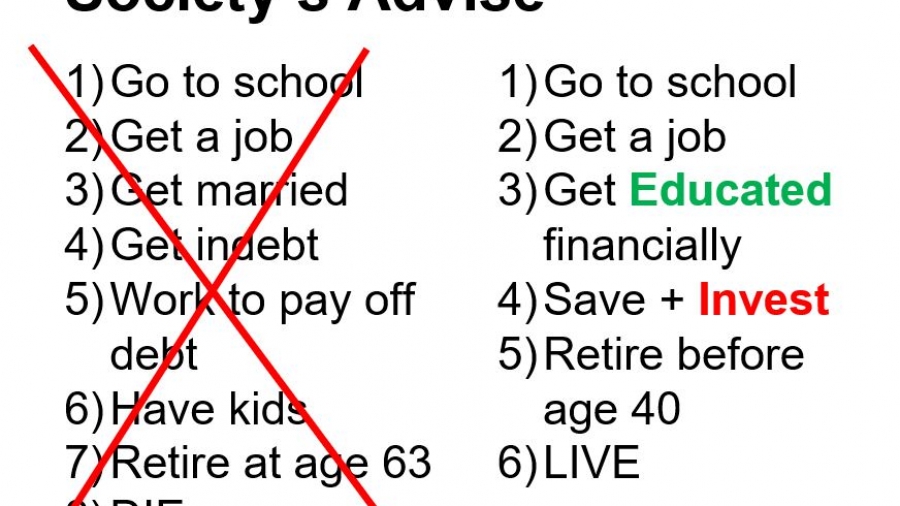

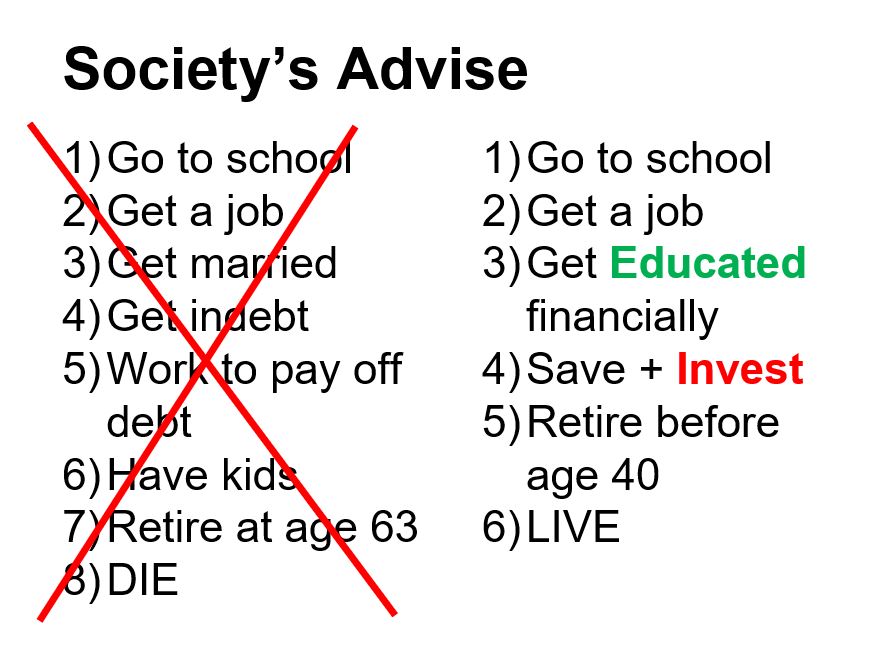

#3: The Outdated Financial Game Plan

Last but not least, the Educated Poor is playing an outdated financial game plan. We are following the game plan of the previous generation. The previous generation ingrained their success game plan into us without know that the game has been changed.

Plenty of people in the world are still running on the outdated game plan on the left. This situation has been made worse as the Educated Poor are less likely to seek professional advice (in the context of making investment decisions). It is likely that the Educated Poor will continue to continue running the existing game plan.

A brunch of friends who achieved financially freedom used the updated game plan on the right. The one thing you can do differently is to get educated financially early. You have to be willing to invest in yourself with knowledge and also the right partners/mentors. You will then be less likely to be affected by the Great Paper Chase and the Great Material Chase as you will then have clarity on your game plan towards financial freedom.

Are you following the game plan on the left?

Final thoughts by Wealthdojo

I have created the 6 Levels Wealth Karate to give the Educated Poor a fighting chance in this life.

With the Great Paper Chase, The Great Material Chase and also an Outdated Financial Game Plan, they become stuck financially and unable to achieve the results they desire in life even though they may be very hardworking.

If this article resonates with you, if it makes your uncomfortable, it is okay. Although 2020 is ending, your life has just began. Take this opportunity to change. I wish you all the best. Do comment below your thoughts. I would love to hear from you.

Chengkok is a licensed Financial Services Consultant since 2012. He is an Investment and Critical Illness Specialist. Wealthdojo was created in 2019 to educate and debunk “free financial advice” that was given without context.

Feel Free To Reach Out To Share Your Thoughts.

Contact: 94316449 (Whatsapp) chengkokoh@gmail.com (Email)

Telegram: Wealthdojo [Continuous Learning Channel]

Reviews: About Me

The views and opinions expressed in this publication are those of the author and do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any entity other than the author.